Husein Industries Limited (PSX: HUSI) was incorporated in Pakistan as a public limited company by the name of Husein Textile Mills. In 2014, the company discontinued its textile business and entered into real-estate business, construction and allied businesses.

Pattern of Shareholding

As of June 30, 2024, HUSI has a total of 10.626 million shares outstanding which are held by 966 shareholders. Directors have the majority stake of 33.94 percent in the company followed by Husein Ibrahim foundation holding 20.57 percent shares and individuals holding 15.86 percent shares.

Around 14.37 percent of HUSI’s shares are held by charitable institutions and 9.45 percent by investment companies.Trust account for 3.63 percent shares of HUSI.

The company’s CEO, Mr. Husein Jamal hold 1.45 percent shares. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

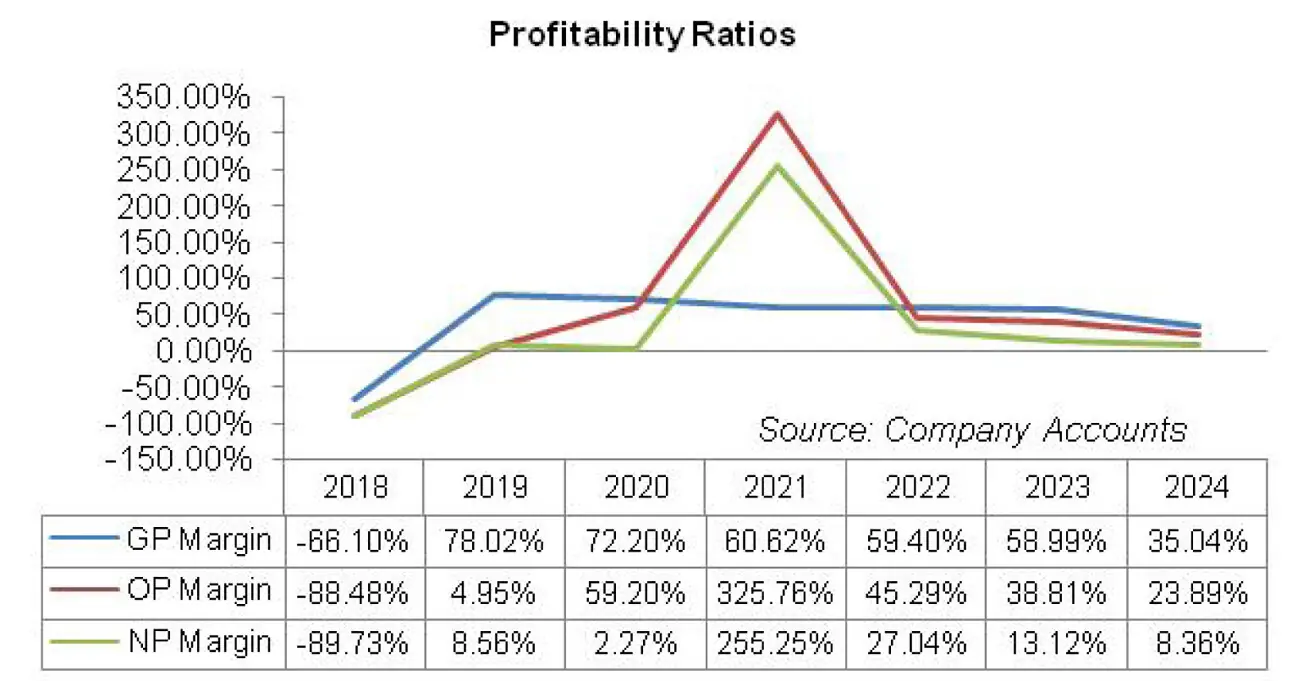

During the period under consideration, HUSI’s topline dropped in 2019 and 2023. Its bottomline which had been in the negative zone for eight years until 2018; registered net profit in 2019.

