Power generation data for August 2020 is out and the upward trend has continued – as the total generation went up by 3 percent year-on-year to 14.2 billion units. Under normal circumstances, such small changes would not warrant a mention, but the numbers for the last two months have come on the back of a long streak of negative power generation growth. The demand, it seems, is back to where it belonged during pre-Covid days.

The demand has fully recovered can now be said with some degree of confidence, as Pakistan seems to have weathered the Covid storm. The power generation mix continues to look impressive, but hardly changed from the same period last year. As winters approach, the contribution from natural gas is expected to dwindle, as the government will again grapple with the distribution priority of natural gas.

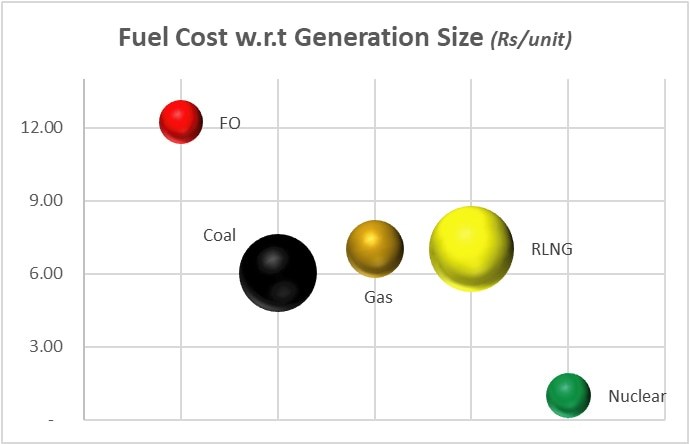

The demand is likely to slowdown as it usually peaks around August and September, and one expects the furnace oil plants to go back in hibernation as the demand will settle under 10 billion units from October onwards, for at least six months. The coal-based power generation has been at all-time high in the last two months, and should now represent a bigger chunk of the pie at the expense of RLNG plants – being 15-20 percent cheaper in terms of fuel cost, sitting higher on the merit order.

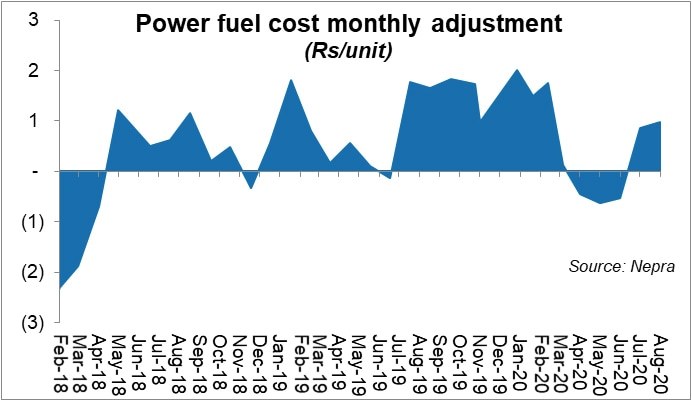

The problem that has resurfaced, after a brief period of generation fuel cost under reference cost, is the rising fuel cost, which has necessitated increase in monthly Fuel Price Adjustment (FPA). Recall that long pending monthly FPAs were only very recently decided and were done in a way so as to minimize the impact on consumers. The government had decided to freeze tariffs and all monthly FPAs were delayed and then clubbed together to be collected in two months.

But the tide will not always be favoring the government on FPA. Firstly, no one knows how the IMF is now going to react to any such intention of carrying the price freeze ahead, in terms of monthly FPAs. The recent announcement of quarterly tariff adjustments to the tune of Rs1.62/unit for the next 12 months is indicating that the prices are now all set to move north. And the problem this time around with FPAs is that the last two months have already created an average of Re1/unit increase in monthly tariffs.

The difference is increasing by the day, despite lower oil prices. The merit order, on which the reference fuel cost is based, is never followed in spirit, and that causes the need for monthly adjustments. It would not have been a problem had that been an automatic adjustment, not requiring the government’s nod. Not only does this lead to the obvious eventuality of higher consumer tariff, it also leads to the stock of unadjusted tariff – which already stands in tens of billions of rupees.

The ballooning capacity payments are already there – and largely remain unaddressed as the demand has failed to match the increase in generation capacity. With winters approaching, expect hefty capacity payments made to RLNG plants for being available. Add the monthly FPAs, on which the government remains undecided and is hoping for negative adjustments to nullify in the future – and you are back to square one. Hope is not a plan. The state of power affairs tells that remains about the only plan for all the near-term woes.

Comments

Comments are closed for this article.