The shipments have finally arrived! After nearly yearlong wheat and flour shortfall, rollercoaster ride of wholesale and retail prices, media outcry, and FIA inquiry, Pakistan has finally imported un-milled wheat worth $9.5 million, as per external trade figures released by PBS for August 2020.

At 39,348 tons, the import volume is equivalent to Karachi city’s wheat demand of less than 6 days, assuming annual per capita wheat consumption of 125kg. Hopefully, the measly quantity imported shall be augmented by further imports over the next several months, as the import quota announced by federal government several months ago continues to be utilized. But will it help reign in the flour prices run amok?

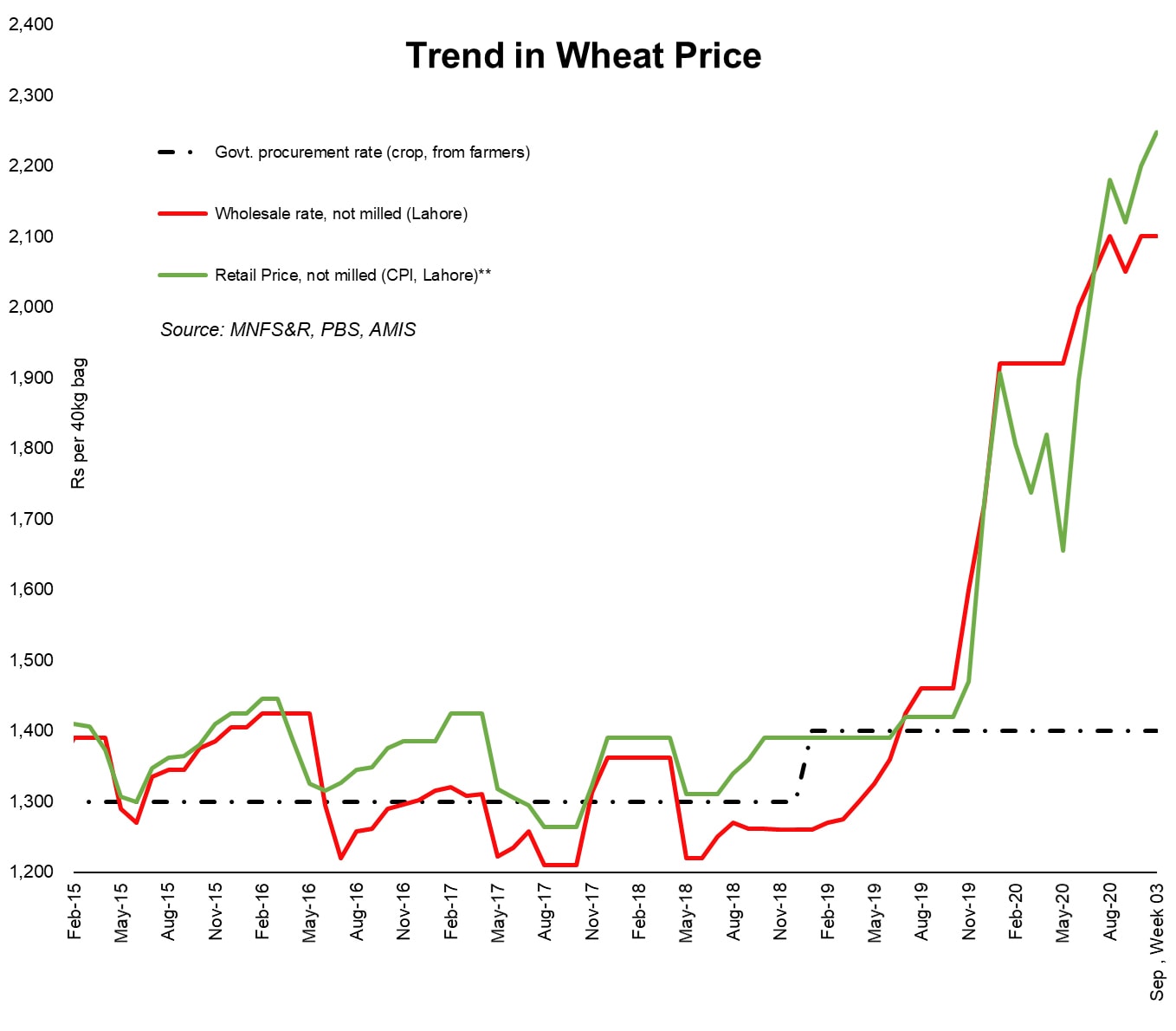

Going by the increasing premium between international wheat prices and domestic retail rate, Pakistan should witness a lot more imports in the months to come: the next harvest is still over 6 months away, whereas domestic prices – both wholesale and retail – have continued charting fresh heights since the latest harvest ended in May 2020.

