Archroma Pakistan Limited (PSX: ARPL) is a limited liability company which was previously known as Sandoz (1963-1995) and Clariant (1996–2013).

The principal activity of the company is the manufacturing, import and sale of chemicals, dyestuffs, coating, adhesives and sealants. It is also engaged in the indent business for textile, paper, adhesives, sealants, coating and construction industries.

ARPL is a subsidiary of Archroma Textiles Gmbh having its headquarters in Reinach, Switzerland.

Pattern of Shareholding

As of September 30, 2024, ARPL has a total of 34.563 million shares outstanding which are held by 1943 shareholders.

Archroma Textiles Gmbh (parent company) holds 75.32 percent of ARPL’s shares followed by local general public having a stake of 13.82 percent in the company. Around 4.97 percent of ARPL’s shares are held by Modarabas & Mutual Funds and 3.12 percent by Insurance companies. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

With the exception of 2020 and 2024, ARPL’s topline followed a growth trajectory in all the years under consideration. Conversely, its bottomline enhanced only in 2019 and 2021. ARPL posted net loss in 2024. The margins which had been deteriorating until 2020, posted a significant rebound in 2021 only to subside in the subsequent years. ARPL’s margins portrayed their lowest level in 2024. The detailed performance review of the period under consideration in given below.

In 2019, ARPL’s topline posted 21.43 percent year-on-year rise to clock in at Rs. 17,353.05 million. While sales volume remained depressed during the year due to sluggish market demand, the company was able to attain the topline growth by revising its price upwards and passing on the onus of cost increase to the customers. 33.1 percent of the sales were contributed by Paper & Packaging segment while Business line Brand & Performance textile accounted for 24.9 percent of the net sales in 2019.

Cost of sales grew by 22.87 percent year-on-year in 2019 due to inflation, Pak Rupee depreciation and increase in commodity prices in the international market. ARPL posted 18.32 percent year-on-year growth in its gross profit; however, GP margin slid from 31.62 percent in 2018 to 30.81 percent in 2019.

Distribution expense grew by 17.84 percent year-on-year in 2019 mainly due to tremendous rise in the royalty fee payable to Archroma Management Gmbh, an affiliated company of ARPL and also because of a hike in outward freight and handling charges on the back of high fuel charges.

Administrative expense rose by only 1.78 percent year-on-year in 2019 due to higher outside service charges incurred during the year. During the year, ARPL booked an impairment allowance of Rs.143.41 million which was 138.30 percent higher than the allowance booked in 2018.

Other expense also grew by 5.76 percent year-on-year in 2019 due to higher provisioning done for WWF and WPPF while other income slid by 32.89 percent during the year as no mark-up income was recognized from retirement benefit plan in 2019 unlike 2018.

Operating profit posted 19.22 percent year-on-year growth in 2019; however, OP margin posted a marginal downtick from 16.61 percent in 2018 to 16.3 percent in 2019. 58.22 percent year-on-year spike in finance cost was the result of higher discount rate and increased borrowings.

Net profit grew by 12.11 percent year-on-year to clock in at Rs.1722.38 million with NP margin of 9.93 percent in 2019 versus NP margin of 10.75 percent recorded in 2018. EPS grew from Rs.45.03 in 2018 to Rs.50.48 in 2019.

2020, scarred by COVID-19, resulted in 13.34 percent year-on-year drop in ARPL’s topline which clocked in at Rs.15,038.94 million. Its major customers operated at less than 50 percent capacity during the period due to lockdown, supply chain disruptions and demand contraction.

Cost of sales slid by 9.77 percent year-on-year in 2020, translating into 21.35 percent year-on-year dip in gross profit. GP margin plunged to 27.96 percent. Distribution expense posted 10 percent year-on-year slide in 2020 due to lower royalty charges and outward freight and handling charges.

Administrative expense continued to grow and posted 10.33 percent hike in 2020 mainly on account of market induced rise in salaries and wages while there was a drop in the number of employees from 284 in 2019 to 276 in 2020. Impairment allowance on trade receivables tremendously fell to Rs.13.18 million in 2020 as the company started the policy of cash collection over sales during the year.

Other expense shrank by 17.87 percent year-on-year in 2020 which was the result of lower provisioning for WPPF. Other income grew by 62.20 percent year-on-year in 2020 on the back of higher scrap sales. Despite keeping a check on expenses, lower sales volume pushed ARPL’s operating profit down by 30.19 percent year-on-year in 2020 with OP margin settling down to 13.14 percent.

Finance cost contracted by 35.43 percent year-on-year in 2020 due to lower discount rate, lesser exchange loss and a slump in short-term borrowings. Net profit plunged by 32.11 percent year-on-year in 2020 to clock in at Rs.1169.266 million with NP margin of 7.77 percent. EPS climbed down to Rs.34.27 in 2020.

