Hinopak Motors Limited (PSX: HINO) was incorporated as a public limited company in Pakistan in 1986. The company is engaged in the assembly, progressive manufacturing and sale of Hino buses and trucksas well as sale of its spare parts and accessories.

HINO is the subsidiary of Hino Motors Limited Japan. The ultimate parent company of HINO is Toyota Motors Corporation Japan.

Pattern of Shareholding

As of March 31, 2025, HINO hasa total of 24.801 million shares outstanding which are held by 2194 shareholders. Hino Motors limited Japan has the majority stake of 59.67 percent in the company followed by Tsusho Corporation Japan holding 29.83 percent shares of HINO.

These are followed by local general public accounting for 6.15 percent shares and NIT & ICP holding 3.38 percent shares of the company. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

Except for a year-on-year rise in 2022, 2023 and 2025, HINO’s topline has inched down in all the years under consideration.

The company’s bottomline also stayed in the positive zone in these three years with net loss recorded in the remaining years. Gross and operating margins of the company slid in 2019 and entered negative zone in 2020. In the subsequent two years, gross and operating margins greatly recovered followed by a downtick recorded in 2023.

In 2024, gross margin registered significant growth while operating margin continued to slide. In 2025, both gross and operating margins boasted their optimum levels. Net margin posted positive value only in 2022, 2023 and 2025. The detailed performance review of the period under consideration is given below.

In 2019, HINO’s net sales slumped by 28.12 percent year-on-year to clock in at Rs. 19,130.84 million. This was becausethe commercial vehicle industry in Pakistan shrank by 14 percent year-on-year due to depreciation of Pak Rupee coupled with the slowdown of CPEC on account of lesser government spending in the project.

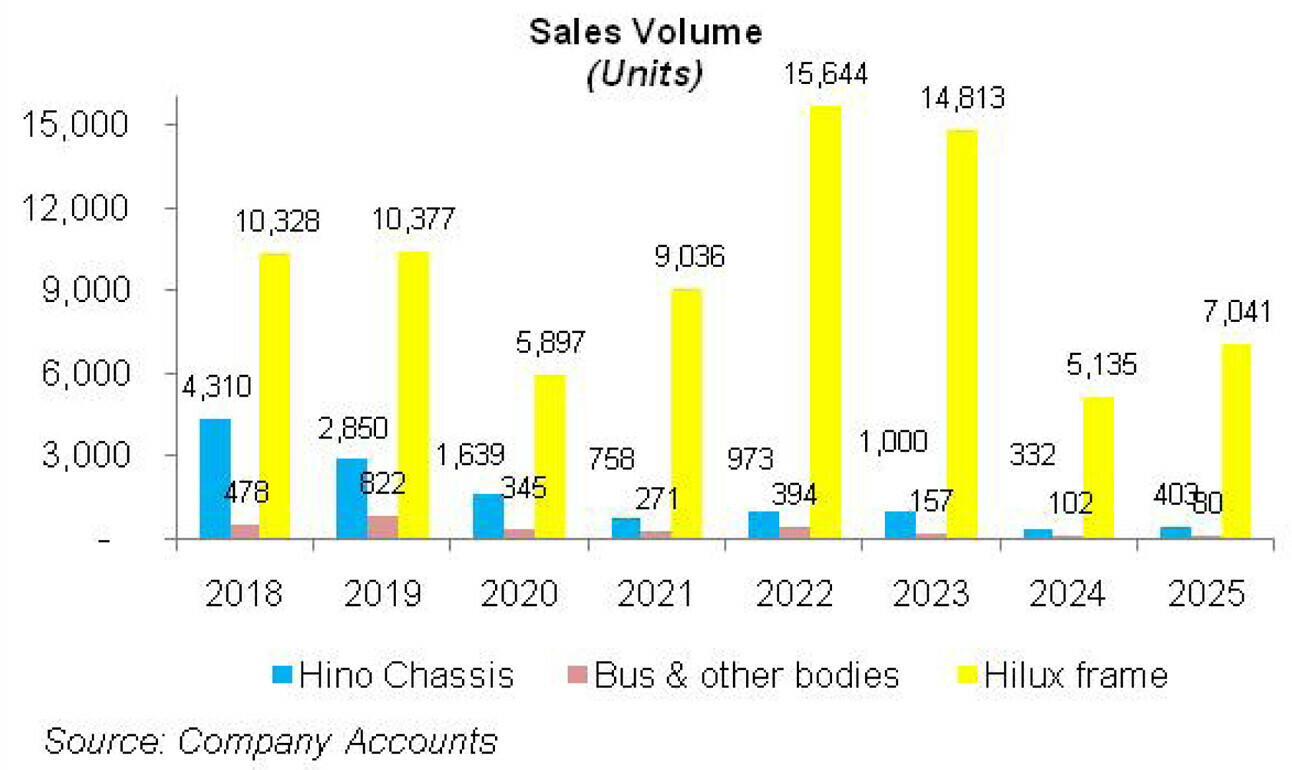

Besides, the auto industry also sufferedvolumetric decline due to restriction imposed on the purchase of vehicles by non-filers. During the year, the sale of HINO Chassis slumped by 34 percent year-on-year to clock in at 2850 units.

