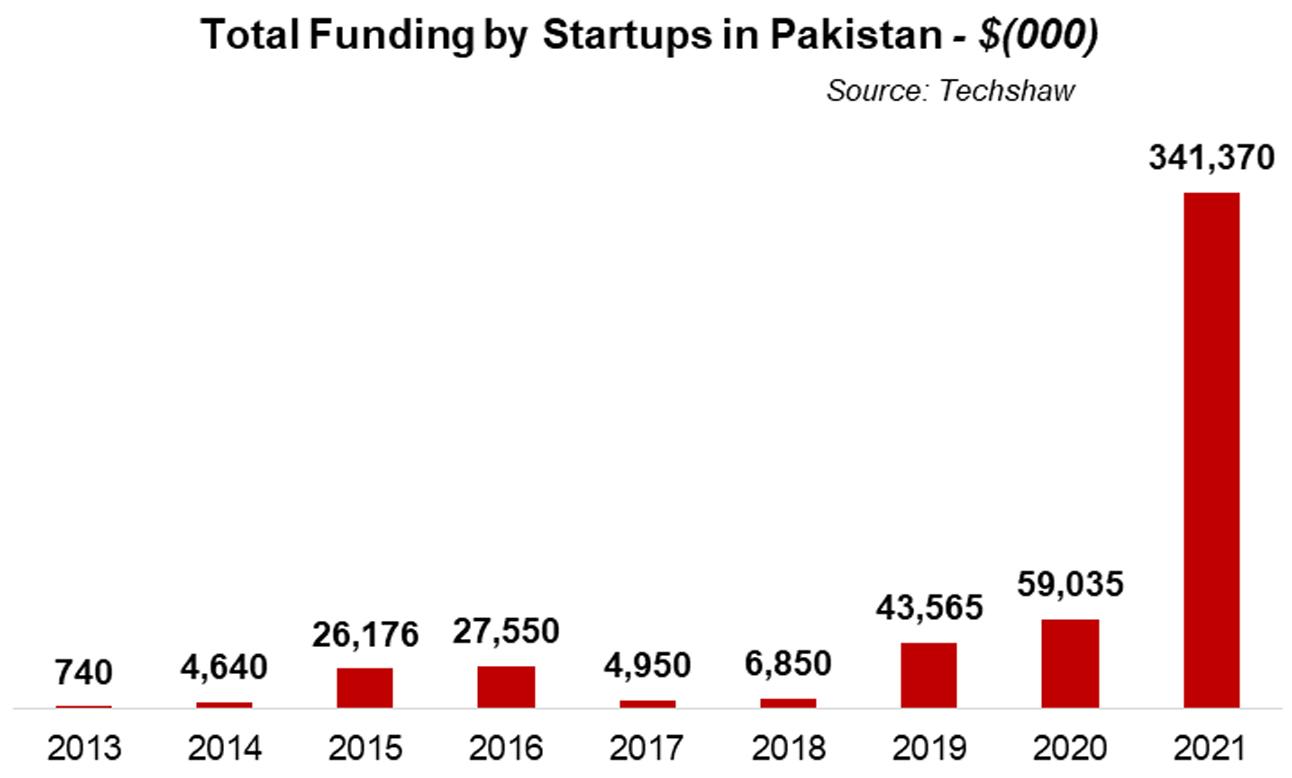

Not only has there been a spate of startups in Pakistan in 2021, there has been a funding frenzy in the startup space with record funding coming in during the year. Overall, 2021 was an inflection point for Pakistani startup space where funding and investment into businesses went through the roof. Total funding in the startups was well above $300 million, which is six times higher than 2020 funding – the previous good year for startups.

I2I’s Deal Flow Roundups for the three quarters of 2021 show that the top funded sectors in terms of total amount raised in 2021 included e-commerce, followed by fintech, and health. It further shows that the seed stage deal count has been on the rise with 2021 recording the highest number of seed stage investments in the country followed by series A and series B.

A key finding from the data available at Techshaw and i2i is that where the total amount raised by startups was staggeringly high in 2021, the number of deals has not increased by the same extent, which means either larger funding rounds or the money is largely going into some specific startups. Also, the funding is coming from multiple investors including VCs, but a general trend has emerged where angel investors and HNWI have also been increasing.

The startup space has definitely come too far in 2021 from a small base earlier on, and the trend will continue. The country has an advantage of its population, increasing tele-density and mobile phone and internet penetration as well as fewer regulatory barriers. But a key challenge for investors and financiers for startups going forward will be macro-economic situation of the country especially with respect to rising interest rates, falling real income, and depreciating currency.

In a startup ecosystem where some startups grow and scale, many fail. With so much funding coming in, the startup ecosystem needs an exit strategy, which is missing currently. Will these startups be able to go and list on the stock market 8-10 years down the line? If they can’t, or have no other viable exit strategy, does that mean there will no unicorns in Pakistan? Nonetheless, as the funding frenzy slackens, many experts believe that a foreign funding crunch could be in the offing - something that India saw 6-7 years ago. This means local investors must be ready to take charge if that happens.

Comments

Comments are closed for this article.