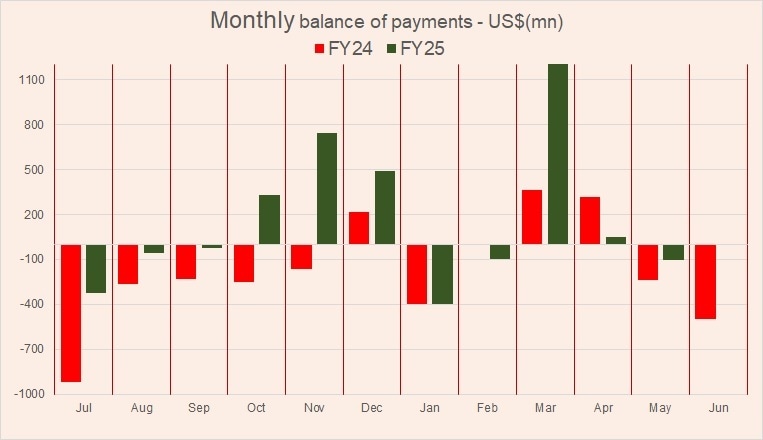

After a brief surplus stint in April 2025, Pakistan’s current account has slipped back into deficit — clocking –$103 million in May. This marks only the third monthly deficit in the past eight months, which may appear reassuring on the surface. But dig a little deeper, and the cracks are more visible than ever.

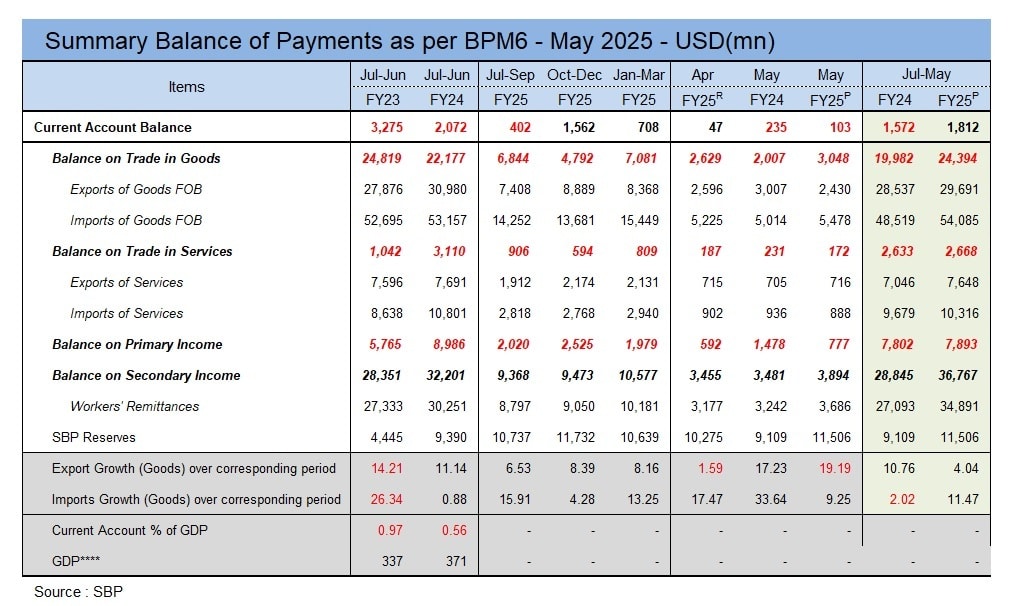

For 11MFY25, the current account shows a surplus of $1.8 billion, a marked improvement over the $1.57 billion deficit during the same period last year. The delta of $3.38 billion is significant. Yet, the quality of this surplus — much like the “growth” it accompanies — is up for debate.

