Feroz1888 Mills Limited (PSX: FML) was incorporated in Pakistan as a public limited company in 1972. The company is in the business of manufacturing and exporting specialized yarn and textile products categorized into bath, beach and kitchen products. Besides having an export market in over ten countries across the globe, FML also caters to the needs of local market. The company is partnered with 1888 Mills (USA) and has its manufacturing units in Sindh and Balochistan.

Pattern of Shareholding

As of June 30, 2024, FML has a total of 399.409 million shares outstanding which are held by 1084 shareholders. Individuals have the majority stake of 35.58 percent in FML followed by Directors, CEO and their spouse holding 32.38 percent shares.

Associated companies, undertakings and related parties account for 30.17 percent shares of FML while joint stock companies hold 1.77 percent of FML’s outstanding shares. The remaining shares are held by other categories of shareholders.

Performance Trail (2019-2024)

FML’s topline has posted growth in all the years under consideration. Conversely, its bottomline slid twice during the period i.e. in 2020, 2022 and 2024. FML’s margins which peaked in 2019 plunged for the next three years except for a trivial uptick in operating and net margins in 2021. In 2023, the margins staggeringly rebounded which was followed by a drastic fall in 2024. The detailed performance review of the period under consideration is given below.

In 2019, FML’s topline posted a tremendous 34.58 percent year-on-year growth to clock in at Rs.29,348.44 million. The growth was mainly backed by export sales which grew by 9 percent year-on-year in USD terms and 34.6 percent year-on-year in Pak Rupee terms to clock in at Rs.28.55 billion. Local sales also posted 21 percent year-on-year growth but in absolute terms, they are much lower than export sales i.e. Rs.395.16 million in 2019.

