Idrees Textile Mills Limited [PSX: IDRT] was incorporated in Pakistan as an unquoted public limited company in 1990. The company is engaged in the manufacturing and sale of yarn and fabric.

Pattern of Shareholding

As of June 30, 2025, IDRT has a total of 19.853 million shares outstanding which are held by 1544 shareholders.

Directors, CEO, their spouse and minor children have the majority stake of 85.93 percent in the company followed by individuals holding 13.514 percent shares. The remaining ownership is distributed among other categories of shareholders.

Historical Performance [2020-24]

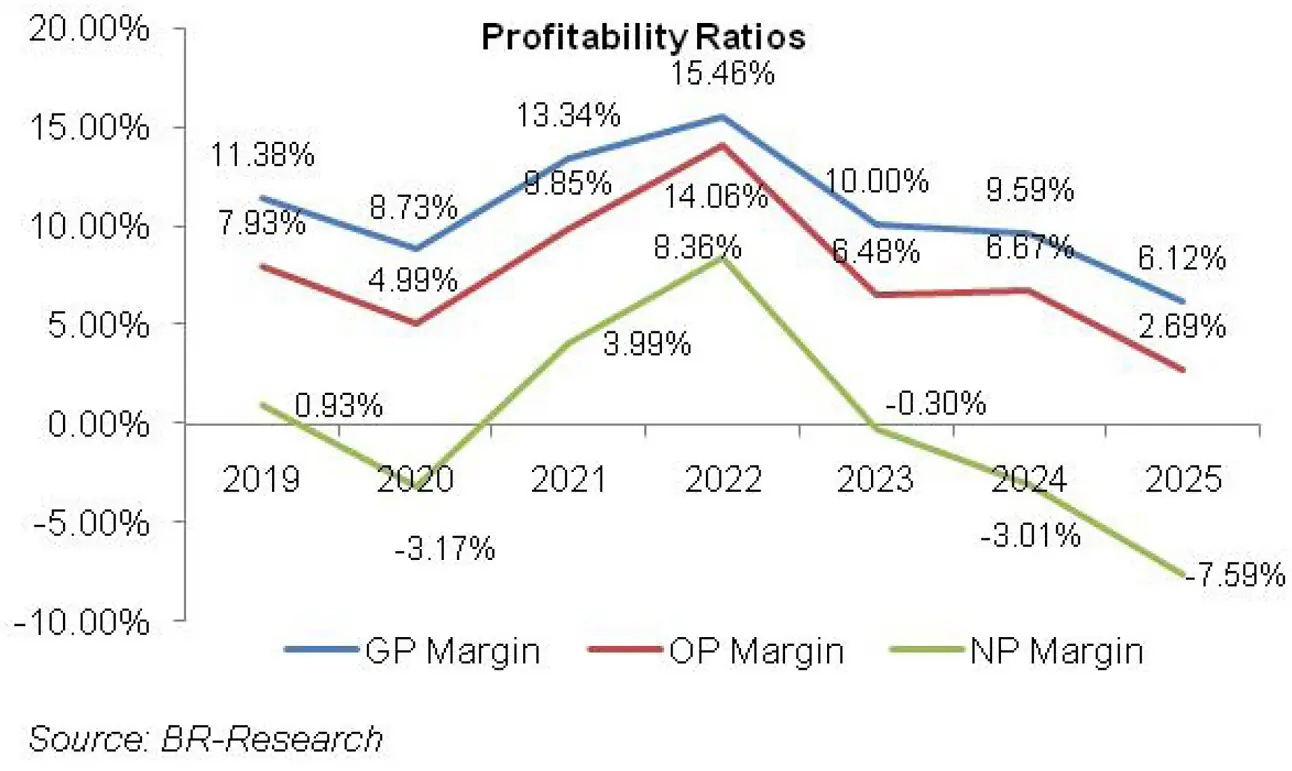

IDRT’s topline slid thrice during the period under consideration i.e. in 2020, 2023 and 2025. The company posted net profit only in 2021 and 2022. IDRT’s margins which slumped in 2020, posted sound recovery for the next two years to attain their optimum level in 2022.

