Another week, another increase. If Pakistan had a (functional) commodities futures market, its sugar index would be a gift that keeps on giving. Sugar prices across the country have continued to inch upwards, even as boilers have been fired up for crushing across the country, after the Federal Minister for Industries & Production threatened that mills who ‘delay’ crushing would be penalized heavily.

Should prices decline? It may be too early to tell ‘when’; but if past trends are any guide, they must, and soon. First, once crushing comes into full swing, the speculation of shortfall in the market – that TCP has tried to fulfil with a trickle of imports – will die down. Remember, that the speculation only pertains to the closing stocks from last season, which by any stretch of imagine are now running low. Thus, even if mills claim poor recovery this season, supply position in the local market shall be restored soon, leaving little reason for retail prices to continue to feel upward pressure beyond November.

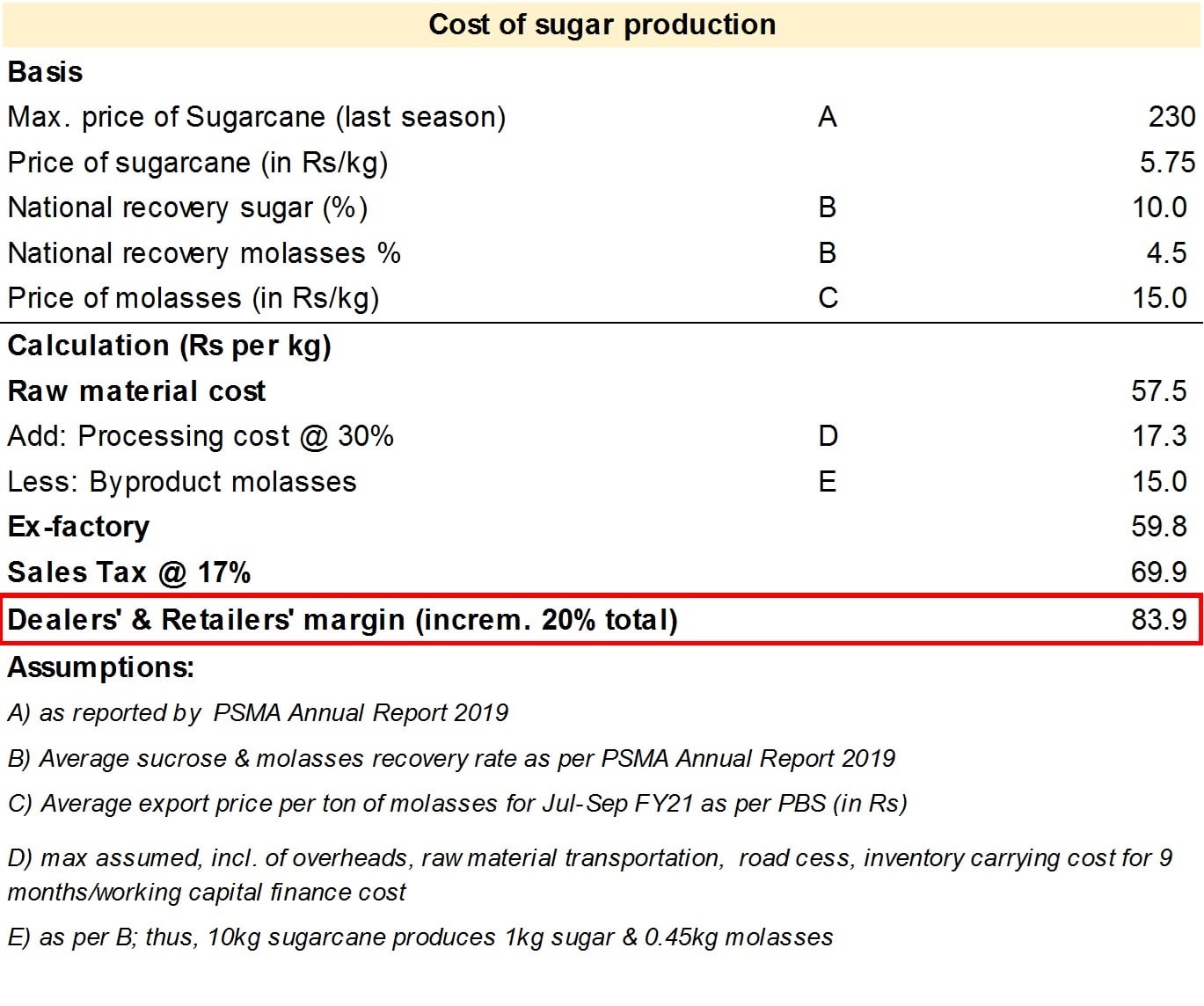

But can prices refuse to decline, even if they stop their endless climb upwards? There is one possibility: if procurement price of sugarcane remains high. News from farming community indicates a bumper crop, which historically weakens growers’ bargaining power. Even so, given the high risk of regulatory interference due to media highlight, chances are that mills will pay a fair & remunerative rate to growers, to prove “inter-mill competition for cane procurement”, and to demonstrate that they do not make abnormal profits at the expense of growers and consumers.

In which case, do not consider it beyond the realm of possibility that mills will claim paying a premium for cane procurement. Also consider that the base price has been increased to Rs 200 per 40 kg (a Rs10 increase – which gives credence to the possibility that average procurement rate may come down at the higher side compared to last year. Either way, even if average procurement price comes out at the maximum rate of last season, prices are still anticipated to decline. Why?

Finance cost. For as long as interest rates do not increase between December 2020 – July 2021, carrying cost of sugar produced will decline considerably compared to the previous year. Recall that the crushing season begins in earnest by December and closes across the country by March. Although monetary policy has been considerably loosened since the onset of Covid-19, most mills drawdown their pledge financing facilities during the peak crushing period, which means revised pricing for finance may have only been locked in beginning July 2020 (by which time mills had already sold most of their stocks in open market).

If nothing else, lower cost of finance coupled with increased supply of sugar should mean the ex-factory price of sugar may no longer remain the same. Regulatory pressure for timely payment to growers (within 15 days of procurement) means mills will be cash hungry in the coming season, meaning they may be more willing to sell off their stocks at lower prices compared to last season, when output was at a 5-year low, and mills’ bargaining power – vis wholesalers and dealers – was high.

Sugar prices have been on an endless joyride for the past two years. While the industry has come into cross-fire due to allegations of ‘collusive behaviour’, it is hard to fathom that any trick of the sort shall come into the way of market forces this season.

Comments

Comments are closed for this article.