Conversely, bus and other bodies and well as Hilux frame recorded growth of 72 percent and 0.5 percent to clock in at 822 units and 10,377 units respectively. The company was able to maintain its market share of 31 percent and 41 percent in truck segment and bus segment respectively.

Due to decline in the company’s manufacturing operations, cost of sales dropped by 23.59 percent year-on-year in 2019. High per unit cost is evident by the fact that gross profit shrank by 63.31 percent year-on-year in 2019 while GP margin fell from 11.40 percent in 2018 to 5.82 percent in 2019.

Owing to lesser staff cost, curtailed advertising and promotion budget as well as slashed legal and professional charges, distribution cost ticked down by 18.30 percent year-on-year in 2019.

Administrative expense also declined by 9.93 percent year-on-year in 2019. Other income posted a massive 50.92 percent year-on-year plunge in 2019 due to lesser return on bank deposits and lesser commission from Group Company.

Other expense plummeted by a whopping 98.91 percent year-on-year in 2019 on account of low provisioning for WWF and WPPF. The company also booked impairment of Rs. 19.53 million on trade receivables in 2019. Operating profit shriveled by 78.64 percent year-on-year in 2019 while OP margin fell down from 8.82 percent in 2018 to 2.62 percent in 2019.

Finance cost grew by 50.49 percent year-on-year in 2019 on the heels of high discount rate and also because of short-term loans obtained by the company during the year which were not on its books until 2018.

However, the major component of finance cost was exchange loss which stood at Rs.815.803 million in 2019, up 28 percent year-on-year. The company recorded net loss of Rs.873.28 million in 2019 as againstnet profit of Rs.1149.38 million posted in 2018. HINO posted loss per share of Rs.70.42 in 2019 versus EPS of Rs.92.69 registered in 2018.

In 2020,HINO’s topline posted another 31 percent year-on-year slump to clock in at Rs.13,191.06 million. The automobile market shrank by 44 percent year-on-year in 2020 to clock in at 4934 units due to contraction of economy on account of COVID-19, lockdowns imposed during the year and restriction on the movement of people and goods which lowered the demand of automobiles.

The sale of Hino Chassis further reduced to 1639 units, down 42.5 percent year-on-year. The sale of bus and other bodies also massively plunged to 345 and 5897 respectively, registering a downfall of 58 percent and 43 percent correspondingly. High inflation and Pak Rupee depreciation kept the cost of sales elevated, resulting in a gross loss of Rs.170.41 million in 2020.

Meticulous cost cutting measures resulted in a reduction of 2.36 percent and 6.11 percent year-on-year in distribution expense and administrative expense respectively despite high inflation.

Other income slid by 43.86 percent year-on-year in 2020 on account of lesser profit on saving deposits and lesser scrap sales made during the year. The company didn’t incur any other expense in 2020. Impairment charge on trade receivables also shrank by 23.63 percent in 2020. Despite keeping a check on expenses, HINO posted an operating loss of Rs.809.218 million in 2020.

Finance cost grew by only 1.27 percent year-on-year due to substantial drop in exchange loss as the company made lesser imports owing to curtailed demand in the local market. Net loss magnified by 135.32 percent year-on-year in 2020 to clock in at Rs.2054.98 million with loss per share of Rs.110.33.

The net sales of HINO posted another 30.77 percent year-on-year plunge to clock in at Rs.9132.18 million. The automobile market also further contracted by 29 percent year-on-year in 2021.

The sale of Hino Chassis and bus and other bodies plummeted by 54 percent and 21.5 percent year-on-year respectively in 2021 while the sale of Hilux frame showed signs of recovery and grew by 53 percent year-on-year (see graph of sales volume).

The company was able to post gross profit of Rs.687.37 million in 2021 as against the gross loss of Rs.170.41 million in 2020. This was on the back of upward price revisions and cost control measures put in place by the company. Distribution expense shrank by 11.68 percent year-on-year while administrative expense remained at almost the same level as recorded in 2020.

