Nepra has approved a reduction of Rs1.15 per unit in the base tariff for all non-lifeline consumers. The cut implies a base tariff relief of 2 to 5 percent for non-protected consumers, and 8 to 10 percent for those in the protected category. Negative base tariff adjustments are uncommon, offering a rare break after an extended spell of steep increases.

The reduction in base tariff is not the main story. What ultimately matters is the effective end-user tariff — where a mix of adjustments, surcharges, and taxes often carries more weight, particularly when the base tariff revision is modest, as is the case this time.

Significant confusion persists around the continuation of the previously announced Rs7.4 per unit relief into FY26. The issue was raised during the tariff hearing, but the Ministry of Energy’s response did little to resolve the uncertainty.

The Ministry stated that the “average applicable consumer tariff in July 2025 would be lower by around seven rupees as compared to July 2024” — a phrasing that, while seemingly affirmative, raises more questions than it answers, especially in the absence of clarity on the underlying assumptions and whether the relief refers to gross billing impact or base tariff trajectory alone.

It is important to recall that much of the previous quarter’s relief was temporary by design, intended to lapse by June 2025. The only component explicitly extended into FY26 was the Rs182 billion relief — equivalent to Rs1.7 per unit — financed through additional Petroleum Levy collections. In its communication with the IMF, the government had clearly stated that this limited subsidy for all non-lifeline consumers would remain in place only until June 30, 2026.

