First UDL Modaraba (PSX: FUDLM) was established in 1991 under the Modaraba Companies and Modaraba Ordinance, 1980. The modaraba is managed by UDL Modaraba Management (Private) Limited. It provides finance on Murabaha and Musharaka arrangements, Ijarah, commodity trading, manufacturing, and trading of pharmaceutical products.

Shareholding pattern

About 44 percent of the certificate holding is under associated companies, undertakings, and related parties. Within this category, two major holders include UDL Modaraba Management (Private) Limited Mr. Khalid Malik. About 40 percent is distributed with the local general public while directors, CEO, their spouses, and minor children collectively hold close to 6 percent of the certificates. Of this, Mr. Shuja Malik, the CEO holds majority of the certificates.

Historical operational performance

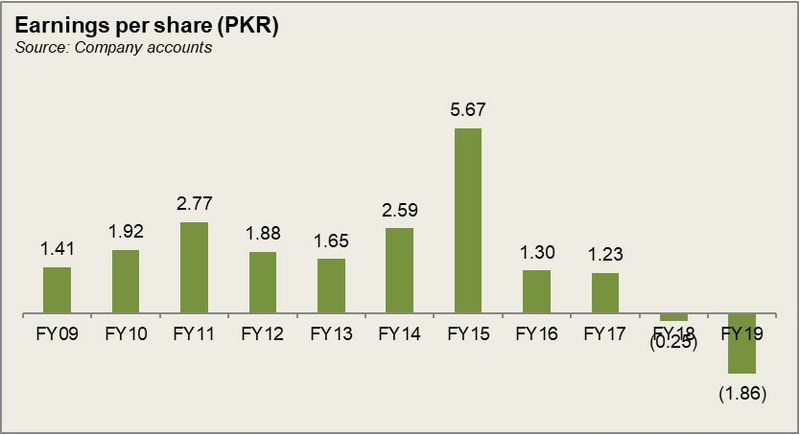

The company’s two primary sources of revenue are ijarah rentals and musharaka receivables. However, over the years, both have declined with musharaka receivables disappearing in the last two years. Income from investments, on the other hand, gained traction but that too, in FY19 reduced to a mere Rs 4 million.

By FY15, income from ijarah operations less than halved. This was attributed to “sizeable maturity of the portfolio”. Income from investments also declined in absolute terms, but its share in total income had increased. Investment income is largely made up of two components: dividend income and gain on sale of securities. During FY15, gain on sale of securities reduced which caused the overall investment income to fall. With a more than 50 percent reduction in total income, the company saw a negative operating profit figure for the first time in almost a decade. However, an addition to income categorized as “extraordinary item” allowed the overall net profit figure to be positive and increase in comparison to last year. This “extraordinary item” was explained as “transfer of long term associated company shares to non-associated at the current market price”.

Income from ijarah operations further reduced in FY16, while musharaka receivables stood at the same level. Investment income, on the other hand, picked up, however, as its share in total revenue, it had reduced. Nominal increase in investment was due to gain on sale of shares. The company had also started adding to its income from its pharmaceutical business, with FY16 its fourth year of adding to income. The increase in revenue from pharmaceutical business was due to volumetric sales, however, if cost of goods sold were to be incorporated, the business was incurring a loss, as the latter exceeded the revenue generated from pharmaceutical operations. However, the overall income allowed profits to increase if the abnormal income seen last year were to be left out.

Share of ijarah operations and musharaka receivables continued to fall in total income in FY17, however, revenue from pharmaceutical business gained momentum as its revenue more than doubled. This was due to continuous addition to the portfolio. Moreover, the company was also manufacturing two new products for a major pharmaceutical company which supported the bottomline of the Modaraba. For the first time, since the operation of pharmaceutical business, FY17 saw profit yielded from this division. investment income, however, reduced but it was more than compensated for by the revenue incline from pharmaceutical business. Yet, this did not allow for a positive operating profit due to increase in costs of goods sold and selling and distribution expenses. However, this was made up for by a positive gain on settlement of liability which resulted in a positive net profit, albeit lower year on year.

Income fell to an all-time low in FY18 with pharmaceutical business, that was contributing significantly to the total income, disappearing completely. This was due to discontinuation of the pharmaceutical business owing to rupee devaluation and taxes imposed on company’s manufacturing activities, in addition to government’s policies towards the pharmaceutical industry, which did not deem it feasible to continue operations. With pharmaceutical business out of the picture, its related costs were also eliminated, investment income became the major contributor to total income which resulted in a positive operating profit whereas net profit was affected by loss due to discontinued operations. Total income further fell to another low in FY19 less than halving, at Rs 35 million. Due to the bearish stock market, investment income reduced, while income from financial activities fell due to cash flow diverted towards pharmaceutical operations in the previous years. With no other major expenses, the company was able to post a positive operating profit, which converted into a negative net profit due to loss from discontinued operations.

Quarterly results and outlook

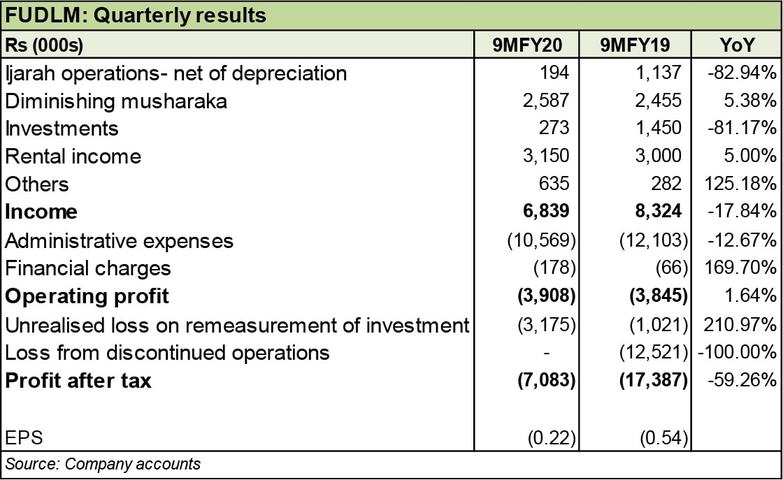

The two primary sources of revenue, ijarah operations and investment income saw a decline, while income from diminishing musharaka and rent saw a 5 percent incline during 9MFY20. Decline from investment income was due to the prevailing economic situation, in addition to the adverse effects of the outbreak of Covid-19 and the resultant lockdown. With lower income, the company was unable to cover its costs, resulting in a loss, although lower than that seen in the corresponding period last year. This was because of the loss incorporated in the last year from discontinued operations.

The company hopes that as situation improves it would be able to liquidate its investments and increase its financing activities.

Comments

Comments are closed for this article.