It is not a crisis. It is not a question of food security. It is not about protecting domestic producers or defending forex reserves. Pakistan’s sugar muddle, as always, is simply the outcome of a policy regime built to reward rent-seeking. From seasonal traders to opportunist processors to ever-pliable public sector functionaries, everyone knows how to play this game—and no one wants the game to end.

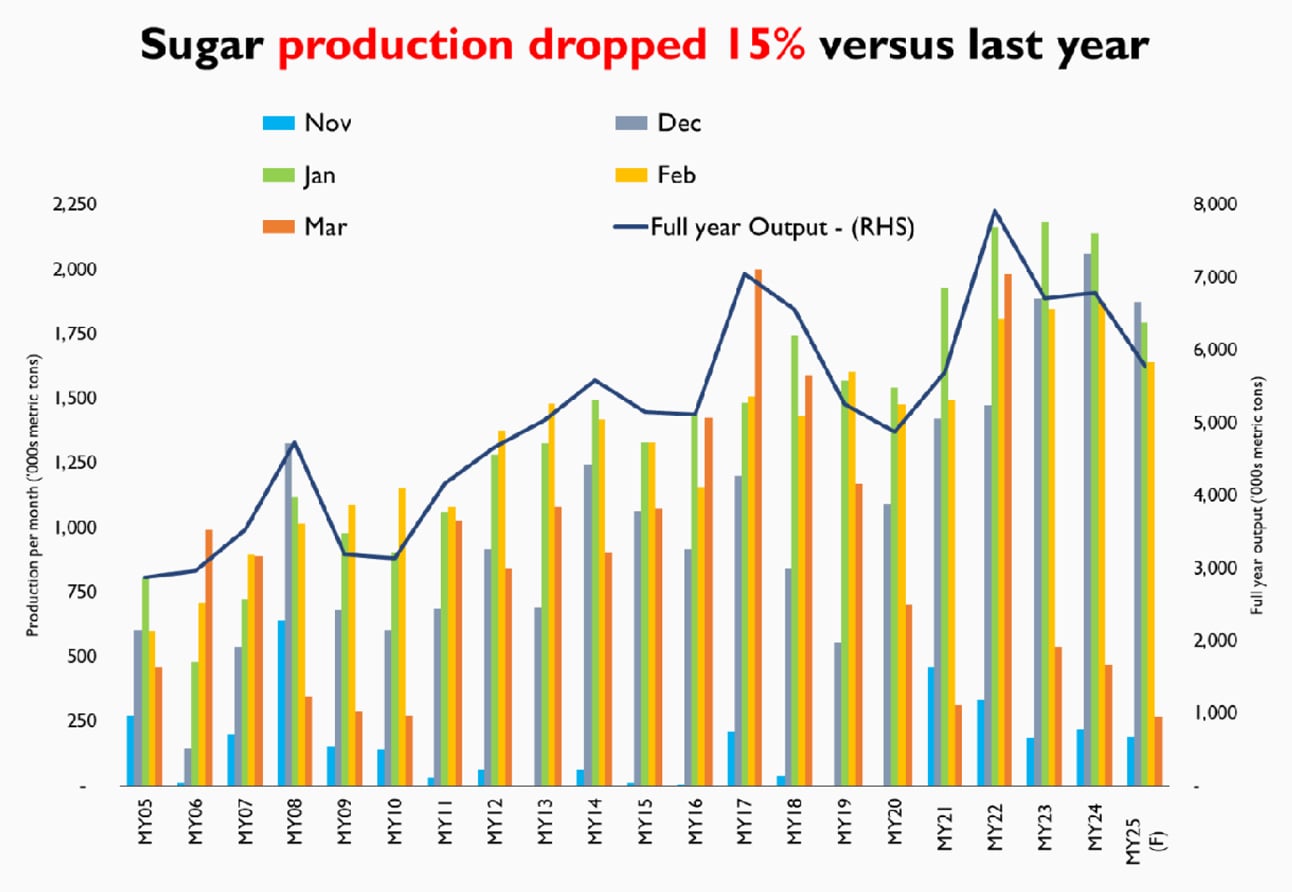

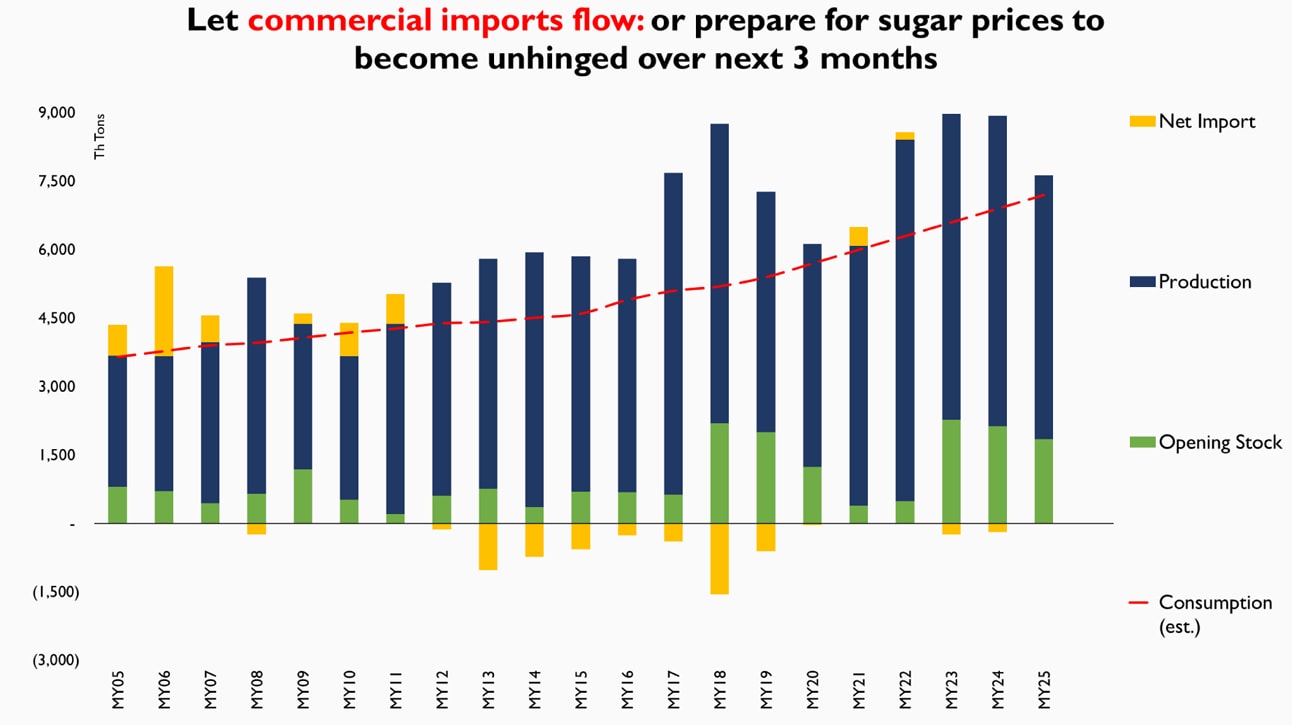

For the current marketing year, sugar output is forecast to clock in at 5.8 million metric tons—lowest in four years. Even if one assumes consumption growth at a modest 4 to 5 percent annually, the supply shortfall is evident. Yet mills appear unbothered.

