First Habib Modaraba (PSX: FHAM) is a multi-purpose modaraba managed by Habib Metropolitan Modaraba Management Company (Private) Limited. Its principal business is that of leasing (Ijarah), Musharaka and Murabaha financing.

Shareholding pattern

More than 50 percent of the certificate holding is held under the category of “others”, the details of which are not disclosed. A little over 26 percent of the certificates are distributed with the local general public. Associated companies, undertakings and related parties own 10 percent of the certificates; this category solely includes Habib Metropolitan Modaraba Management Company (Private) Limited. The directors, CEO, their spouses, and minor children do not hold any certificates, while the remaining about 7 percent is with the rest of the certificate holders.

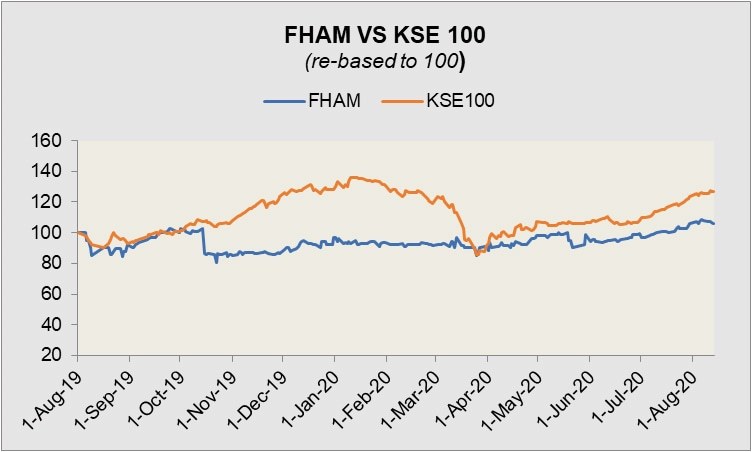

Historical operational performance

The company’s primary source of income has been income from ijarah (leasing); however, over the last few years share income of profit from diminishing musharaka has increased, to claim 80 percent of it by FY19.

During FY15, the economy registered a growth rate of 4.24 percent; although this was higher than that seen the previous year, it was still below the target level. During the year, textile sector which is a major export revenue source saw a decline due to low demand and a limited export market, which had a notable impact on the country’s export earnings. Coming to the company’s performance, it made a disbursement of Rs3 billion of which lease financing claimed a bigger part than diminishing musharaka financing. Asset-wise most of the financing was in the category of motor vehicle- about more than 80 percent. With a slight change in financial charges, profit margin reduced year on year.

In FY16, the economy grew by 4.7 percent, supported by 6.8 percent growth in industry and services; growth in former was due to better energy supply and improvement in the security situation. Looking at the company’s financials, there was a decline in share of income from ijarah whereas profit from diminishing musharaka increased to contribute 47 percent to the revenue. Disbursement increased to Rs3.4 billion of which vehicle financing portfolio made up 85 percent. With a reduction in other income and a rise in finance expense, profit margin reduced further.

Although GDP grew by 5.28 percent in FY17, the highest seen in a decade, it was still lower than the targeted 5.7 percent. This was due to growth in agricultural output as well as the services sector. Agriculture was supported by policies such as subsidy on fertiliser, reduction in sales tax on tractors, and better access to finance.

Although its disbursement continued to increase, the company’s profit margin reduced. The company saw intense competition in the market, particularly with Islamic commercial banks, while vehicle financing continued to make up a large part of the total portfolio, increasing gradually year on year; in FY17, it increased to 84 percent.

GDP growth touched its highest level in thirteen years ay 5.8 percent during FY18. Progress was seen in the agriculture, manufacturing, and services sector. The second half of FY18, however, was marked by political uncertainty, decline in exports, and significant currency devaluation. For the company, financing increased to Rs5 billion; of this 66 percent was made in diminishing musharaka financing, while 84 percent was directed towards vehicle financing portfolio. The consistently increasing income, however, was offset by rise in financial charges that reduced profit margins.

In FY19, the country saw GDP growth shrinking to 3.3 percent. With a high policy rate, agriculture, manufacturing, and service sector saw an adverse impact. The company’s business was impacted due to high lending rates, currency depreciation and increase in cost of utilities and withdrawal of tax subsidies. Total financing increased to Rs5.2 billion of which 76 percent was made in diminishing musharaka and vehicle financing portfolio made up 84 percent of disbursement. With a continuous rise in finance expense, profit margin reduced to its lowest seen in a decade.

Quarterly results and outlook

Both income from lease financing and diminishing musharaka financing saw a rise year on year during 9MFY20. However, this could not be translated into higher profit margins as increase in financial charges exceeded the increase in revenue; high interest rates caused a rise in finance expense. Size of disbursement reduced from Rs4.1 billion last year in the corresponding period, to Rs 3.2 billion in 9MFY20.

However, Covid-19 brought the world to a standstill as business across the country and all over the world saw reduced activity. State Bank of Pakistan (SBP) has brought out circulars regarding “deferment of credit facilities after going through merit of customer’s request” whereas the company is analysing the situation of businesses within various sectors as their operations have been greatly impacted. With reduced business activity, modaraba has received several requests for deferral of credit facilities between three months to one year.

Comments

Comments are closed for this article.