In the subsequent years, gross margin ticked down while operating margin inched up in 2024 and descended in 2023 and 2025. Net margin stayed in the negative zone since 2023. IDRT’s margins hit their lowest level in 2025 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2020, IDRT’s topline slid by 6.69 percent to clock in at Rs.3239.26 million. This was on account of reduced demand as well as curtailed operations on account of COVID-19 related restrictions.

The company’s annual production slid from 17.37 million kgs of yarn in 2019 to 10.073 million kgs in 2020. Cost of sales slid by 3.90 percent during the year, resulting in 28.40 percent thinner gross profit recorded during the year. GP margin also fell from 11.38 percent in 2019 to 8.73 percent in 2020.

Distribution expense mounted by 42.43 percent in 2020 on account of higher freight and octroi charges as well as elevated clearing and forwarding charges on account of disturbances and blockages across the supply-chain.

Administrative expense grew by 7.52 percent in 2020 due to higher depreciation expense as well as fee and subscription charges incurred during the year. No provisioning done for WWF and WPPF as well as lesser infrastructure cess incurred during the year resulted in 20.84 percent lesser other expense in 2020. Other income mounted by 195.32 percent in 2020 due to gain recognized on the sale of property, plant and equipment as well as higher profit recognized on saving deposits.

Operating profit tapered off by 41.2 percent in 2020 with OP margin sliding down from 7.93 percent in 2019 to 5 percent in 2020. Finance cost surged by 15.10 percent in 2020 due to increased borrowings and higher discount rate for most part of the year.