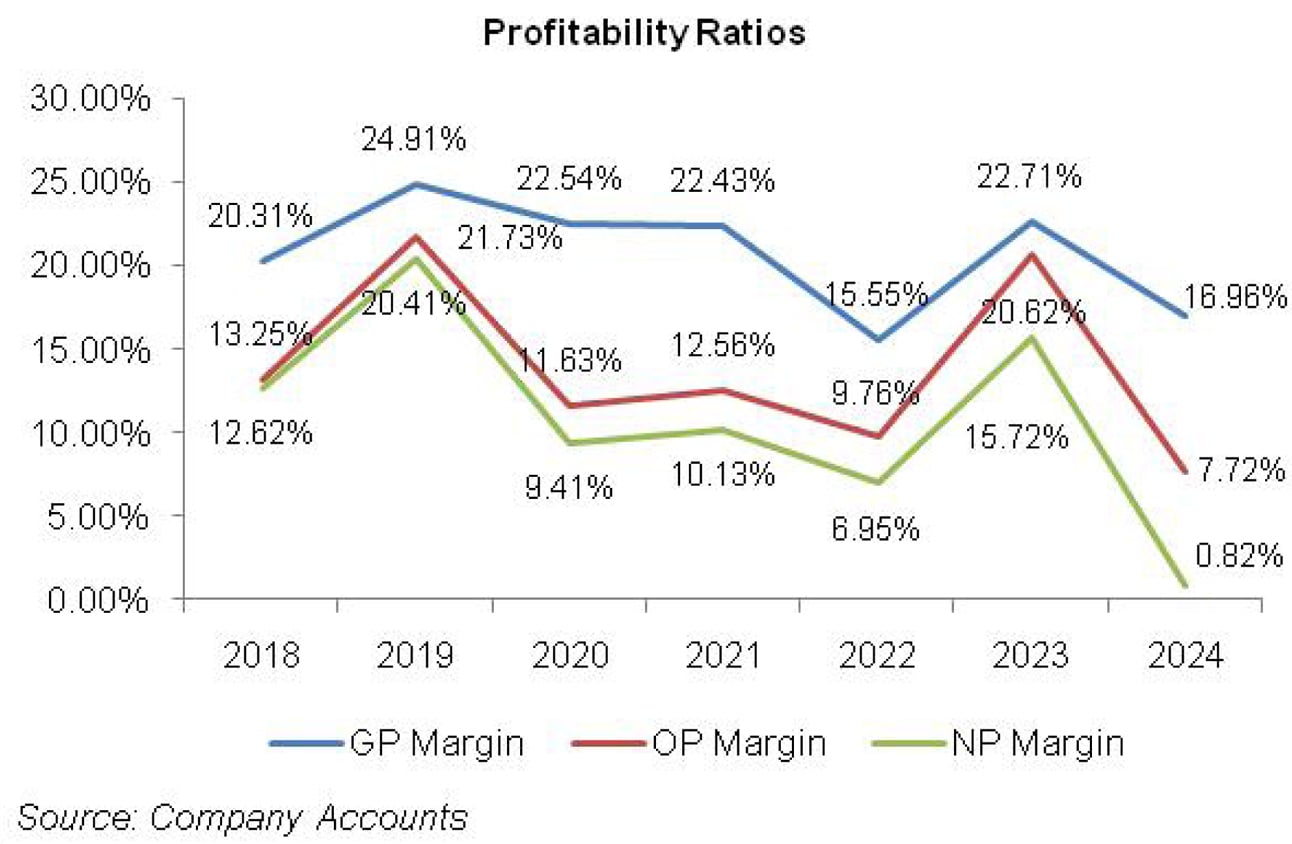

While cost of sales also grew in the wake of inflationary pressure, gross profit grew by 65 percent year-on-year with GP margin clocking in at 24.91 percent in 2019 as against GP margin of 20.31 percent recorded in the previous year. Operating expenses continue to enlarge with major outlay recorded in the category of advertising and marketing expense. Other expense grew by 68 percent year-on-year in 2019 on account of increased profit related provisioning.

However, other income completely wiped it off with a significant growth of 185 percent year-on-year recorded in 2019. This was on the back of considerable exchange gain earned on export receivables. As a result, operating profit grew by 120.67 percent in 2019 with OP margin clocking in at 21.73 percent as against OP margin of 13.25 percent posted in the previous year. Finance cost rose by 81.84 percent year-on-year in 2019 because of high discount rate coupled with increased borrowings during the year.

FML secured a huge amount of both long-term financing for the import of machinery as well as short-term financing as export refinance facilities during the year. As a consequence, FML’s gearing ratio grew from 30.15 percent in 2018 to 34.51 percent in 2019.

