For decades, Pakistan’s merchandise exports have been stuck in low gear. The headline numbers show some growth — from around $9 billion in 2000 to just over $32 billion today — but the pace has been glacial, especially when viewed against regional peers such as Bangladesh, Vietnam, Cambodia, Sri Lanka, and India. When all countries’ exports are rebased to 100, Pakistan’s line barely nudges upward over a full decade, while competitors have scaled their export bases by multiples.

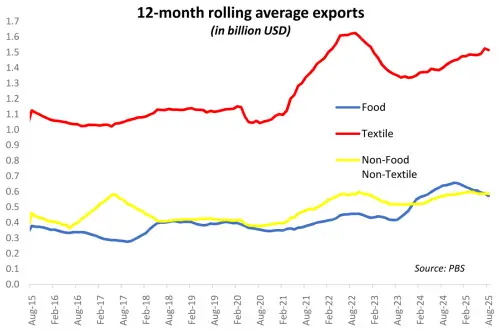

The divergence is most stark when looking at Vietnam and Bangladesh. Both began the 2000s from similar starting points as Pakistan but surged ahead by anchoring their industrial strategy around export-oriented manufacturing. Pakistan, by contrast, has failed to sustain a similar trajectory. This is not only a story of missed growth, but also of premature deindustrialisation: the non-food, non-textile segment — largely large-scale manufacturing and SME-driven products — has barely moved in ten years. The charts show stagnation, where in a country seeking industrialisation, one should expect takeoff.

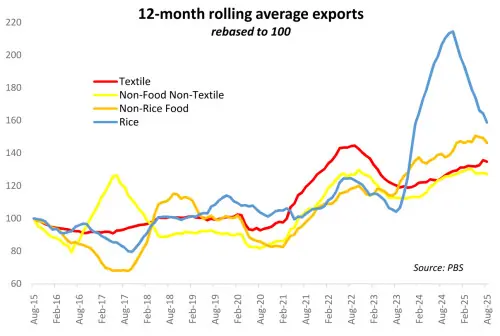

Yes, there have been encouraging transitions within textiles. The shift from low-value yarn and fabric exports to higher-value-added products such as readymade garments, knitwear, and bedwear has been steady. But textiles alone cannot carry the burden of a $350 billion economy. Worse still, the surge in rice exports over the past two years — which gave a temporary lift to food exports — was a windfall created by India’s export restrictions. The spike is already fading, underscoring that Pakistan’s gains are often circumstantial rather than structural.

The deeper problem lies in the industrial base. Non-food, non-textile exports — essentially the backbone of manufacturing diversity — have flatlined. That speaks to weak competitiveness in industrial clusters, thin integration into global value chains, and limited innovation. Pakistan’s export basket appears diversified on paper, but in reality, new entrants have failed to make meaningful inroads. This hollowing-out is visible in foreign direct investment trends too: inflows are typically directed at sectors serving domestic consumption or, at best, import substitution. Export-oriented FDI remains negligible, in contrast to the experience of Vietnam or Cambodia, which actively attracted global manufacturers seeking efficiency and scale.

The policy record does not inspire confidence either. Successive five-year and even 15-year industrial and export strategies have been rolled out, only to be discarded or overtaken by crises. Chronic problems refuse to budge: energy costs are a drag, but not the only constraint; inconsistent policies, weak logistics, and shallow institutional support for exporters are equally binding. The fact that even this modest export performance has been achieved largely through state patronage — in the form of subsidised financing and an artificially cheap labour cost base — highlights the fragility of the model.

The much-discussed “potential” of Pakistan’s exports risks becoming an empty slogan. Potential needs to be backed by competitive edge. Where, precisely, does Pakistan hold such an edge? Is there an exportable surplus in goods where the country can scale sustainably? These questions remain unanswered even as years slip by. The temporary duty advantages enjoyed in Western markets may also be short-lived, and are no substitute for a coherent long-term strategy.

The challenge ahead is not just to lift export numbers for the balance-of-payments math. Pakistan’s export strategy must be one that creates jobs, deepens industrial capacity, and embeds the economy into global production networks. That requires narrowing the focus to sectors where Pakistan can realistically scale and build clusters of competitiveness. Without that, the country will continue to stand still while its peers — starting from the same place a generation ago — leave it further behind.

Comments

Comments are closed for this article.