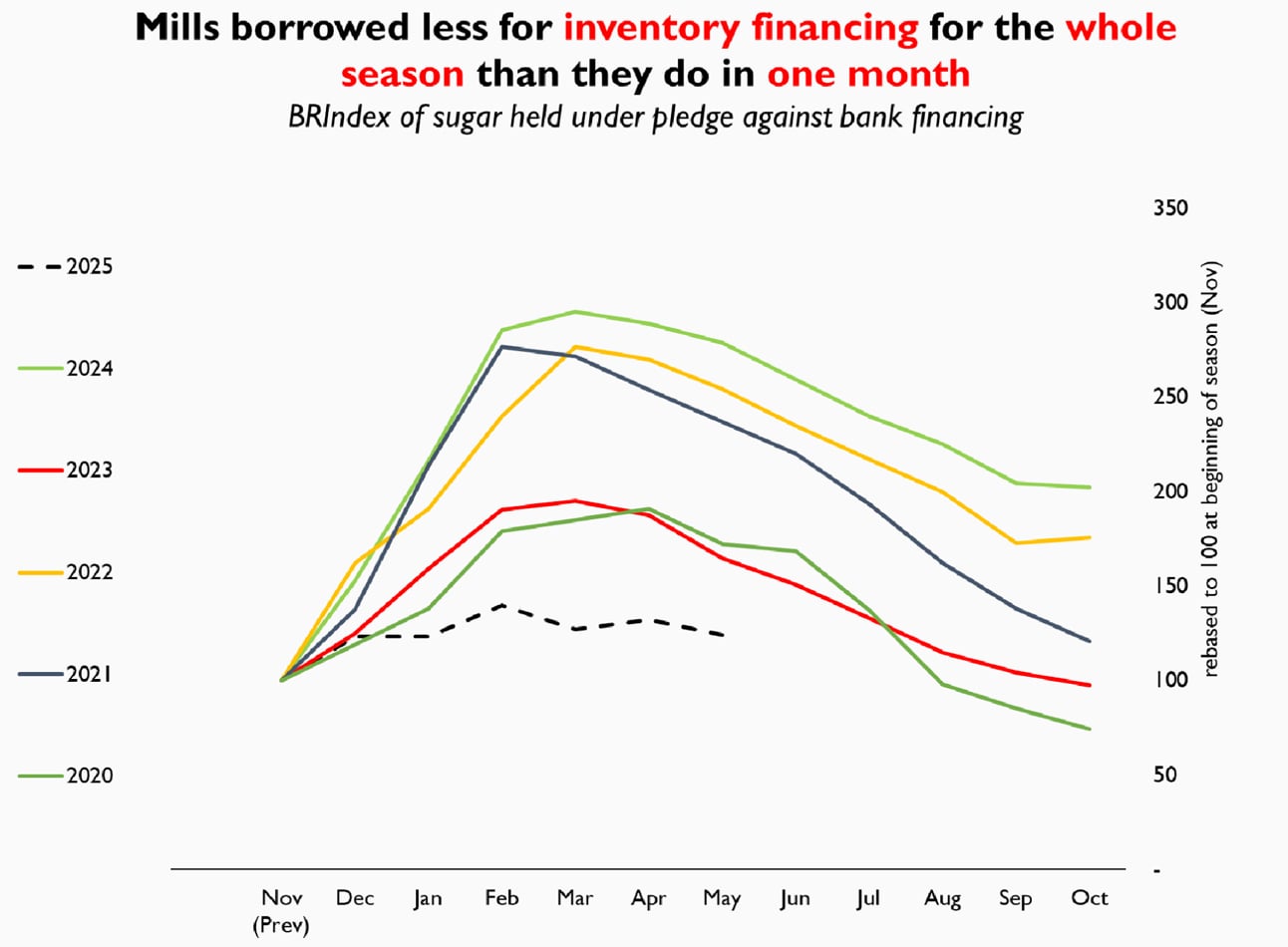

There has been no scramble for seasonal financing, no surge in bank borrowings against pledged stock, no build-up of commercial inventories. In fact, sugar inventory under bank pledge during peak crushing season was lower than in October, when stocks usually hit rock bottom. Which suggests only one thing: buyers had enough cash on hand to mop up available volumes off-book, off-ledger, and off the state’s radar.

