The spinning industry may have to fulfil close to half of its cotton requirement through imports during the ongoing season, as domestic production may struggle to exceed 6 million bales. Damage due to extreme weather only partly explains the low output, which is primarily attributable to the crop falling out of favour with growers, a storm that has long been in the brewing. Last week, this space claimed that the ‘loss of cotton acres is not a loss to farmers’; they have indeed been forced to switch away from cotton, but not necessarily to less preferable crops. Here’s why.

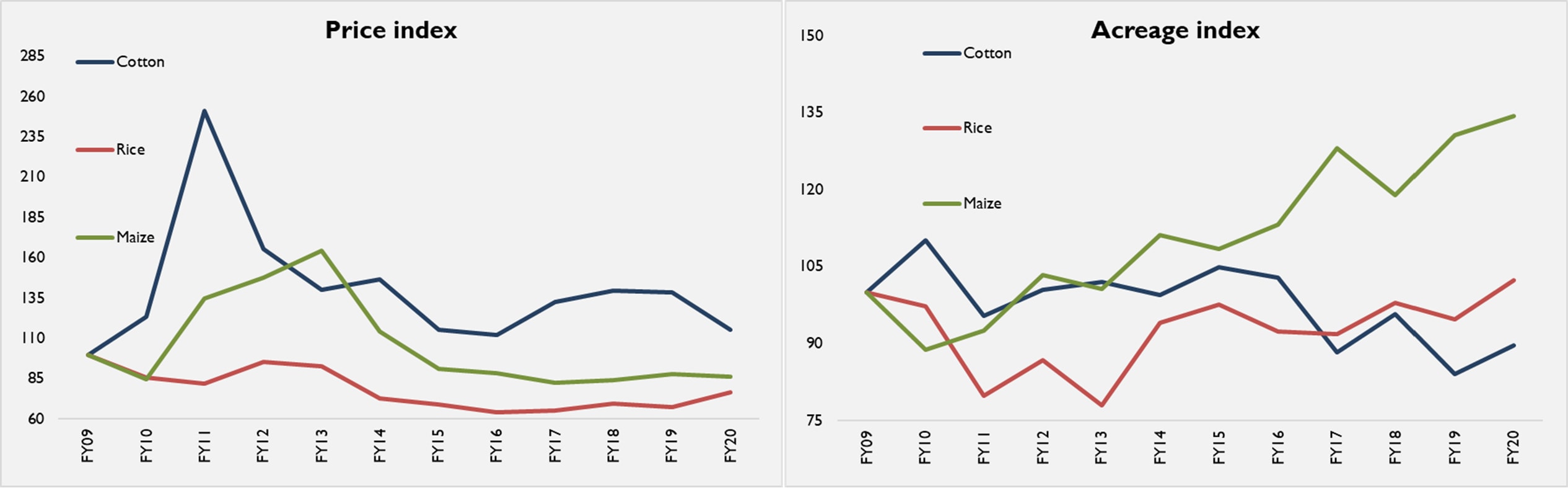

A cursory glance at global price ($ denominated) indices trends of cotton and its substitute crops may dispute this notion. Over the past decade, bears have dominated global agricultural commodity prices, as price of competing crops such as maize and rice have witnessed a steeper decline than cotton. Has policymakers’ indifference towards agriculture forced farmers to grow less profitable crops?