ARPL’s net sales recovered by 32.14 percent year-on-year to clock in at Rs. 19,872.24 million in 2021. This came on the back of a staggering rise in sales volume as the major customers of ARPL i.e. Textile and Construction sector boasted tremendous growth on account of regional competitiveness, fiscal measures to boost textile exports and low-cost housing and infrastructure related projects initiated by the government. Increased demand also spurred upward price revision which also buttressed ARPL’s topline in 2021.

Cost of sales grew by 26.39 percent year-on-year in 2021 as the resumption in demand post-COVID resulted in supply chain delays due to non-availability of containers and vessels globally. This not only increased the cost and lead time of raw materials. ARPL managed to record 46.96 percent year-on-year surge in its gross profit with GP margin bouncing back to 31.10 percent in 2021.

Distribution expense piled up by 25.73 percent year-on-year in 2021 due to rise is sale volume which drove up outward freight and handling charges. Higher royalty fee paid to the holding company and higher payroll expense also contributed towards hefty distribution expense incurred in 2020. Administrative expense ticked up by 4.23 percent year-on-year in 2021 due to higher payroll expense.

During 2020, the company booked reversal on its trade receivables due to improved cash generation. This was on account of improved business sentiment as the signs of COVID-19 caved in. Other expense magnified by 120.39 percent year-on-year in 2021 due to higher provisioning for WWF and WPPF. Higher indenting commission, grant income and scrap sales drove other income up by 123.51 percent year-on-year in 2021.

Operating profit jumped up by 75.18 percent year-on-year in 2021 with OP margin growing up to 17.42 percent – the highest among all the years under consideration. Due to low discount rate and lesser borrowings on account of improved cash generation, finance cost tapered off by 38.15 percent year-on-year in 2021.

Net profit incredibly grew by 97.51 percent year-on-year in 2021 with OP margin mounting to 11.62 percent. EPS also grew to Rs.67.69 in 2021.

In 2022, ARPL’s net sales mustered 26.58 percent year-on-year rise to clock in at Rs.25,154.03 million.

The year began with a robust note with textile and construction sector attaining new highs, however, in the last quarter, both the sector started underperforming as political uncertainty, high energy and commodity prices, record high inflation, Pak Rupee depreciation as well as devastating floods during the year translated into demand compression, Cost of sales grew with an even higher magnitude of 30.97 percent due to the factors stated above, squeezing GP margin to 28.71 percent in 2022.

Distribution expense ascended by 31.47 percent year-on-year due to massive rise in royalty fee coupled with a hike in outward freight and handling on the back of higher fuel charges.

Administrative expense grew by 7.46 percent year-on-year in 2022 which was the consequence of higher payroll expense and outside service charges. The company also booked reversal of impairment allowance on trade receivables worth Rs.16.72 million in 2022.

Other expense nosedived by 1.21 percent year-on-year due to lower provisioning for WWF and WPPF booked in 2022 while other income grew by 1.83 percent due to higher indenting commission earned during the year.

Operating profit mounted by 10.67 percent year-on-year in 2022, however, OP margin dived to 15.23 percent. Finance cost gave a major blow to the bottomline as it surged by 155.10 percent year-on-year on account of hefty exchange loss, higher discount rate as well as increased short-term borrowings.

Sizeable growth in finance cost translated into 18.37 percent year-on-year decline in net profit in 2022 which stood at Rs.1885.064 million with NP margin of 7.5 percent. EPS also marched down to Rs.55.25 in 2022.

During 2023, textile and construction sector performance remained sluggish due to economic and political headwinds. ARPL’s topline posted 19.32 percent year-on-year rise to clock in at Rs.30,012.73 million. This was on the back of increased sales to textile effects and paper, packaging and coatings business.

High inflation and discount rate, steep depreciation in Pak Rupee, higher energy and commodity prices triggered by Russia-Ukraine conflict and devastating floods in the southern region of the country during the period resulted in 25.71 percent year-on-year hike in cost of sales in 2023. This resulted in a paltry 3 percent uptick in gross profit. GP margin tumbled to 24.88 percent in 2023. Distribution expense mounted by 18.15 percent during 2023 due to elevated royalty charges and outward freight & handling charges incurred during the year.

Administrative expense surged by 22.36 percent in 2023 due to higher outside service charges, legal & professional charges as well as repair & maintenance charges. Other expense slumped by 25.96 percent due to lower profit related provisioning made during the year. Other income also shrank by 27 percent in 2023 due to lower indenting commission, lesser scrap sales and no grant income recorded during the year.

Operating profit nosedived by 8.54 percent in 2023 with OP margin marching down to 11.67 percent. Finance cost mounted by 82.14 percent in 2023 due to unprecedented level of discount rate on account of hefty exchange loss and significant rise in short-term borrowings. Net profit declined by 34 percent in 2023 to clock in at Rs.1244.382 million with EPS of Rs.36.47 and NP margin of 4.15 percent.

In 2024, ARPL posted year-on-year slide of 17.46 percent in its topline which clocked in at Rs.24,773.12 million. This was because the main consumption sectors of the company i.e. Textiles, Construction and Consumer sales remained lackluster in 2024 – both in the local and export markets.

