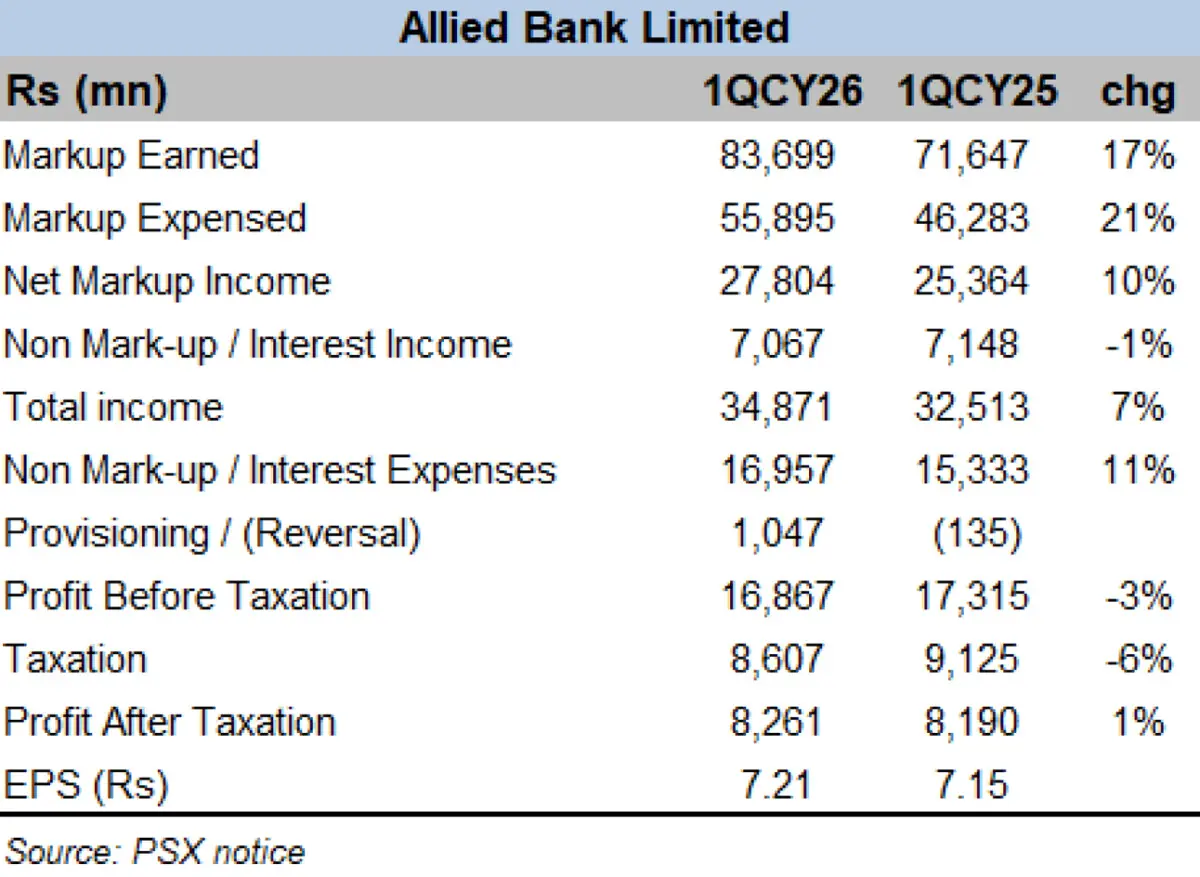

Allied Bank Limited (ABL) announced its financial results for the first quarter of 2026, alongside an interim cash dividend of Rs4 per share, much in line with street consensus.The topline grew appreciably despite lower average interest rates for the period versus same period last year, mainly on account of double-digit expansion in earning asset volume.