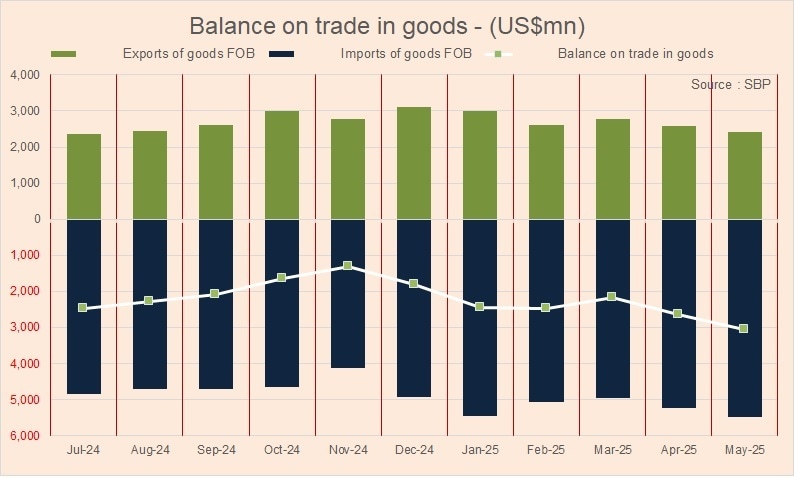

The early warning signs have been flashing for a while — and they’re no longer just flickers. Goods imports are back with a bang, rising 11.5 percent year-on-year to $54 billion — the highest level since FY22, a year marked by sky-high global commodity prices and strong GDP growth. FY25, in contrast, is scraping by with an expected GDP growth of ~2 percent, despite all the statistical stretching.

And the import party might just be getting started. With GDP growth aspirations, regional supply disruptions, and IMF program demands, the import curve could steepen further in FY26.

Zooming in, the textile sector alone accounts for $1.4 billion of the additional import bill, primarily through cotton imports — a full quarter of the YoY rise in goods’ imports. With concerns around Kharif crop prospects and early USDA projections on cotton output looking bleak, reliance on imported cotton may remain elevated. Not a good sign for the trade balance.

The food group is another pressure point. Edible oil imports surged nearly a billion dollars, driven by both quantity and price. Yes, wheat imports saved a billion, but that could well be a short-term reprieve, not a structural fix.

Then there’s machinery and transport, together adding $1.5 billion to the bill. Solar panels are leading the machinery charge — a welcome signal for energy transition — while textile and power generation machinery follow. On the transport side, the budget’s easing on used car imports, paired with lower interest rates and currency stability, might just revive auto demand. That said, 2018 levels are still far away, despite the recent bounce-back.

Exports? Up just 4 percent year-on-year. Textile exports grew 6 percent — stable, not stellar. High value-added exports are holding up, but the global picture is murky. Uncertainty around US tariffs, ongoing negotiations with Pakistan and competitors, and potential Chinese price retaliation could threaten Pakistan’s fragile edge in some product lines.

Food exports have slowed, with rice taking a hit, although, sugar saved some grace. Horticulture exports are down. Curiously, over half the $1.1 billion rise in goods exports came from a vague "other exports" category. Could be arms, could be something else. Either way, don’t count on it recurring.

Which brings us to the real hero (or lifeline): workers’ remittances.

With a massive 28 percent year-on-year growth, clocking a record $35 billion, remittances have kept the current account afloat. This rise is no fluke — it's a mix of organic growth and a successful crackdown on informal channels. But here’s the rub: this base is now huge. Further growth will slow, and there's only so much juice left to squeeze. What’s more, the FY26 budget offers no grant allocation for the Remittance Initiative, which saw Rs87 billion spent in FY25. Will the schemes continue quietly? Will there be a new approach? For now, it's all up in the air — and uncertainty is never a good strategy.

Even the central bank is sounding cautious, citing both domestic and global risks to the external account. If Pakistan pursues the kind of growth envisioned for FY26, it will import more. And without an export-led push, the current account risks reverting to its old, familiar cycle of “boom-bust, rinse, repeat.”

Comments

Comments are closed for this article.