Revenue proceeds from textile effects tumbled by 20 percent to clock in at Rs.21,203 million in 2024. Conversely, revenue from packaging technologies posted an uptick of 3 percent to clock in at Rs.3,570 million in 2024.

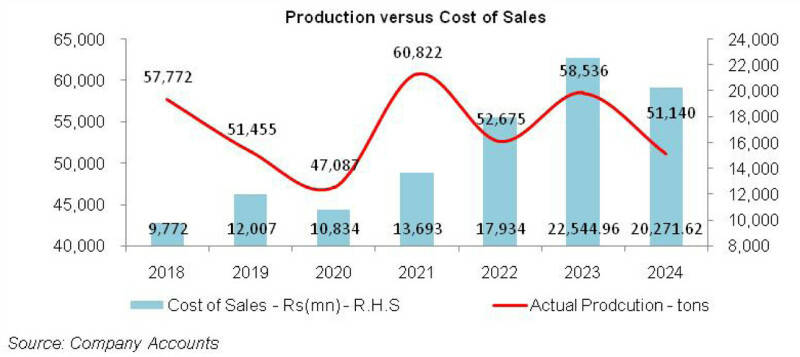

In view of demand destruction, ARPL’s production dropped from 58,536 tons in 2023 to 51,140 tons in 2024. Cost of sales dipped by only 10 percent due to elevated cost of imported raw materials, high energy cost and lesser absorption of fixed cost. This coupled with the company’s inability to pass on the impact of cost hike to its customers due to lower demand resulted in 39.72 percent year-on-year decline recorded in gross profit in 2024 with GP margin hitting its lowest level of 18.17 percent.

Distribution expense slid by 2.17 percent in 2024 due to lower royalty payment as well as outward freight & handling charges incurred during the year. Administrative expense surged by 19.32 percent in 2024 due to higher outside service charges and increased payroll expense which was the effect of inflationary pressure as well as workforce expansion from 253 employees in 2023 to 261 employees in 2024.

Unlike last three years, where the company was booking reversals on impairment loss on trade receivables, this year around, ARPL booked impairment loss of Rs.44.98 million on its trade receivables. Other expense dwindled by 89 percent in 2024 as the company didn’t book any profit related provisioning during the year.

Other income strengthened by 302.65 percent in 2024 mainly on account of indenting commission. ARPL recorded 79.69 percent thinner operating profit in 2024 with OP margin falling down to 2.87 percent. Finance cost dipped by 3 percent in 2024. This was mainly due to exchange gain recorded in 2024 versus exchange loss recorded in the previous year.

Lesser utilization of working capital lines also contributed in driving the finance cost down despite exceptionally high borrowing rates prevailing during the year. ARPL posted net loss of Rs.546.452 million in 2024 with loss per share of Rs.15.81.

Recent Performance (6MFY25)

During the half-year period of the ongoing fiscal year, ARPL’s net sales ticked up by 2.5 percent to clock in at Rs.14,638.31 million. This was due to an uptick recorded in revenue proceeds from textile effects in both domestic and export markets.

Conversely, sales proceeds from packaging technologies registered a decline during the period. Textile and construction sectors which are the main customers of ARPL began showing signs of improvement in the second quarter of FY25.

Market driven changes implemented in the sales mix as well as cost optimization measures implemented during the year resulted in 25.73 percent improvement in gross profit recorded during the period with GP margin clocking in at 23 percent in 6MFY25 versus GP margin of 18.76 percent recorded in 6MFY24.

Distribution expense ticked up by 10.22 percent in 6MFY25 due to improved sales volume. Administrative expense also surged by 9.46 percent due to inflationary pressure and rebound in the company’s operations. Other expense mounted by 696.80 percent in 6MFY25 seemingly due to higher profit related provision booked during the period.

However, it was offset by 80.10 percent stronger other income recognized during the period which might be due to higher indenting commission. ARPL’s operating profit strengthened by 73.34 percent in 6MFY25 with OP margin clocking in at 7.64 percent versus OP margin of 4.52 percent recorded during the same period last year.

Monetary easing as well as reduced utilization of working capital lines due to improved liquidity conditions enabled the company to drive down its finance cost by 59.80 percent in 6MFY25. ARPL recorded net profit of Rs.634.199 million with EPS of Rs.18.35 in 6MFY25 versus net loss of Rs.121.171 million and loss per share of Rs.3.62 registered in 6MFY24. NP margin was recorded at 4.33 percent in 6MFY25.

Future Outlook

The local macroeconomic scenario has significantly improved off-late, providing impetus for robust local sales. However, import tariffs imposed by the US government may take its toll on the export sales of the company.

On the positive side, the tariffs imposed put Pakistan at a competitive advantage versus its regional peers and provide our local industry with an opportunity to grab the market share from India, Bangladesh and Vietnam.

Comments

Comments are closed for this article.