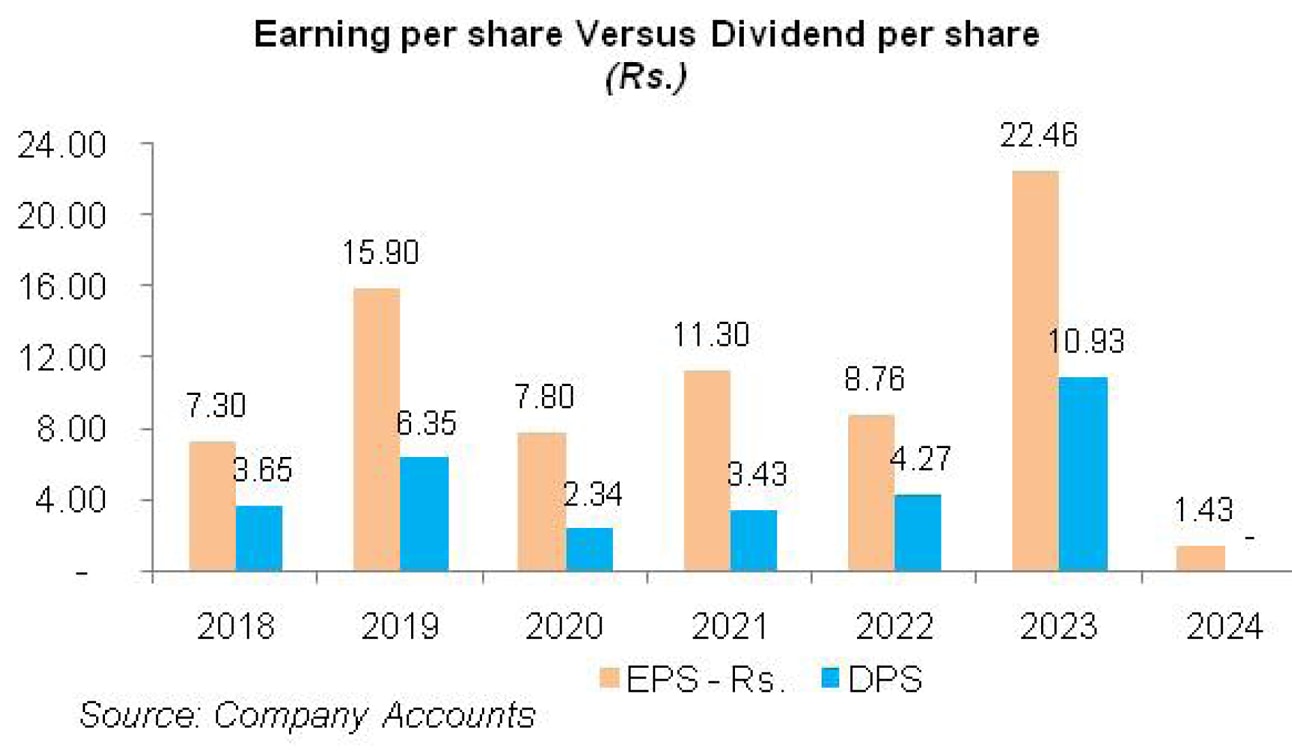

The bottomline boasted a year-on-year growth of 117.65 percent in 2019 to clock in at Rs.5,989.81 million with EPS of Rs.15.90 as against EPS of Rs.7.30 registered in the previous year. NP margin stood at 20.41 percent in 2019 as against NP margin of 12.62 percent recorded in the previous year.

As against the new highs achieved by the company in 2019, 2020 was a sluggish year for FML. Both local and export sales came to a halt due to lockdown imposed locally as well as in the major export destinations of FML during the second half of FY20. 6.33 percent year-on-year growth in net sales was mainly attributable to exchange rate difference during the year. FML’s net sales clocked in at Rs. 31,205.68 million in 2020.

Cost of sales gave no respite as inflationary pressure pushed up the cost of raw materials, fuel and power charges etc. Gross profit slid by 3.78 year-on-year with GP margin clocking in at 22.54 percent in 2020.

Administrative and distribution expenses grew by 13.76 percent and 12.20 percent respectively during the year. The main growth drivers were marketing expense as well as payroll expense. FML expanded its workforce from 11,255 employees in 2019 to 11,971 employees in 2020. FML’s bottomline was hit hard by other expense which grew by 87.21 percent year-on-year in 2020 mainly on the back of exchange differences on export receivables, trade payables and derivative financial instruments.

FML also made provisioning for doubtful receivables during the year. Other income didn’t support either and dropped by 89.31 percent year-on-year in 2020 as exchange gains were zeroed by exchange losses. FML’s operating profit plunged by 43 percent year-on-year with OP margin standing at 11.63 percent in 2020.

Finance cost grew by 122.56 percent in 2020 as discount rate was high during the first three quarters of FY20. This coupled with increased short-term and long-term borrowings and lease liabilities jacked up FML’s gearing ratio to 48.23 percent in 2020. Consequently, bottomline shrank by 50.96 percent year-on-year in 2020 to clock in at Rs. 2937.22 million with EPS of Rs. 7.80 and NP margin of 9.41 percent.

2021 was a vigorous year for FML, characterized by 36.43 percent year-on-year topline growth coming on the back of both local and export sales. FML’s net sales clocked in at Rs.42,575.47 million in 2021. The US market represented the major export destination for the company with a share of 83 percent in the net sales of FML in 2021. Increased yarn prices, Pak Rupee depreciation, hike in fuel and power cost etc took its toll on the cost of sales which grew by 36.62 percent year-on-year in 2021.

While gross profit enhanced by 35.78 percent in 2021, GP margin dropped to 22.43 percent. Operating expense grew mainly on account of marketing expense, freight, forwarding and insurance charges and also because of higher payroll expense as number of employees grew to 13,354 in 2021.

Other income and other expense gave some breather as the company reversed the provision for doubtful advances and also because of higher dividend income on open ended mutual fund units.. Operating profit grew by 47.29 percent year-on-year with OP margin clocking in at 12.56 percent in 2021. Finance cost continued to grow despite slashed discount rate as the company’s long-term and short-term borrowings as well as lease liabilities enlarged during the year which also drove its gearing ratio up to 51.33 percent in 2021.

FML’s bottomline posted 46.78 percent year-on-year growth in 2021 to clock in at Rs.4311.29 million with EPS of Rs. 11.30 and NP margin of 10.13 percent.

2022 was a difficult year not only for the textile sector but for the economy as a whole. Soaring inflation, sharp depreciation of Pak Rupee, multiple upward revisions in discount rate coupled with import restrictions and subdued purchasing power of consumers were the challenges that began to raise their heads in 2022 and continued even in 2023.

The topline of FML grew by 15.13 percent year-on-year to clock in at Rs.49,018.46 million in 2022. The topline couldn’t sustain the rise in cost of sales due to the challenges quoted above. As a result gross profit took 20.18 percent year-on-year plunge in 2022 with GP margin drastically falling down to 15.55 percent. The company had never seen such a thin GP margin since 2014.