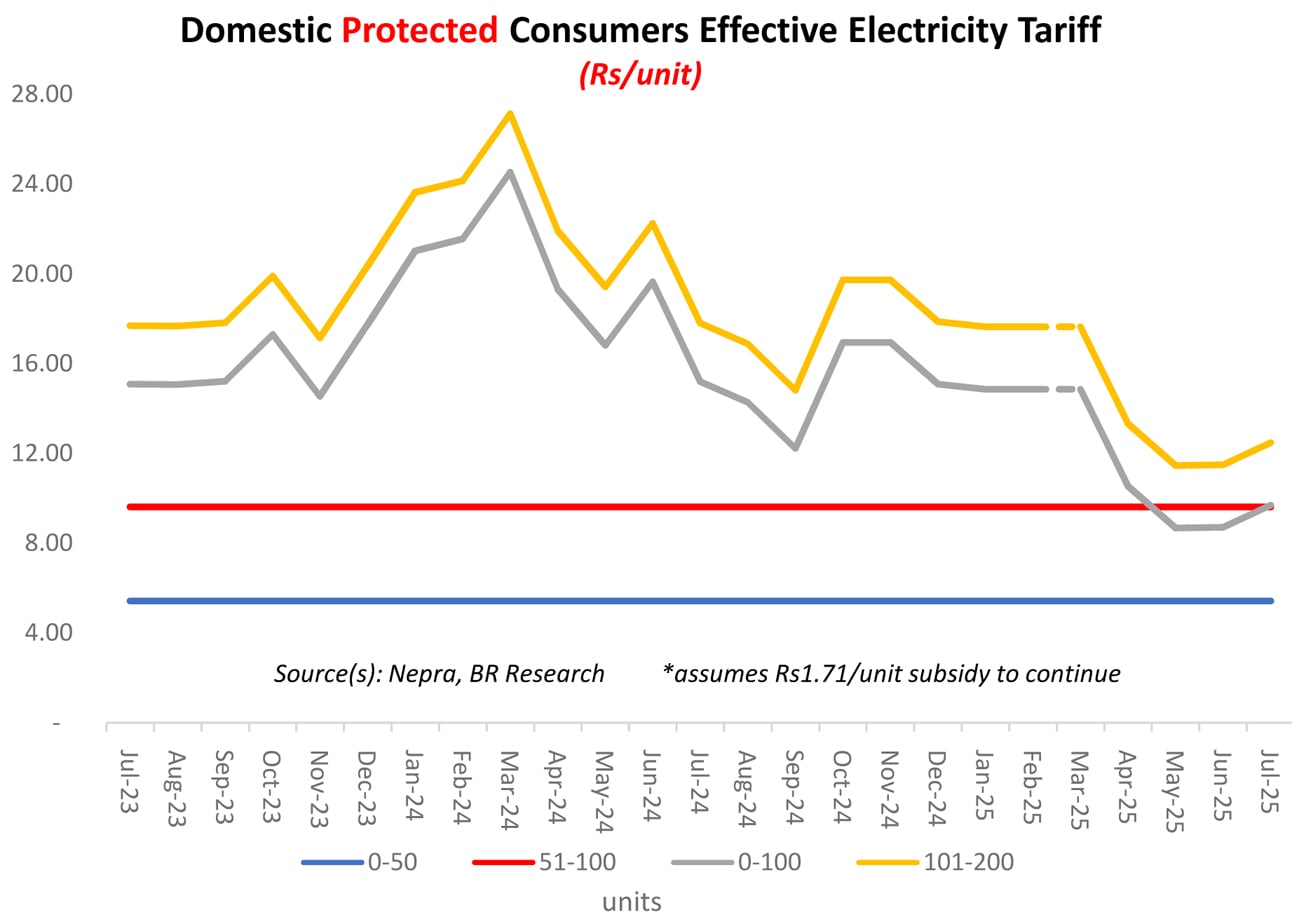

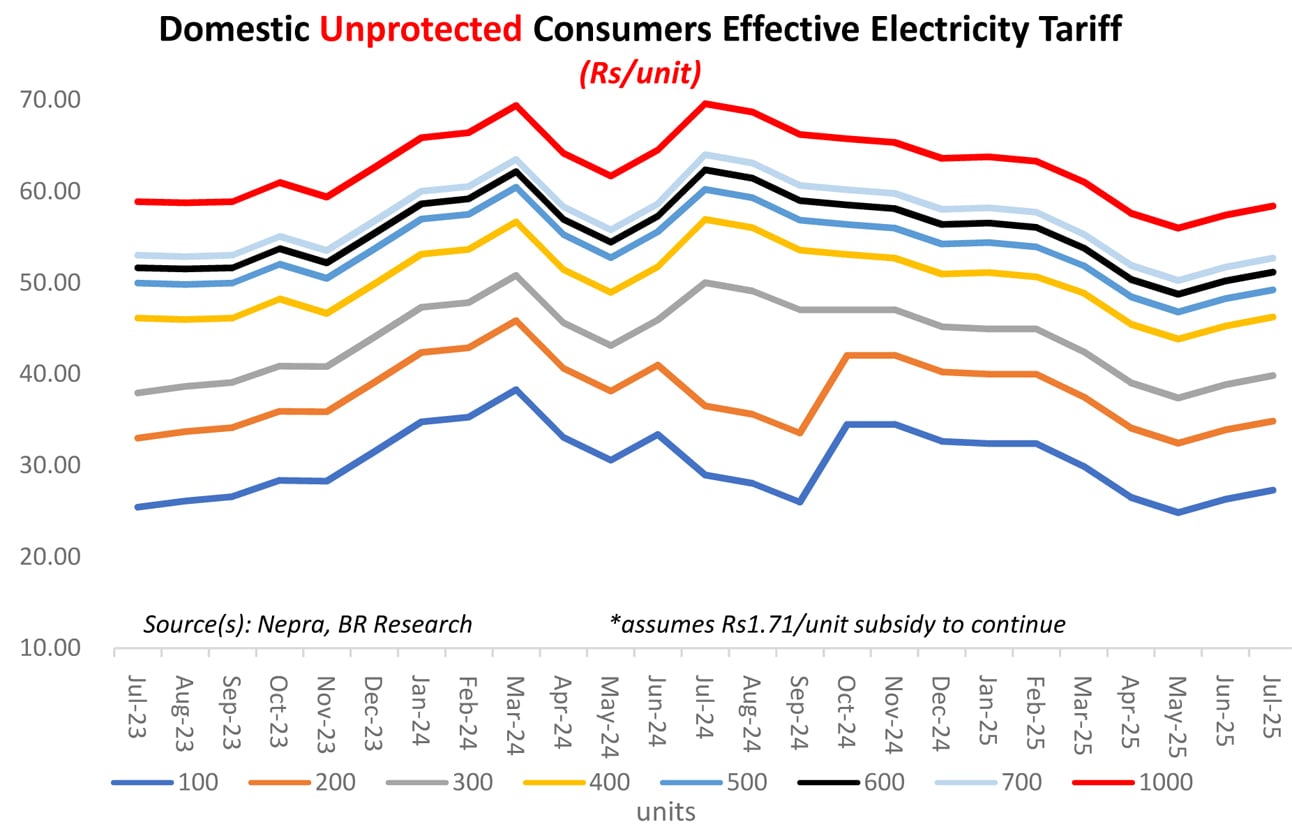

Combining the Rs1.15 per unit base tariff reduction with the Rs1.7 per unit Petroleum Levy–financed subsidy brings the total relief for July 2025 to Rs2.8 per unit. However, the most significant contributor is the Fuel Charge Adjustment (FCA), which has dropped from Rs3.2 per unit in July 2024 to around 10 paisas — a major swing. Additionally, quarterly tariff adjustments (QTA) offer further relief of Rs2.5 per unit, as the current QTA is a negative Rs1.55 per unit, compared to a positive Rs0.93 per unit last July. It’s worth recalling that effective electricity tariffs for all consumer slabs had peaked in July 2024.

Despite the base tariff cut, effective tariffs are set to increase by Re1 per unit on a month-on-month basis — primarily due to the quarterly adjustment becoming less negative, narrowing from Rs3.45 to Rs1.55 per unit. With this periodic negative adjustment scheduled to lapse after July 2025, the year-on-year relief in effective tariffs will also diminish as FY26 progresses.

