Shabbir Tiles and Ceramics Limited (PSX: STCL) was established in 1978 as a public limited company under the repealed Companies Act, 1913. Its primary business is manufacture and sale of tiles and trading of allied building products. Its range of offering includes feature wall tiles, floor tiles, bathroom tiles, kitchen tiles and outdoor tiles in addition to having an exclusive emporium collection. The company also stands as a member of Karachi Chamber of Commerce and Industry, All Pakistan Ceramics Tiles Manufacturers Association and Landhi Association of Trade and Industry.

Shareholding pattern

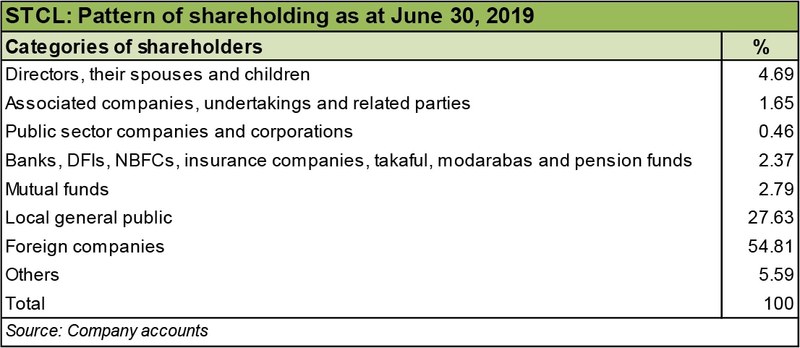

Foreign companies hold majority of the shares in Shabbir Tiles and Ceramics Limited at nearly 55 percent. However, the details of this are not known. This is followed by the local general public that collectively holds almost 28 percent of the shares of the company. Close to 5 percent shares are held by the directors, CEO, their spouses, and minor children. Within this, Mr. Rafiq M. Habib, and Mr. Ali Suleman, both directors of the company, each hold close to 2 percent shares, the highest in the category. The remaining about 12 percent is distributed with the rest of the categories.

Historical operational performance

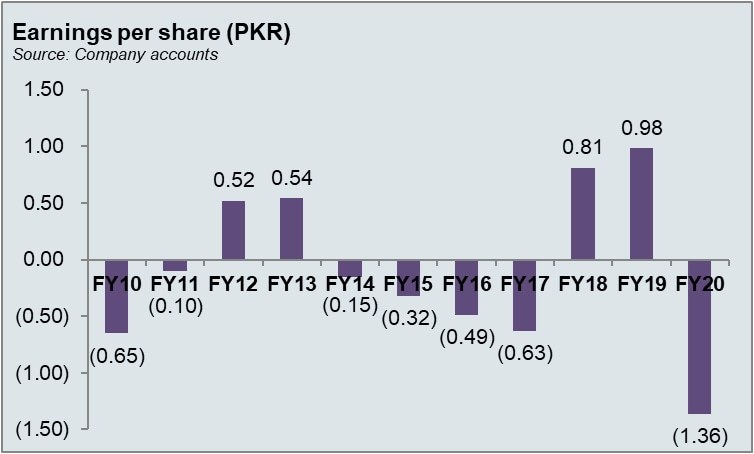

The company’s performance has been dwindling, with a fluctuating topline and a gradual decline in profitability for a large part of the decade, with only FY18 and FY19 seeing any improvement.

During FY15, topline contracted by a little over 14 percent. The company has two main streams of sales: a nationwide dealership network and directly to builders and corporate customers. The company saw sales declining from both the avenues. The industry as a whole also faced competition from under invoiced imports entering the country. In addition to a reduction in revenue, cost of production increased to claim about 83 percent of the total revenue, bringing gross profit down drastically. With other costs remaining more or less intact, the company posted a relatively elevated net loss.

The industry and the company continued to face the menace of dumping of imported tiles during FY16. After continuous efforts, the application for imposition of anti-dumping duties was accepted by the National Tariff Commission (NTC). Although sales revenue improved during FY16 by around 12 percent, this was mostly consumed by cost of sales as the latter stood at 88 percent of the revenue. This was in part due to a 23 percent gas tariff increase. However, this cost could not be passed on to customers due to fierce competition resulting in a decline in profitability. Although finance costs reduced considerably due to lower expense with regards to long term finance, yet the company incurred a loss.

Revenue increased by almost 9 percent in FY17 while profitability failed to recover. Cost of production continued to claim a higher percentage of revenue each year, with FY17 seeing a little more than 89 percent of revenue being consumed by cost of production. Gas tariffs hindered whereas machine upgradation and BMR costs further added to costs that could not be covered by the revenue. Moreover, the company was also not able to increase selling prices due to stiff competition coming from imported tiles. Other income was also not able to contribute significantly towards the bottomline, thereby only escalating the losses.

Shabbir Tiles saw a close to 15 percent climb in revenue in FY18 - the highest it has seen in the last eight years. This was partly due to imposition of anti-dumping duty on imported tiles that allowed companies to regain some market share; however, to some extent tiles still entered the country through smuggling. Moreover, the investment made towards BMR activities also added to profitability as it resulted in better quality and better products. The company also focused on reducing debt and generating cash that is evident from a lower finance cost as a share in revenue. Cost of production, as a whole, also reduced considerably allowing improvements in profitability.

The company saw an even higher growth in revenue at 20 percent in FY19. This was a result of BMR activities conducted in the previous years in addition to spending on advertisements and promotions. Cost of production also went down to improve profit margins for a second consecutive time. With other costs remaining intact as a percentage of revenue, and an increase in other income that came from gain on disposal of operating fixed assets and sale of scrap, profit margins reached its highest seen in almost a decade.

Recent result and future outlook

The company’s financial performance in FY20 suffered. Revenue in the last quarter (Q4) fell drastically in comparison to previous three quarters; rather halving quarter on quarter leading the company to incur a gross loss in FY20. This was seen for the first time in a decade. While cost of production remained intact, partly due to the fixed cost element, while other costs reduced corresponding to lower sales. As a result, the company saw its lowest profit margin during FY20. With the outbreak of Covid-19, the construction sector was given a special incentive package, as a result of which the company hopes for some revival. However, results of current year have been affected due to halt in production processes and lock downs placed in various cities of the country.

Comments

Comments are closed for this article.