Administrative and distribution expenses multiplied by 12.50 percent and 25.50 percent respectively in 2022. This was on the back of elevated freight charges and higher payroll expense despite the fact that FML’s workforce shrank to 12,643 employees in 2022. Other income gave major support to the bottomline as it multiplied by 638 percent in 2022 on the back of hefty exchange gain.

Other expense also slumped by 55.85 percent in 2022 due to no exchange losses incurred during the year coupled with lower profit related provisioning done in 2022. Operating profit eroded by 10.50 percent year-on-year in 2022 with OP margin clocking in at 9.76 percent. Finance cost grew by 19.17 percent year-on-year in 2022 on the back of multiple rate hikes during the year as well as increased borrowings.

However, increased share capital due to issue of right shares resulted in a lower gearing ratio of 43 percent in 2022. FML’s bottomline dropped by 20.94 percent year-on-year in 2022 to clock in at Rs.3408.45 million with EPS of Rs.8.76 and NP margin of 6.95 percent.

During 2023, FML’s topline registered 16.39 percent year-on-year growth to clock in at Rs.57,051.83 million. The main reason behind higher net sales was 45 percent depreciation of Pak Rupee resulting in tremendous exchange gain. Elevated proportion of export sales in the total sales mix of FML coupled with Pak Rupee depreciation conveniently absorbed the cost of sales, resulting in 69.94 percent higher gross profit recorded by the company in 2023. GP margin climbed up to 22.71 percent in 2023.

Administrative expense hiked by 50.63 percent year-on-year in 2023 on account of higher payroll expense as FML hired additional resources to take its workforce up to 13,127 employees in 2023. Higher travelling & conveyance charges also contributed towards elevated administrative expense recorded by the company in 2023. Distribution expense also grew by 3.90 percent in 2023 due to higher marketing and other related expenses incurred during the year. 107.55 percent spike in other expense in 2023 was the result of higher provisioning for WWF, WPPF and ECL.

However, it was nullified by a tremendous other income of Rs.4721.34 million recorded by FML in 2023 due to robust exchange gain and dividend income. Operating profit mounted by 145.85 percent year-on-year in 2023 with OP margin of 20.62 percent. Finance cost magnified by 199.23 percent in 2023 due to unprecedented level of discount rate coupled with increased short-term borrowings. Gearing ratio also picked up to 52.19 percent in 2023. FML posted 163.15 percent taller net profit to the tune of Rs. 8969.46 million in 2023 with EPS of Rs.22.46 and NP margin of 15.72 percent.

In 2024, FML’s topline picked up by 22.27 percent to clock in at Rs.69,757.60 million. As of June 30, 2024, export sales comprised of 96.62 percent of FML’s net sales. Export sales showed great resilience and mounted by 21.83 percent in 2024. This mainly encompassed sales to America and European region. Cost of sales surged by 31.36 percent in 2024 due to elevated energy and gas prices. This coupled with the stability portrayed by Pak Rupee during the year, squeezed the margins on export sales. This resulted in 8.67 percent downtick recorded in gross profit in 2024. GP margin also fell to 16.96 percent in 2024.

Administrative expense surged by 14.79 percent in 2024 on the back of higher payroll expense, elevated utility charges as well as greater conveyance & travelling charges incurred during the year. FML expanded its workforce from 10,908 employees in 2023 to 12,483 employees in 2024.

Distribution expense mounted by 22.21 percent in 2024 due to higher marketing budget as well as freight & insurance charges incurred during the year. Other expense ticked down by 0.60 percent in 2024 as considerably lesser profit related provisioning done during the year was greatly offset by hefty net exchange loss. Other income also fell by 88.24 percent in 2024 as FML didn’t record any exchange gain.

Operating profit tapered off by 54.25 percent in 2024 with OP margin registering its lowest level of 7.72 percent. Finance cost escalated by 92.65 percent in 2024 due to higher discount rate and increased short-term borrowings. This resulted in a gearing ratio of 57.84 percent in 2024. FML’s net profit eroded by 93.62 percent to clock in at Rs.572.341 million in 2024. This translated into EPS of Rs.1.43 and NP margin of 0.82 percent in 2024.