HUSI’s net profit drastically declined in 2020 followed by a staggering rise in 2021. In the subsequent two years, HUSI’s bottomline began to shrink followed by growth recorded in 2024. The company’s margins considerably improved in 2019.

In 2020, gross and net margins fell while operating margin tremendously strengthened. In 2021, gross margin continued to plunge while operating and net margins attained their highest levels. In the subsequent years, all the margins dived down (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, HUSI’s topline fell by 14.17 percent to clock in at Rs.63.83 million. The decline in net sales in 2019 was due to the fact that the company disposed off its textile stock worth Rs.75.858 million in 2018.

In 2019, with no leftover inventory in hand, the company started afresh and made revenue from sale of plots and also made rental income. Cost of sales dropped by 88.64 percent in 2019 as there was no cost related to textile inventory.

The only cost incurred by HUSI in 2019 was the cost of development property sold as well as expenses related to rented property. The company made gross profit of Rs.49.8 million in 2019 versus gross loss of Rs.49.16 million posted in 2018. GP margin stood at 78 percent in 2019.

Administrative expense plummeted by 26.52 percent year-on-year in 2019 due to curtailed depreciation expense as well as payroll expense.

Other charges narrowed down by 7.86 percent in 2019 as unlike last year, the company didn’t incur loss on the sale of inventory as well as loss on de-recognition of building in 2019. Furthermore, there was no re-measurement loss on investment carried at FVTPL in 2019.

On a gloomier note, other income contracted by a massive 97.69 percent in 2019 as HUSI sold the plot from which it earned rental income in 2018. The absence of rental income severely squeezed its other income.

The company recorded operating profit of Rs.3.159 million in 2019 with OP margin of 4.95 percent versus operating loss of Rs.65.8 million in 2018.

The company had acquired long-term loan and short-term loans from external creditors which were in the process of restructuring with overdue mark-up to be completely waived. HUSI recorded net profit of Rs.5.467 million in 2019 as against net loss of Rs.66.734 million posted in 2018.

EPS stood at Rs.0.51 in 2019 versus loss per share of Rs.6.28 registered in 2018. NP margin clocked in at 8.56 percent in 2019.

In 2020, HUSI’s net sales multiplied by 69.73 percent to clock in at Rs.108.34 million. This was due to hefty lease income recorded during the year. Cost of sales mounted by 114.71 percent in 2020 due to elevated repair & maintenance expense, utility charges as well as commission paid.

Gross profit grew by 57 percent in 2020; however, it translated into lower GP margin of 72.20 percent. Administrative expense nosedived by 12.16 percent in 2020 due to lower depreciation expense. Other charges dropped by 99.70 as no impairment loss on trade debts was recorded in 2020.

Other income also slid by 98.23 percent in 2020 particularly because the gain on disposal of vehicles recorded in the previous year was missing in 2020. This translated into 1930.23 percent taller operating profit recorded by HUSI in 2020 with OP margin of 59.0 percent. HUSI recorded finance cost of Rs.60.52 million in 2020 versus finance cost of Rs.5000 in the previous year.

The increase in finance cost signified mark-up on delayed payment of restructured loan, mark-up on directors’ loan as well as bank overdraft. HUSI also incurred commission on bank guarantees in 2020 which also drove up its finance cost.

Higher finance cost resulted in 54.95 percent decline in net profit which clocked in at Rs.2.463 million in 2020 with EPS of Rs.0.23 and NP margin of 2.27 percent.

In 2021, HUSI registered 38.16 percent higher topline to the tune of Rs.149.68 million. This was due to significant rise in the sale of residential plots as well as robust lease income recognized during the year.

Cost of sales surged by 95.72 percent in 2021 due to escalation in the cost of development property sold during the year, higher repair & maintenance charges as well as utility expense. Gross profit grew by 16 percent in 2021; however, it culminated into a lower GP margin of 60.62 percent.