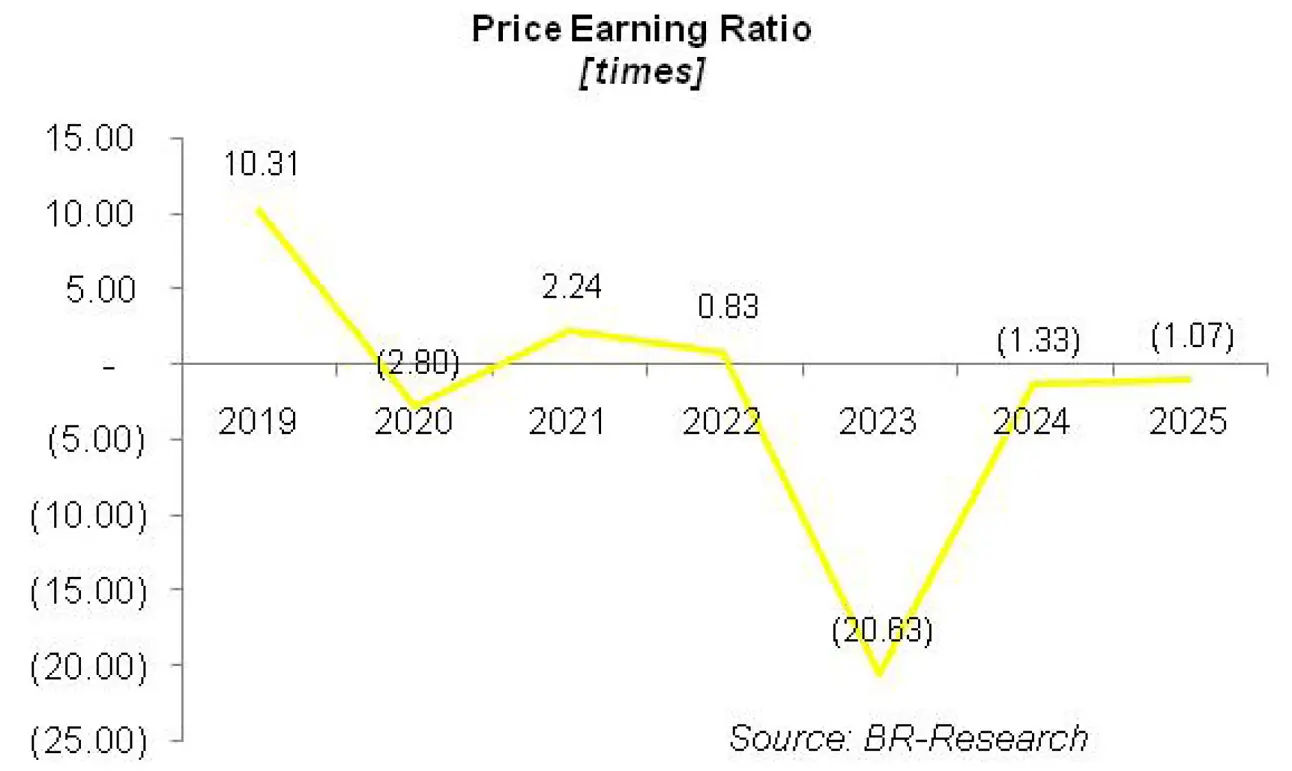

IDRT registered net loss of Rs.102.58 million in 2020 with loss per share of Rs.5.17. This was against net profit of Rs.32.31 million and EPS of Rs.1.63 recorded in 2019.

In 2021, IDRT’s net sales strengthened by 23.56 percent to clock in at Rs.4002.48 million. This was on account of higher sales volume as well increased prices of yarn which allowed the company to pass on the onus of higher power tariff to its consumers.

The company also optimized the cost of raw materials by purchasing a mix of local and imported varieties of cotton. This resulted in 88.74 percent improvement in gross profit in 2021 with GP margin jumping up to 13.34 percent.

Distribution expense multiplied by 32.39 percent in 2021 due to higher freight and octroi charges as well as business promotion expenses incurred during the year.

The company was able to cut down its administrative expense by 7.47 percent in 2021 by reducing payroll expense, entertainment expense as well as travelling and conveyance expense during the year.

Provisioning done for WWF and WPPF, higher infrastructure cess and loss incurred on the modification in terms of financial assets resulted in 143.87 percent higher other expense in 2021.

However, it was partially offset by 143.61 percent higher other income recorded during the year which was primarily the consequence of unwinding of discount on other receivables. IDRT’s operating profit multiplied by 143.72 percent in 2021 with OP margin clocking in at 9.85 percent.

Finance cost slid by 28.75 percent during the year due to monetary easing and reduced short-term borrowings due to improved liquidity position. The company recorded net profit of Rs.159.80 million in 2021 with EPS of Rs.8.05 and NP margin of 4 percent.

In 2022, IDRT recorded 29 percent year-on-year improvement in its net sales which clocked in at Rs.5166.17 million. This was the result of combination of higher dispatches and upward revision in prices.

During the year, the company focused more on direct and indirect export which amid Pak Rupee depreciation resulted in higher sales value in Rupee terms. Cost of sales mounted by 25.92 percent in 2022, resulting in 49.59 percent higher gross profit with GP margin attaining its optimum level of 15.46 percent.

Increased sales volume drove the distribution expense up by 30.18 percent in 2022. Administrative expense escalated by 25.56 percent in 2022 on account of higher payroll expense.

Increased infrastructure cess and higher provisioning done for WWF and WPPF resulted in 28 percent higher other expense in 2022. Other expense was completely offset by 442.37 percent higher other income recorded during the period. This was primarily due to contract settlement charges received by the company from its suppliers who defaulted on the cotton supply contracts owing to increase in the international prices of cotton while the contracts were finalized on slightly lower prices.

The company also recognized exchange gain during the year due to Pak Rupee depreciation. Operating profit progressed by 84.19 percent in 2022 with OP margin jumping up to 14 percent.

Finance cost inched up by 1.72 percent in 2022 despite higher discount rate. This was due to lesser short-term borrowings outstanding during the year. IDRT’s net profit strengthened by 170.34 percent in 2022 to clock in at Rs.432 million with EPS of Rs.21.76 and NP margin of 8.36 percent.

IDRT recorded 18.7 percent year-on-year drop in its topline which clocked in at Rs.4200.14 million in 2023. This was due to economic slowdown which resulted in demand destruction – both locally and internationally. High energy cost, Pak Rupee depreciation as well as elevated level of inflation and discount rate also took their toll on the textile industry.

Cost of sales slid by 13.45 percent in 2023, resulting in 47.39 percent drop in gross profit with GP margin dipping to 10 percent. Lower sales volume resulted in 7.31 percent plunge in distribution expense in 2023.

Conversely, administrative expense mounted by 15.87 percent due to higher payroll expense on account of inflationary pressure. No profit related provisioning done during the year resulted in 42.85 percent slide in other expense in 2023. Other income also shrank by 67 percent in 2023 due to high-base effect as the company recorded contract settlement charges in the previous year.