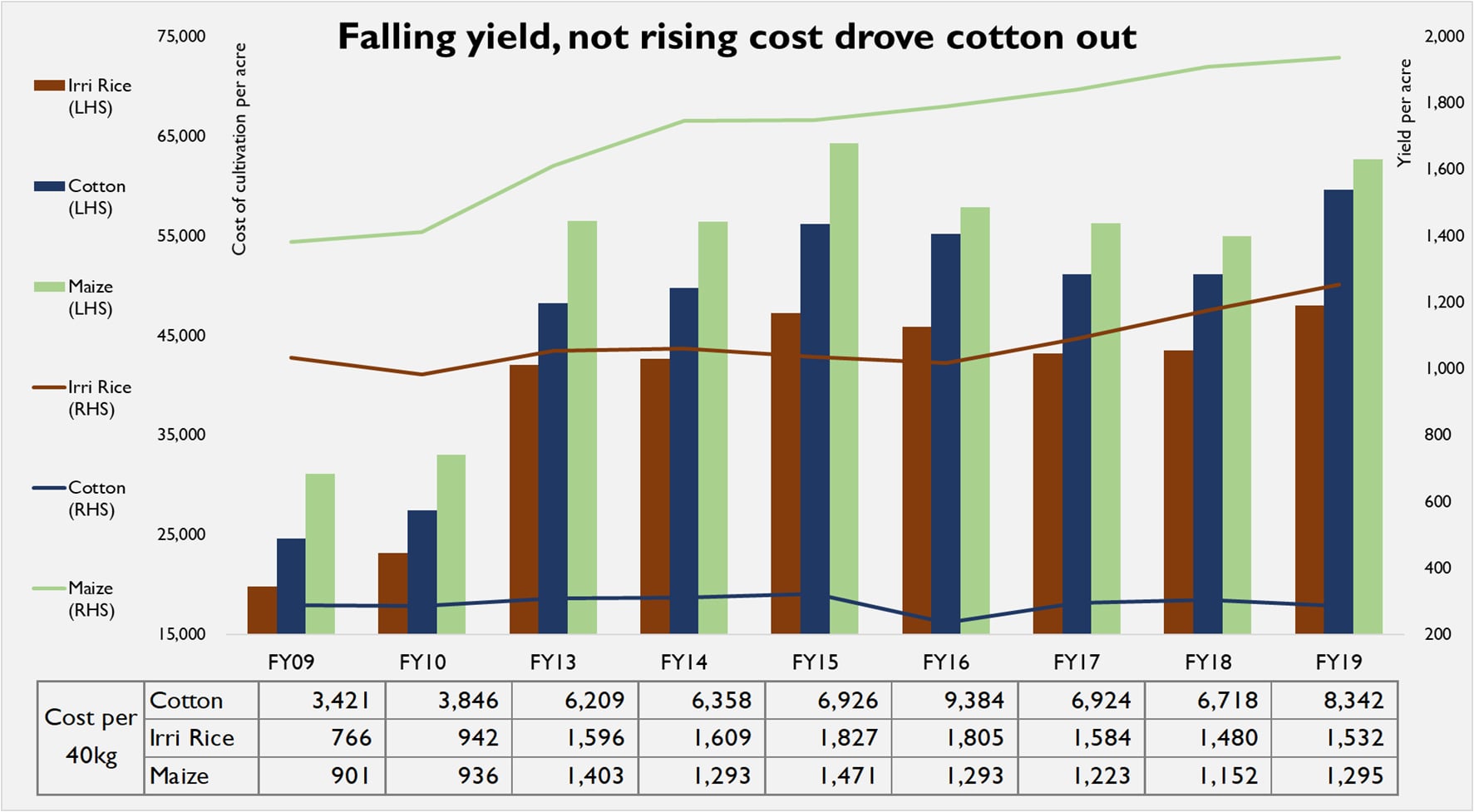

The tale of tragedy does not end there. Using nominal domestic prices, observers note that over past 10 years, cost of production for cotton and its competing crops has more than doubled, which bearish commodity prices have failed to offset. They are correct, going by cost of cultivation per acre, as notified by Government of Punjab annually.

Yet, the conclusion drawn from the ‘falling prices, and growing costs’ theory is wildly incorrect. Cost of tilling an acre of land may have indeed doubled, but thanks to advancement in seed technology, an acre of land is far more productive today than it was 10 years ago.

For both rice and maize, productivity advances mean unit cost of production has grown at a negligible rate over the last decade, in fact declining in real (and $) terms for maize. The fibre crop stands out, in that a cotton acre yields less output today than it did 10 years ago, even as cost of inputs consumed by the same parcel of the land has grown at the same pace as competing crops.

Few conclusions stand out: in absolute terms, input costs have grown for all crops across the board in tandem with inflationary pressures. For crops such as maize, required investment per acre is even higher than that for cotton, indicating that it is not lack of liquidity/investment avenues that pulling farmers away. Lack of interest in cotton is not a matter of affordability; thus, subsidies on inputs alone will not reverse cotton’s impending demise.

Bearish trends in international markets are not responsible either; Over past 10 years, commodity prices of competing crops have been under greater pressure than cotton. Thus, replacing import price parity with an indicative or minimum guaranteed price for domestic cotton will not persuade growers to go long on the crop. Especially not when unit cost of production for competing crops is more profitable.

Cotton’s challenge is of yield alone. And will not be resolved by rigging any other variable of the equation, whether its area under cultivation, purchase price, or input costs. Unless the decline in yield is arrested, in 10 years, government may have to give away free inputs to convince farmers to grow cotton. Even that may prove insufficient.

The MNFS&R knows the answer is adoption of seed technology. But may be the resolution will not feel dramatic enough unless it turns into a full-blown crisis first. What will it take? Cotton import bill is already projected to be double this year; may be, if triples or quadruples as a result of global cotton prices going on a bull run. That’s nowhere in sight. Meanwhile, will biotechnology companies wait and watch, or divest from a market that refuses to grow?

n.b. (1) the author has consciously excluded comparison with sugarcane, a substitute crop that is not only more profitable due to guaranteed return (a market distortion), but is also uniquely more attractive as it requires lower investment in annualized terms (due to longer duration) and less risky (due to higher resilience in face of extreme weather). (2) Price indices for 3 substitute crops e.g. cotton, rice, and maize are a proxy based on internationally commodity prices (World Bank); note that as the three crops are freely traded with no government intervention in price fixing, domestic prices move in tandem with global prices.

Comments

Comments are closed for this article.