Administrative expense hiked by 38.11 percent in 2021 due to higher payroll expense despite the fact that the number of employees was intact at 10. In 2021, HUSI recorded exceptionally higher other income worth Rs.416.22 million primarily on account of waiver of long-term borrowings and mark-up. This resulted in 660.29 percent higher operating profit in 2021 with OP margin of 325.76 percent.

Finance cost slipped by 54.92 percent in 2021 as the company didn’t have to pay mark-up on delayed payment of restructured loan and bank overdraft. Moreover, no commission was paid on bank guarantees in 2021.

HUSI’s finance cost in 2021 only comprised on mark-up paid on directors’ and shareholders’ loan as well as bank charges. HUSI recorded 15413.91 percent greater net profit worth Rs.382.07 million in 2021 with EPS of Rs.35.96 and NP margin of 255.25 percent.

In 2022, HUSI’s topline expanded by 48.21 percentto clock in at Rs.221.85 million. This was on account of sustained lease income and massive rise in the sale of residential property during the year.

The company earned from its main industrial property in Landhi and was constructing further buildings within its property to earn increased revenue. Cost of sales hiked by 52.78 percent in 2022 on the back of escalated repair & maintenance expense.

While gross profit grew by 45.24 percent in 2022, GP margin further tapered off to 59.40 percent. Administrative expense soared by 62.18 percent in 2022 due to increased payroll expense (number of employees stood constant at 10) as well as rent, rates and taxes incurred during the year. One-off event of waiver on long-term loan and mark-up received in 2021 had driven up HUSI’s other income.

However, its absence led to 99.99 percent drop in other income. In 2022, other income comprised of dividend income, gain on disposal of vehicles and other miscellaneous income which were further squeezed by re-measurement loss on investment carried at FVTPL. All these factors translated into 79.39 percent thinner operating profit recorded by the company in 2022 with OP margin radically falling down to 45.29 percent.

Finance cost inched up by 3.33 percent in 2022 which comprised of mark-up on directors’ loan and bank charges. Net profit posted 84.30 percent year-on-year plunge to clock in at Rs.59.996 million in 2022 with EPS of Rs.5.65 and NP margin of 27 percent.

After three successive years of posting topline growth, HUSI recorded 27.61 percent year-on-year diminution in its net sales in 2023. This resulted in net sales of Rs. 160.60 million in 2023. This was the consequence of decline in sale proceeds from residential plots as well as curtailed lease income.

Unprecedented level of discount rate clutched the purchasing power of consumers which coupled with economic and political uncertainty resulted in thin investment in property during the year. Cost of sales plummeted by 26.86 percent in 2023 due to considerably lower cost of development property sold as well as significantly lesser repair & maintenance expense incurred during the year.

Gross profit shrank by 28.12 percent in 2023 with GP margin slightly ticking down to 59 percent. Administrative expense also posted paltry 7.21 percent uptick in 2023 on account of higher payroll expense. Profit on Al-Meezan Investment gave boost to HUSI’s other income which recorded 2017.11 percent growth in 2021.

HUSI’s other income stood at Rs.1.22 million in 2023. Operating profit fell by 37.97 percent in 2023 with OP margin sinking to 38.81 percent. Finance cost increased by 59.70 percent in 2023 due to increased mark-up on directors’ loan. Net profit slid by 64.89 percent in 2023 to clock in at Rs.21.067 million with EPS of Rs.1.98 and NP margin of 13.12 percent.

With 125.94 percent year-on-year topline growth in 2024, the ongoing year seems to have a silver lining for the company. HUSI’s net sales clocked in at Rs.362.87 million in 2024.Revenue growth came on account of higher sale of residential plots and elevated lease income.

During the year, the revenue from the sale of residential plots posted a phenomenal year-on-year growth of 512.15 percent to clock in at Rs.183.510 million, accounting for 50.57 percent of the total sales mix of HUSI in 2024.