Other income slid by 26.24 percent year-on-year in 2021 as there was no commission income from Group Company in 2021. No other expense was incurred during the year and impairment on trade receivables also shrank for second year in a row. Lesser expenses resulted in operating profit of Rs.70.60 million in 2021 as against operating loss of Rs.809.218 million posted in 2020.

OP margin was recorded at 0.77 percent in 2021. Finance cost climbed down by 77.28 percent year-on-year not only because of lower discount rate but also because of the issuance of right shares during the year to pay its short-term loans during the year.

As of March 2021, the company had no short-term borrowings on its books. Despite significant reduction, finance cost was big enough to turn operating profit into net loss of Rs.288.29 million in 2021, down 85.97 percent year-on-year. The company also posted loss per share of Rs.13.37 in 2021.

After three successive years of topline decline and net losses, in 2022, HINO posted year-on-year growth of 37.22 percent in its topline which clocked in at Rs.12,530.89 million. This came on the back of both volumetric growth as well as price increases.

The sales volume of Hino Chassis, bus and other bodies as well as Hilux frame posted growth of 28 percent, 29 percent and 73 percent respectively in 2022. The overall size of automobile market also grew by 68 percent year-on-year in the financial year ending March’22 as the economy fully rebounded from COVID-19.

Although cost of sales also grew by 34 percent year-on-year in 2022 on account of inflation, gross profit rebound of 75.97 percent speaks volume of the superior performance delivered in terms of revenues. GP margin grew to 9.65 percent in 2022. Owing to an increase in the company’s operations, distribution and administrative cost also increased by 14.96 percent and 5.52 percent respectively during 2022.

Higher scrap sales and robust return on bank deposits pushed other income up by a huge 250.81 percent in 2022. Unlike last three years, where the company booked impairment loss on trade receivables, in 2022, the company booked reversal of Rs.16.62 million. After two years, the company was able to book provision for WWF and WPPF worth Rs.41.62 million in 2022.

Operating profit grew by 844.17 percent in 2022 with OP margin climbing up to 5.32 percent. As the company paid off its short-term borrowings in 2021, finance cost majorly comprised of exchange loss and bank charges. This translated into 56.72 percent year-on-year drop in finance cost in 2022.

The company posted net profit of Rs.417.13 million in 2022 with NP margin of 3.33 percent. EPS clocked in at Rs.16.82 in 2022.

In 2023, HINO’s net sales registered 5.23 percent year-on-year rise to clock in at Rs.13,185.97 million. This was for the second consecutive year that the company was able to drive its topline up. A glance at the sales volume shows that only HINO chassis posted a paltry 3 percent year-on-year rise in 2023, while the other two categories lost their ground (see the graph of sales volume).

During the year, the commercial vehicle industry shrank by 15 percent due to sluggish economic activity. Import restrictions also created acute shortage of raw materials forcing many automobile industries to shut down.

HINO was able to capture market share of 20 percent in 2023 as against its market share of 16.6 percent recorded in the previous year. Escalating prices of raw materials was further exacerbated by declining value of local currency during the year. This translated into 6.52 percent surge in cost of sales in 2023.

Consequently, gross profit nosedived by 6.86 percent in 2023 while GP margin fell to 8.54 percent. Inflationary pressure pushed up distribution and administrative expenses by 13.71 percent and 7.49 percent respectively during the year.

Other income contracted by 4.60 percent in 2023 particularly due to low return on deposit accounts. Other expense also shrank by 64.22 percent in 2023 due to lower profit related provisioning done during the year. Operating profit dipped by 22.51 percent in 2023 with OP margin slipping to 3.92 percent.

Finance cost multiplied by 151.40 percent in 2023 due to high discount rate and hefty exchange loss. HINO’s borrowings significantly declined in 2023. Net profit slid by 96.16 percent to clock in at Rs.16.03 million in 2023 with EPS of Rs.0.65 and NP margin of 0.12 percent.

Unprecedented level of inflation, political uncertainties, economic slowdown, credit tightening and high discount rate as well as import restrictions resulted in many unproductive days for HINO and the auto industry as a whole.

After two years of rise, HINO’s net sales drastically fell by 42.19 percent to clock in at Rs.7,622.71 million in 2024. This came on the back of 67 percent, 35 percent and 65 percent year-on-year decline in the sales volume of HINO chassis, bus & other bodies and HILUX frame respectively in 2024 (see the graph of sales volume).

Due to shutdown of operations and thinner production volume, cost of sales shrank by 44.32 percent in 2024. Gross profit also dwindled by 19.41 percent in 2024; however, GP margin attained an unprecedented level of 11.91 percent. Distribution expense tumbled by 1.79 percent in 2024 mainly on account of lower product maintenance charges incurred during the year.

