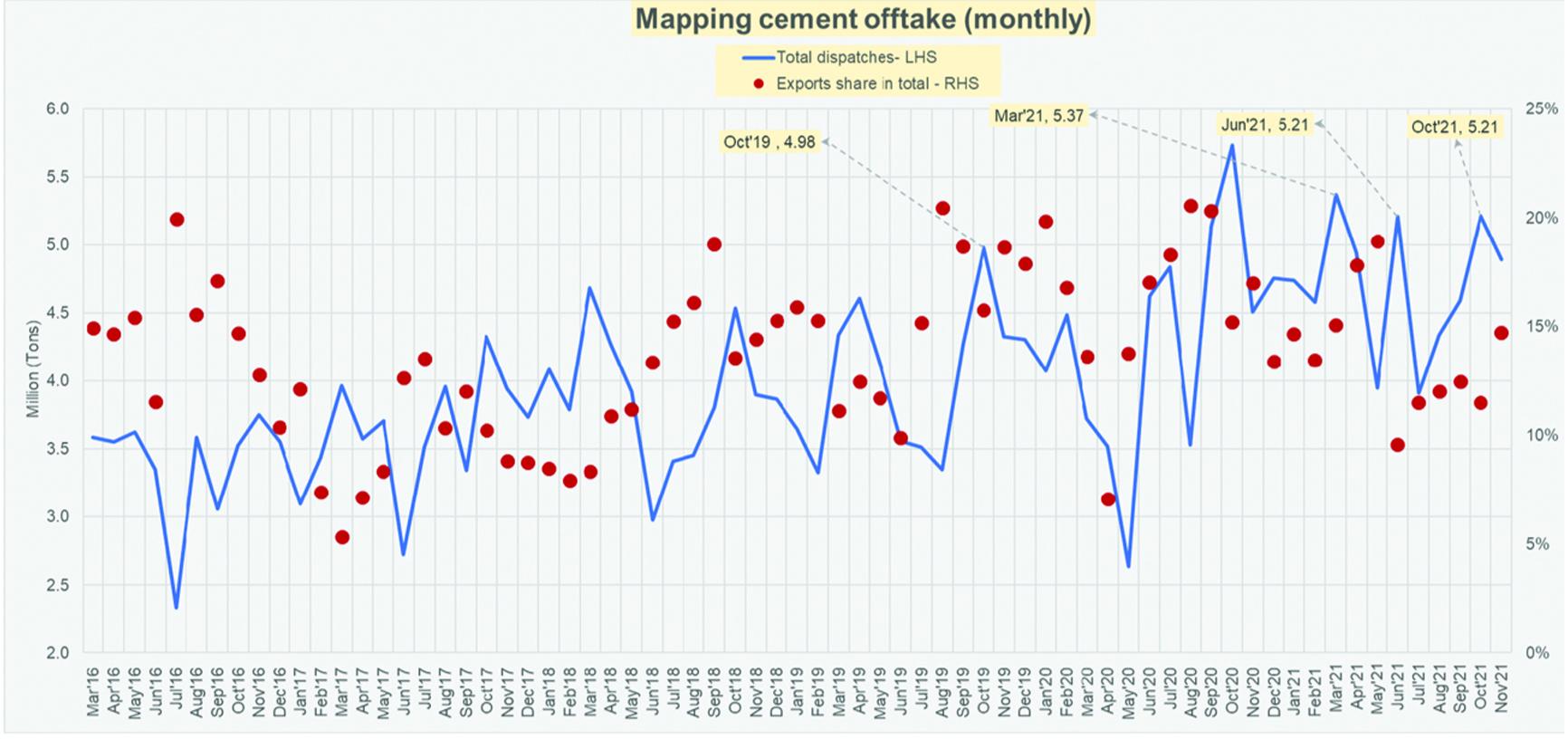

The cement industry is all ready to add nearly 30 million tons of new capacity by FY25, expecting the market demand for cement to grow in the range of 8-10 percent annually over the next few years (read: “Cement’s pecking order”, Nov 15, 2021). Current demand however is not spirited as one would hope. In 5MFY22, estimated total dispatches have dropped 3 percent—the main culprit here being exports which declined 33 percent year on year. Last year, they were 18 percent of total dispatches which has now dropped to 12 percent due to not only reduced demand abroad but also sky-high freight costs that make exports unviable. Domestic dispatches have grown leisurely at 3 percent—not much to write home about.

The second phase of CPEC which constitutes development of Special Economic Zones (SEZs) has had a slow start. While SBP has been boasting about increased construction financing, and within it, the push in housing finance due to Mera Ghar Mera Pakistan mark-up scheme for Naya Pakistan Housing projects, construction demand is lacking lustre. Winter is coming which will further keep construction demand patchy over the next few months specially in the north. At the current pace though, cement offtake this year may land lower than last year, with a dramatic drop in exports. The industry would potentially end the year at a capacity utilization of 76 percent.

But as the industry adds more capacity, domestic demand will have to keep up; otherwise, the industry will be left with plenty of idle capacity and would eventually lose pricing power that it is currently enjoying. This is however, not an unfamiliar cycle for cement manufacturers who go into expansion together, spend a year or so producing in excess of demand and doling out discounts whilst competing with each other for market share. Demand eventually catches up, handing back the pricing power to industry players. Cement prices are being raised over the past year, as domestic demand firmly grew. Cost pressures due to costlier cost and higher freight costs (the Baltic Exchange Dry Index saw a massive growth of 4-5x over the past year) also necessitated these price increases. The industry wrapped the first quarter with gross margins actually growing to 25 percent (from 19 percent) by diverting coal sources and bypassing the nearly 200 percent increase in prices for global coal.

Most cement companies have coal inventories secure for winter, but the global coal price rally has started to simmer down too which bodes well for future procurements; and margins. Cement prices are still being increased gradually in nearly all the markets but manufacturers have to play a delicate game here before demand starts drying up due to costlier construction.

Comments

Comments are closed.