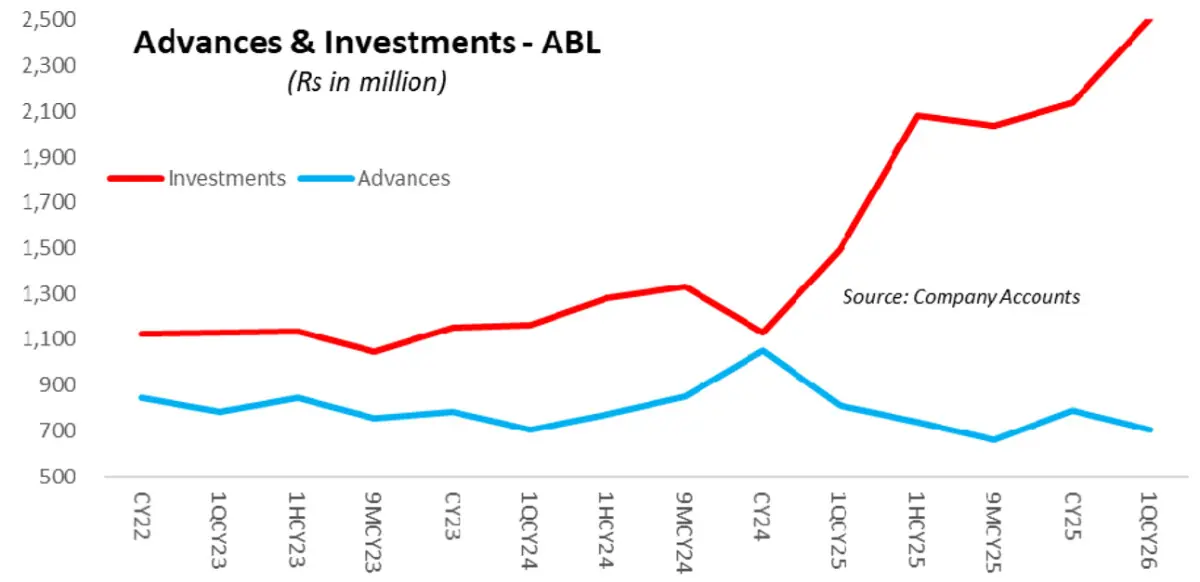

As has been the case across the industry, investments once again came to the fore of asset book expansion. The investment portfolio at ABL by the end of 1QCY26, soared 17 percent over December 2025–an addition of Rs368 billion–at Rs2.5 trillion. The Investment to Deposit Ratio (IDR) clocked an astonishing105 percent – comfortably the highest ever.Interestingly, 105 percent is also the coverage ratio at ABL. This is how much the banking asset allocation landscape has altered in the last 12 months or so.

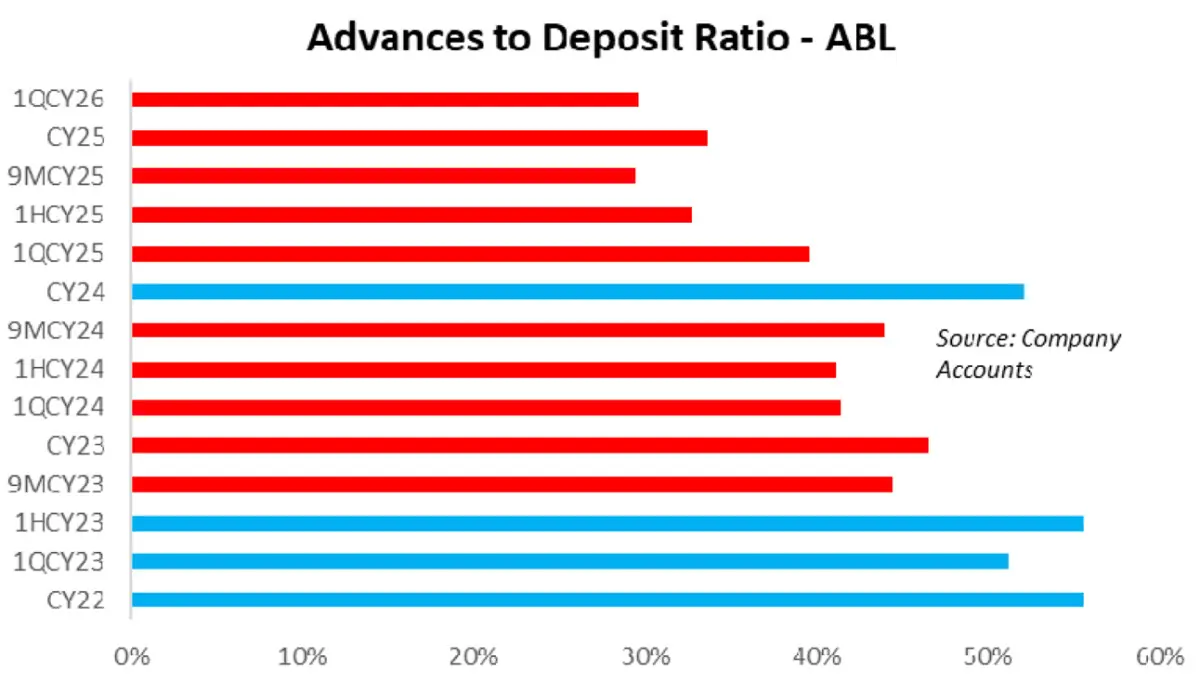

Advances, on the other hand, shed Rs85 billion over December 2025. At Rs704 billion – ABL’s advances portfolio is amongst the lowest for any period end in the last four years. Recall that the advances portfolio had crossed Rs1 trillion mark at the end of CY24 – as banks rushed to meet the ADR requirement in order to avoid higher taxes.

Allied Bank’s ADR slipped close to 10 percentage points from a year ago to under 30 percent – only the second time in recallable memory. Businesses have not been really lining up for credit of late and to satiate the government’s seemingly never-ending appetite for bank borrowing – banks have relied heavily on government’s open market operations – only for the government to borrow from banks again.

Not surprisingly, markup expensed on borrowings is nearly doubled from a year ago – and markup earned on investments now accounts for nearly three-fourth of all markup earned. Deposit growth has slowed across the industry. Allied Bank saw its CASA ratio negligibly changed from December 2024 – with domestic current accountposting a slight decline.

On the non-markup front, things are pretty without being exemplary. Commission income and dividend income continue to grow at a healthy pace, whereas sale of securities and foreign exchange income contributed lower from a year ago. Administrative expenses grew well over period inflation as the bank went on investing on technology and branch expansion.

With the ongoing war throwing uncertainties, businesses have been on the rather cautious side. The interest rate increase late last month will likely lead to repricing of assets and tenor management will once again be at the center of asset mix reprofiling. ABL’s infection and coverage ratios sit at very sound levels, and there appears no reason to panic. Whether or not, banks resort to more lending remains to be seen, but shareholders are not exactly complaining, as the banking sector keeps positing decent profits.

Comments