Over the past 6 months, international prices for US HRW wheat has averaged a little over $200 per ton, even as domestic retail prices have increased by at least 20 percent in dollar equivalent terms (and 30 percent in Pak Rupee). Granted that it may be problematic to compare international commodity prices with domestic retail market rates, the rate of increase is still a valid proxy to forecast prices in months to come as the country continues to run out of stocks from last harvest.

But first, some discussion of the premium between international and local prices. Long before the last currency devaluation cycle began in December 2017, wheat in Pakistan retailed at a substantial premium over international prices. Between Dec 2014-2017, the premium averaged at nearly 1.90 times, ranging between 1.4 – 2.35 times.

As it happens to all commodities, the sharp currency depreciation that followed quickly evaporated this difference; between January 2018 and June 2019, the premium dropped from 1.75 times to a little over 1.05 times, nearly bringing domestic retail prices at par with international commodity prices.

It appears that ‘the rise and rise’ witnessed in domestic wheat prices since then is simply an effort to restore/reverse the premium to its ‘normal levels’, in effect nullifying any gains made due to devaluation. But what good is a peg with international prices if the commodity market has historically been insulated from external trade, thanks to prohibitive controls on both import and export?

Answering that question takes us to the realm of conjecture. While traditionally held beliefs about self-sufficiency dictate that the country witnesses commodity shortfall every time there is a currency devaluation as unscrupulous elements smuggle it out of the country to make a quick buck, a look at price chart also offers an alternate explanation.

Consider that each time currency devaluation brings international and local prices close, importing (or smuggling) wheat into the country becomes a less profitable proposition. Because wheat import from official channels is usually barred, smuggling the commodity into the country must require a hefty premium. Going by this theory, average premium of 1.90 times during Dec 2014-2017 suddenly begins to make sense.

Also consider that the landed cost of wheat imported from official channels during August 2020 comes out at $242 per ton. This indicates that prevailing (dollar equivalent) local prices of $330 per ton is finally beginning to offer an attractive premium. But at 1.67 times, is it still attractive enough?

The low volume imported so far means that imported supply will barely make a mark on domestic prices. And unless cargo ships carrying over million tons dock at ports between September and December, domestic prices may continue their upward trajectory well into the next sowing season.

And that should scare the czars of agriculture policymaking. Unless the country is blessed with a bumper crop miracle next season, the premium between domestic wholesale/retail and government notified rate (support price) is already so high that MNFS&R will have no choice but to increase support price substantially, or risk missing its procurement target by a substantial margin.

As of August 2020, 40kg wheat wholesale price is averaging close to Rs 2,100 (retail price Rs 2,200) against government procurement rate of Rs 1,400kg. Except, increasing support price will fuel a vicious cycle which may drive further increases in domestic wholesale and retail rates. Unless, the government decides to pick up an ever-greater share of the tab – that is, the difference between the rate at which it procures wheat from growers (support price) and the issue price at which it sells the commodity off to millers.

Of course, no government can ill-afford an abrupt exit from a commodity market as essential as wheat. Also granted that the substantial subsidies on fertilizer announced in the PM Agriculture Package may go some way in helping improve wheat output in the upcoming season. But there are many a slip between bona fide incentives and a bumper crop, untimely rain and frost witnessed over last two years being the chief among them.

Given restrictive fiscal space to further subsidize wheat, the policymakers may wish to reconsider the limited quotas announced for import, and instead give some weight to suggestions of opening up the floodgates of import, at least temporarily. Erratic crop performance amid stagnant yield over the last decade indicates that delaying decision on import quantum until peak harvest season is a risk the country can ill-afford. If the crop output target suffers substantially, abrupt announcement of large import quotas may also send international commodity prices out of control, as was witnessed with cotton in the aftermath of 2010-11 floods. And while large import quotas may dampen the spirits of farming community, the guaranteed return on the crop means most growers will still shy away from switching to substitutes, at least not in the upcoming season.

Sooner or later, the public sector will have to exit the wheat procurement business; Punjab has already made commitment to do so under SMART program of the World Bank. Gradually opening up import of wheat over subsequent years may help prepare farmers gear up for the eventuality. And it appears the upcoming 2021 season shall offer a ripe opportunity to take serious decisions. Take the bull by its horns!

Comments

Comments are closed for this article.