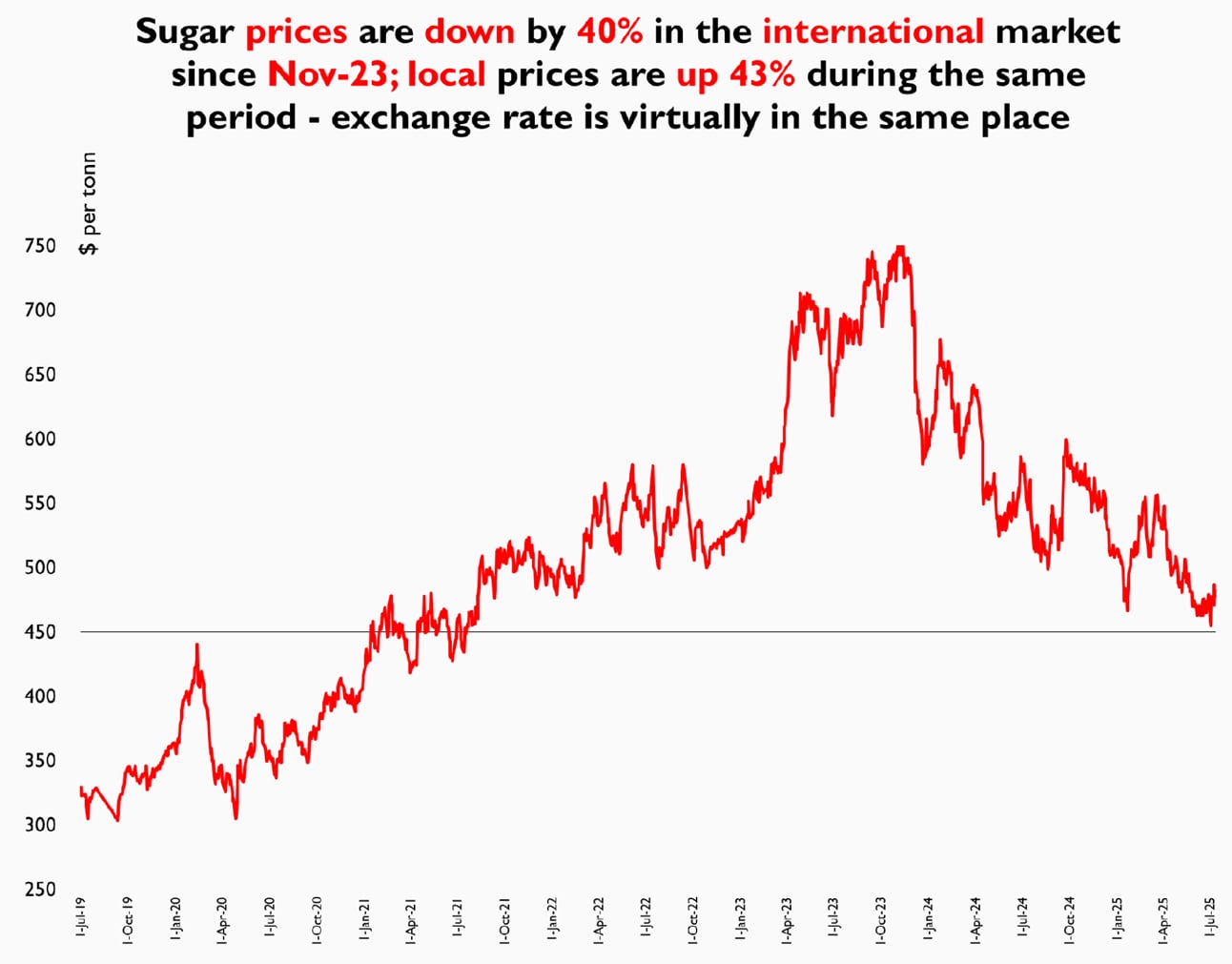

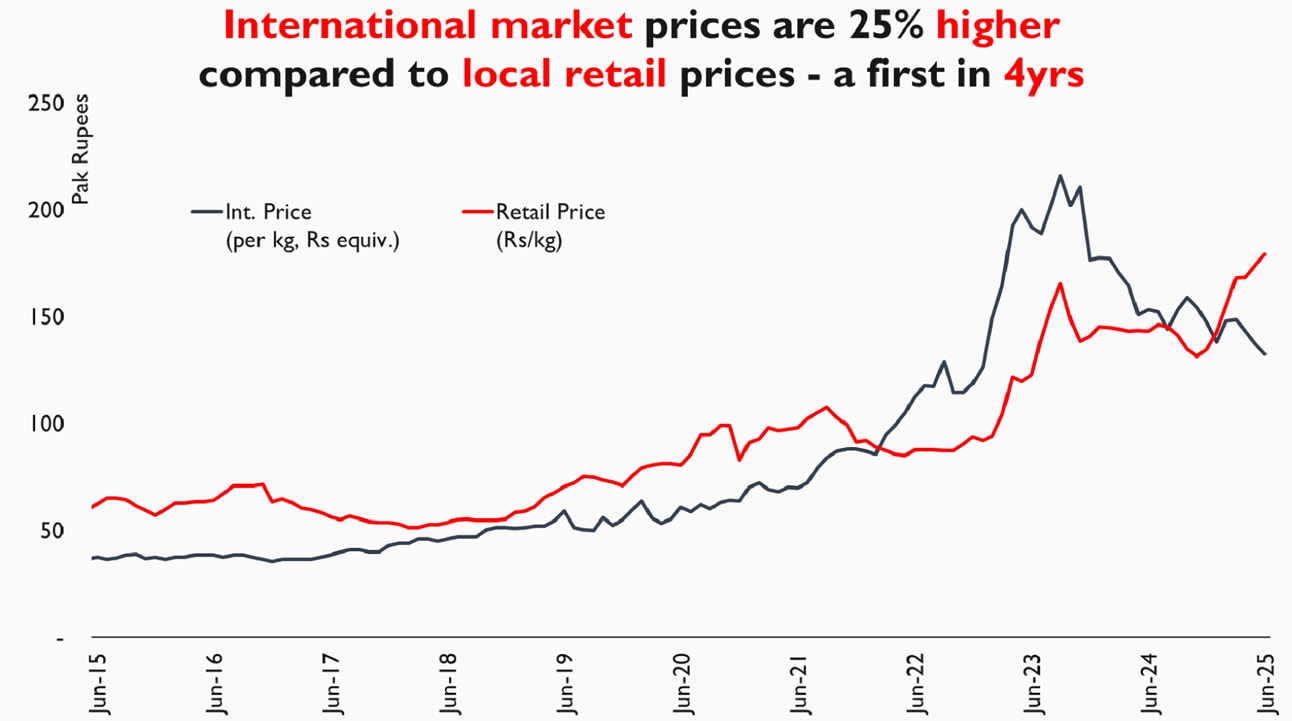

Meanwhile, international prices have collapsed—down over 40 percent since November last year—while domestic retail prices have gone the other way, rising more than 40 percent over the same period. The rupee is roughly where it was. The implication is clear: import parity is now well below domestic market prices. That should have triggered a wave of private commercial imports by now. It has not.

Why? Because the trade regime is designed not to facilitate trade, but to centralize permissions. Commercial importers require approvals, access to LC limits, clarity on duties, and certainty that the rug won’t be pulled out mid-voyage. Instead, they are being told to wait for a government tender—another state-run procurement process that will inflate prices, delay arrivals, and crowd out the private sector. Traders have seen this movie before.

The irony, of course, is that even when the state is not in the market, it still sets the rules so no one else can enter freely. Export quotas are issued in fits and starts, often reversed overnight. Import permissions are granted on political whim. Duties are tweaked to favour whoever is in favour. What passes for policy is really just orchestrated uncertainty.

This is not how market economies work. Sugar is not a strategic commodity. It is not a staple. It is not essential for national nutrition. It is simply a value-added cash crop with a large and politically networked lobby.

The best way to defang it is not to subsidize it, not to stockpile it, and not to manage it through tenders and quotas—but to walk away. Open up the trade regime. Allow imports and exports to flow freely, at zero duty and without discretionary licensing. Let market participants hedge their risks, and bear their own consequences.

Because when regulation exists only to be gamed, deregulation is not ideological. It is practical.

Comments

Comments are closed for this article.