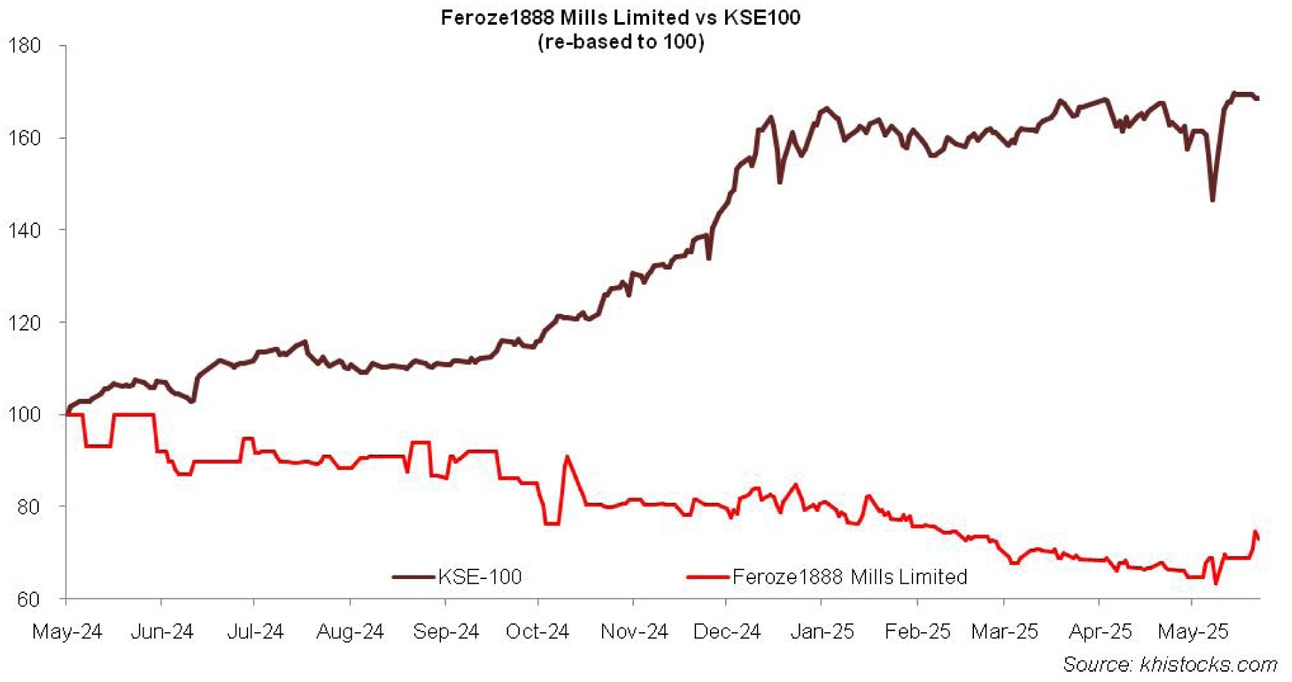

Recent Performance (9MFY25)

During the nine-month period of the ongoing fiscal year, FML’s net sales narrowed down by 10.49 percent to clock in at Rs.47,329.49 million. This was due to increased competition and high recession in the international market. Stronger Pak Rupee also reduced the value of the company’s exports in terms of local currency. This coupled with higher cost of sales due to elevated energy tariff resulted in 30.30 percent decline in gross profit in 9MFY25. GP margin also fell from 17.76 percent in 9MFY24 to 13.83 percent in 9MFY25.

Administrative expense ticked up by 8.55 percent in 9MFY25 due to inflationary pressure which pushed up the payroll expense. Conversely, tighter export sales resulted in 17.10 percent downtick recorded in distribution expense during the period. Lesser provisioning done for WWF and WPPF resulted in 90.48 percent decline in other expense in 9MFY25. However, it was offset by 266.39 percent growth recorded in other income during the period which came on the back of hefty replenishment income of Rs.658.799 million recorded during the period.

FML’s operating profit slumped by 28.45 percent in 9MFY25 with OP margin dipping to 6.10 percent versus OP margin of 7.63 percent recorded in 9MFY24. Finance cost thinned down by 16 percent in 9MFY25 due to lower discount rate while borrowings continued to escalate. FML recorded 97 percent weaker net profit to the tune of Rs.13.685 million in 9MFY25. This culminated into EPS of Rs.0.03 in 9MFY25 versus EPS of Rs.1.17 recorded in 9MFY24. NP margin also dipped from 0.88 percent in 9MFY24 to 0.03 percent in 9MFY25.

Future Outlook

The imposition of 10 percent universal tariff on imported goods and additional reciprocal tariffs on the countries with high trade barriers resulted in a total of 29 percent tariff imposed on Pakistan’s exports to the US market. This coupled with higher local energy tariff will result in further decline in the country’s textile exports which is already grappling against regional counterparts such as India, Bangladesh and Vietnam.

However, the company is aggressively looking to expand in other export markets. FML is actively seeking for ways to reduce its energy cost by installing a solar unit and also by enhancing its capacity. Lower discount rate will also significantly reduce the company’s finance cost.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.