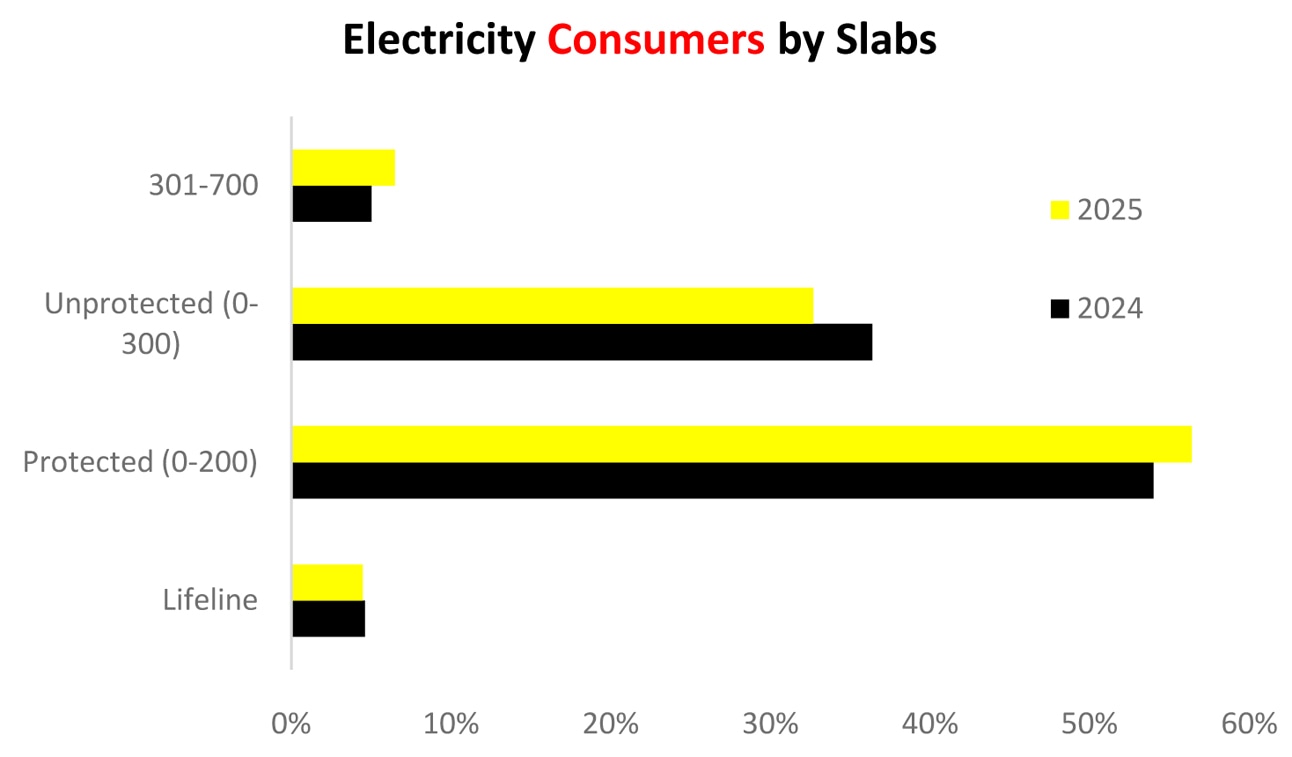

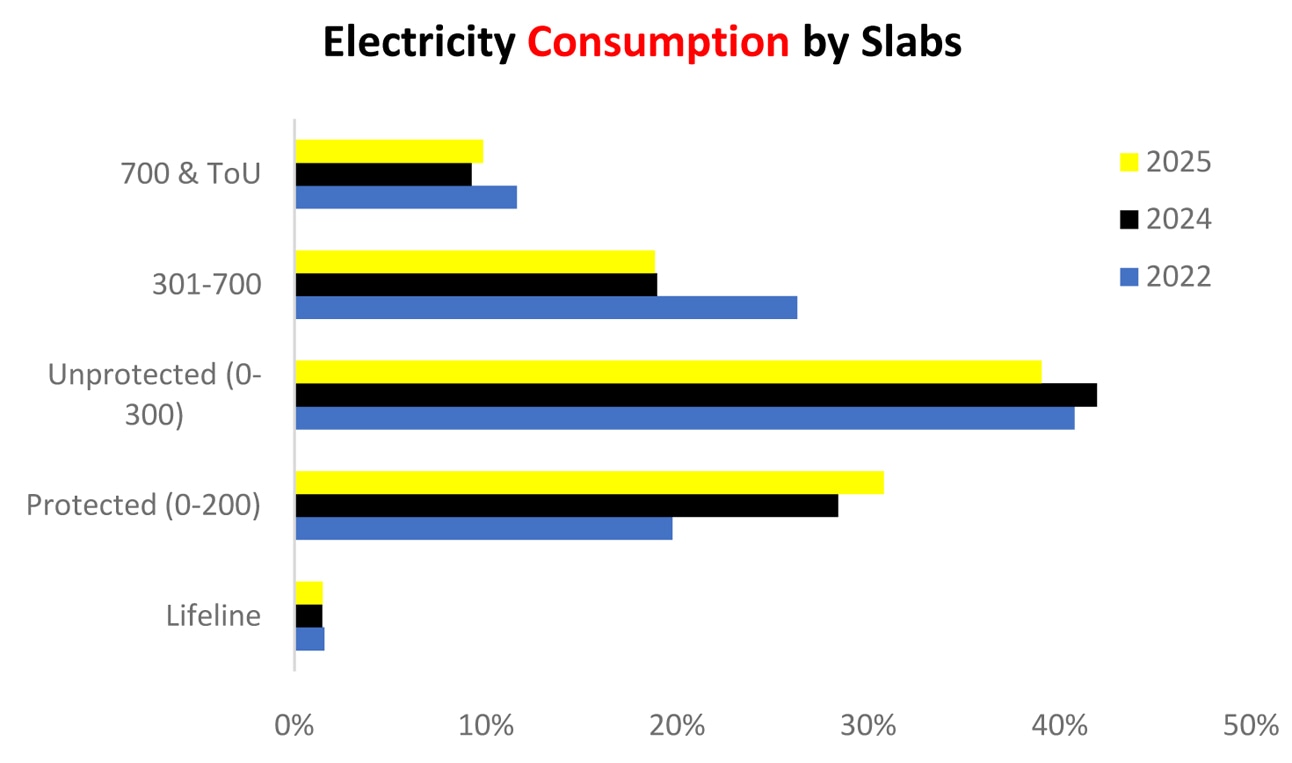

The more fundamental shift is unfolding in consumption patterns. An estimated 3.5 million additional consumers are expected to move into the protected category in FY26 compared to FY25. Today, 60 percent of all domestic consumers fall under protected or lifeline slabs — up from 50 percent just three years ago. Their share in total domestic consumption has risen from 22 percent in FY22 to 32 percent now.

In contrast, consumption in the unprotected category — primarily middle and lower-middle income households — has declined sharply. The 301–700 unit slab has seen a drop of 5 billion units over three years, with its share in domestic consumption falling from 26 to just 19 percent. Despite lower tariffs compared to last year, the shift appears structural. Erosion in purchasing power has pushed millions into protected categories, shielding them from steep tariffs — but at the cost of mounting pressure on those left behind to cross-subsidize.

The shift also mirrors the acceleration of solar adoption. In many remote areas, the grid is becoming increasingly redundant. Solar uptake is now evident across commercial, agricultural, and industrial segments as well. Meanwhile, uncertainty around net metering policy continues. Without clarity, the burden will keep growing on mid-tier unprotected consumers still tied to the grid.

Comments

Comments are closed for this article.