In the previous year, sale of residential plots had a share of 18.67 percent in the sales mix of the company. This implies that HUSI is undertaking a great deal of diversified construction projects to boost its revenue streams. However, it is to be noted that the company didn’t recognize any sale of commercial projects in 2024.

Cost of sales magnified by 257.82 percent in 2024. The main growth drivers of cost were thecost of development projects, repair & maintenance charges as well as fuel & power expense.

The company converted one of its properties into commercial cum residential projects during the year which also indicates towards elevated cost of development projects and higher repair & maintenance cost incurred during the year.

Gross profit grew by 34.24 percent in 2024, however, GP margin marched down its six-year low of 35 percent. Administrative expense grew by 19.67 percent in 2024 on account of higher payroll expense, utility expense as well as travelling and legal charges incurred during the year.

Other income stood at Rs.1.75 million in 2024, up 42.82 percent year-on-year. This mainly included profit on saving deposits. Other income was completely offset by other charges of Rs.1.99 million recorded during the year which comprised of provisioning done for WPPF.

HUSI posted 39 percent higher operating profit in 2024, however, OP margin dipped to 23.89 percent. Finance cost surged by 34.30 percent in 2024 due to higher mark-up on loans obtained from the company’s directors. The company was able to register net profit of Rs.30.347 million in 2024, up 44 percent year-on-year. EPS stood at Rs.2.86 while NP margin dwindled to 8.36 percent in 2024.

Recent Performance (9MFY25)

While the company reversed the downward journey of its topline in 2024, it lost its ground yet again with 13.42 percent slide in its net sales in the ongoing fiscal year. HUSI’s net sales were recorded at Rs.184.28 million in 9MFY25. This was due to a downtick recorded in the sale of residential plots during the period which was on account of the fact that the company had some unfulfilled performance obligations which it will recognize in a phased manner based on the completion of the development work.

Cost of sales shrank by 26.46 percent in 9MFY25 due to lower repair charges and lower cost of development projects incurred during the period.

HUSI recorded 6.45 percent uptick in its gross profit in 9MFY25 with GP margin inching up to 48.72 percent versus GP margin of 39.62 percent recorded during 9MFY24. Administrative expense mounted by 19.12 percent during the period under review seemingly on account of higher payroll expense to conclude the ongoing projects in a timely manner.

Other income ticked up by 2.98 percent during 9MFY25 probably due to higher rental income as HUSI converted one of its properties into commercial cum residential project which is generating positive cash flows for the company.

Other income, however, was completely wiped off by other expense worth Rs.0.82 million incurred which encompassed profit related provisioning done during 9MFY25. HUSI’s operating profit dipped by 1.10 percent to clock in at Rs.57.39 million in 9MFY25. This translated into OP margin of 31.14 percent in 9MFY25 versus OP margin of 27.26 percent recorder during 9MFY24.

Finance cost thinned down by 21.51 percent due to monetary easing. HUSI recorded 118.96 percent stronger bottomline to the tune of Rs.26.787 million in 9MFY25. This culminated into EPS of Rs.2.52 in 9MFY25 versus EPS of Rs.1.15 recorded in 9MFY24. NP margin staggeringly improved from 5.75 percent in 9MFY24 to 14.54 percent in 9MFY25.

Future Outlook

As of March 31, 2025, HUSI had negative shareholders’ equity of Rs.49.608 million versus Rs.76.396 million worth negative equity reported during the same period last year. This was on account of accumulated losses of Rs.989.057 million as of March 31, 2025 which stood at Rs.1026.840 million as of March 31, 2024. Its current liabilities also exceeded as its current assets by Rs.633.22 million as of March 31, 2025. This may cast significant doubts about the ability of the company to continue as a going concern.

However, the management is confident that the launch of Jamal Garden residential/commercial projects will rake in reasonable revenue in the coming times and will enable the company to initiate more projects which will soon result in positive shareholders’ equity by squeezing the accumulated losses.

Comments

Comments are closed for this article.