Operating profit slid by 62.50 percent in 2023 with OP margin moving down to 6.48 percent. To add to ado, finance cost surged by 75.96 percent during 2023 on account of multiple rounds of monetary tightening that took place during the year.

The company’s borrowings also increased during the year particularly financing against imported merchandise, running finance and long-term financing for capacity enhancement. IDRT posted net loss of Rs. 12.49 million in 2023 with loss per share of Rs.0.63.

In 2024, IDRT recorded year-on-year topline growth of 53.56 percent. This pushed its net sales up to Rs.6449.76 million in 2024. The company enhanced its capacity from 14.8 million kgs of yarn in 2023 to 16.72 million kgs of yarn in 2024.

Capacity utilization also increased from 49 percent in 2023 to 61.30 percent in 2024. Capacity enhancement enabled the company to attain new orders both locally and internationally which played a pivotal role in driving up the sales.

The company’s home textile products made great strides in the export market. Direct and indirect export of yarn also increased during the year. Massive hike in energy tariff due to discontinuation of Regionally Competitive Energy Tariff [RCET] coupled with unavailability of good quality cotton in the local market compelled the company to use imported cotton. This resulted in 54.26 percent spike in the cost of sales in 2024.

In absolute terms, gross profit picked up by 47.23 percent in 2024, however, GP margin nosedived to 9.60 percent. Distribution expense escalated by 51.21 percent in 2024 due to surge in freight and octroi as well as clearing and forwarding charges incurred during the year.

Administrative expense inched up by 9.1 percent in 2024 due to higher payroll expense. This was despite the fact that the company squeezed its workforce from 768 employees in 2023 to 552 employees in 2024. 32.46 percent higher other expense incurred in 2024 was the result of exchange loss.

However, it was roughly offset by 8.46 percent stronger other income recorded during the year on the back of higher profit recognized on bank deposits.

Operating profit multiplied by 57.95 percent in 2024. OP margin slightly ticked up to 6.67 percent in 2024. Finance cost didn’t show any mercy and magnified by 88.92 percent in 2024. This was the consequence of higher discount rate and higher working capital related borrowings.

IDRT registered net loss of Rs.194.388 million in 2024, up 1455.86 percent year-on-year. This culminated into loss per share of Rs.9.79 in 2024.

Recent Performance (2025)

In 2025, the company recorded 19.35 percent year-on-year drop in its topline which clocked in at Rs.5201.69 million. This was particularly on the back of a drastic decline in direct and indirect export. Not only did the volumes remain under pressure, stronger Pak Rupee also squeezed the value of export sales in Pak Rupee terms.

Elevated energy tariff and use of imported raw materials due to quality issues in the local produce didn’t allow the cost of sales to shrink proportionately. This resulted in 48.55 percent thinner gross profit recorded in 2025 with GP margin hitting its lowest level of 6.12 percent.

Distribution slipped by 16.75 percent in 2025 due to lower sales volume. Conversely, administrative expense ticked up by 3.93 percent in 2025 particularly on the back of allowance booked for ECL.

Other expense dipped by 36.34 percent in 2025 due to lower exchange loss due to appreciation in the value of local currency. Other income nosedived by 29 percent during the year due to lower profit on bank deposits, lesser gain recognized on property, plant & equipments, no dividend income and no realized gain on short-term investments recorded during the year.

Operating profit slid by 67.44 percent in 2025 with OP margin falling down to 2.69 percent. Finance cost nosedived by 17.72 percent in 2025 due to monetary easing. IDRT recorded net loss of Rs.394.765 million in 2025, up 103 percent year-on-year. This translated into loss per share of Rs.19.88 in 2025.

Future Outlook

Low quality local cotton crop due to adverse weather conditions, high energy tariff, geopolitical tensions and demand supply imbalances due to uncertain foreign exchange levels are formidable challenges for the local textile industry.

On the flipside, improvement in macroeconomic indicators such as reduction in discount rate and stronger Pak Rupee will help the businesses in controlling their cost.

The company is also planning to expand its solar power capacity to reduce its energy cost. Besides, IDRT is also optimizing its product mix to improve its margins and profitability.

Comments

Comments are closed for this article.