Administrative expense registered 17.71 percent year-on-year surge in 2024 due to higher payroll expense. This was despite the fact that HINO right-sized its workforce from 763 employees in 2023 to 582 employees in 2024.

Other income slumped by 19.59 percent in 2024 due to no return on deposit accounts recorded during the year. Scrap sales and return on saving accounts also fell in 2024. Unlike the last two years, the company didn’t book any provisioning for WWF and WPPF in 2024, hence no other expense.

Operating profit contracted by 60.72 percent in 2024 with OP margin sliding down to 2.66 percent. Finance cost registered 6.47 percent slide in 2024 as the company didn’t incur any exchange loss during the year.

However, short-term borrowings massively increased during the year to clock in at Rs.2285.314 million in 2024 versus Rs.19.309 million in 2023. This drove up mark-up expense in 2024. HINO registered net loss of Rs.131.10 million in 2024 with loss per share of Rs.5.29.

After registering the highest year-on-year fall in 2024, HINO posted a tremendous 35.60 percent growth in its topline in 2025 which clocked in at Rs.10,336.50 million.

While the sales volume of bus & other bodies fell by 22 percent to clock in at 80 units in 2025, HINO Chassis and Hilux frame posted year-on-year growth of 21 percent and 37 percent in its sales volume respectively (see the graph of sales volume). This was in line with the improvement with the wider recovery witnessed in the overall automobile sector.

Easing import restrictions, downing inflation and discount rate, stability in the value of local currency and restoration of investor confidence were the main drivers behind the staggering topline growth recorded in 2025.

Downtick in cost due to stable currency coupled with operational efficiency achieved over the year resulted in 42.25 percent growth in HINO’s gross profit in 2025 with GP margin climbing up to its optimum level of 12.49 percent.

Distribution expense remained largely intact at the last year level while administrative expense posted 4.84 percent downtick in 2025 due to lower payroll expense as HINO streamlined its workforce from 582 employees in 2024 to 501 employees in 2025.

Other income ticked up by 8.58 percent in 2025 due to reimbursement of finance cost under cost compensation agreement with Hino Motors Japan for holding additional inventory by the company. While HINO recorded no other expense in 2024, it registered other expense to the tune of Rs.23.75 million in 2025 on account of profit related provisioning.

Operating profit strengthened by 196.68 percent in 2025 with OP margin jumping up to 5.82 percent. Despite monetary easing, HINO’s finance cost grew by 17.81 percent in 2025 due to exchange loss and increased short-term borrowings. HINO posted net profit of Rs.161.957 million in 2025 with EPS of Rs.6.53 and NP margin of 1.57 percent.

Recent Performance (Quarter ended June 30, 2025)

During the first quarter ended June 30, 2025, HINO registered 106.49 percent year-on-year growth in its topline which clocked in at Rs. 3961.557 million. This came on the back of a phenomenal 136.84 percent rise in the sales volume of Hinopak trucks and buses which clocked in at 180 units.

Improved sales volume coupled with price optimization and cost control resulted in 276.26 percent higher gross profit in 1QFY25 with GP margin clocking in at 21.34 percent versus GP margin of 11.71 percent posted in 1QFY24. Higher sales volume resulted in 22.55 percent spike in distribution expense in 1QFY25.

Administrative expense also ticked up by 4.39 percent in 1QFY25 due to inflationary pressure which pushed up the payroll expense. Other income picked up by 9.66 percent during the period due to reimbursement of finance cost by Hino Motors Limited, Japan.

Improvement in Other incomewas despite the fact that the company recorded no exchange gain in 1QFY25. Other income was completely offset by other expense of Rs.34.23 million registered by the company during the period due to provisioning done for WWF and WPPF.

Operating profit strengthened by 1195.37 percent in 1QFY25 with OP margin jumping up to 15.48 percent versus OP margin of 2.47 percent posted during the same period last year. Finance cost ticked up by 2.67 percent during 1QFY25 on account of exchange loss and hefty short-term borrowings.

HINO recorded net profit of Rs. 416.817 million with EPS of Rs. 16.81 and NP margin of 10.52 percent in 1QFY25. This was against net loss of Rs.119.688 million and loss per share of Rs.4.83 registered in 1QFY24.

Future Outlook

The recovery of industrial activity and better politico-economic environment will bode well for the sale of buses and trucks. Moreover, with the government determined to develop and modernize urban public transport, HINO expects a brighter future. On the flipside, the introduction of NEV levy across all internal combustion vehicles including trucks & buses and restriction on the purchase of new vehicles by non-filers may take its toll on the sales volumes.

Comments

Comments are closed for this article.