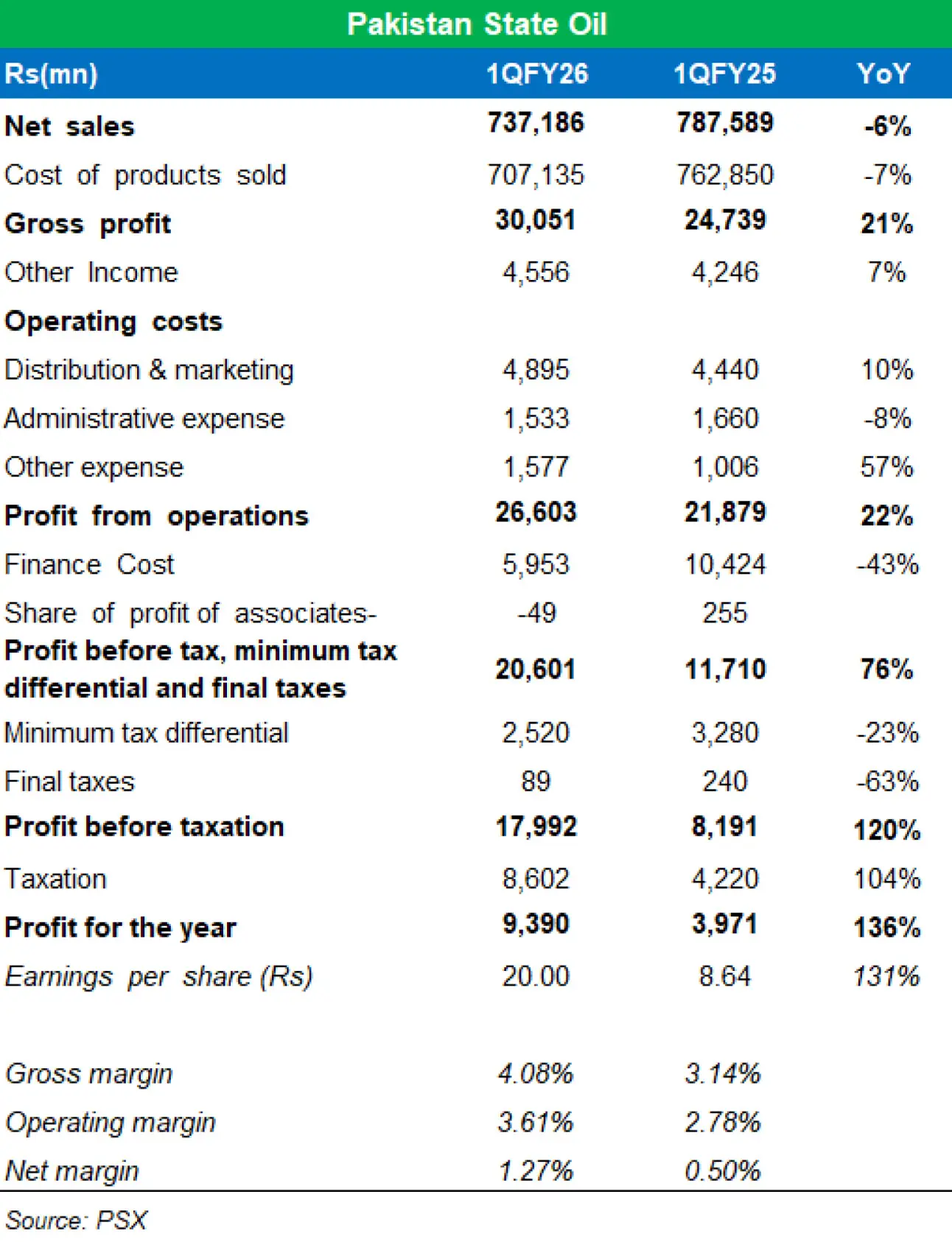

Pakistan State Oil Company Limited (PSX: PSO) delivered a strong financial performance in the first quarter of FY26, with profits more than doubling year-on-year, underpinned by higher inventory gains, lower finance costs, and improved liquidity. This comes despite a slight contraction in topline revenue, largely due to weakness in the RLNG segment.

During the quarter, the company’s net revenue fell by 6 percent year-on-year, driven by lower RLNG prices, even as volumes of key petroleum products continued to grow. Gross profit margins climbed to 4.1 percent, up from 3.3 percent in 1QFY25. Finance costs declined sharply by 43 percent year-on-year, reflecting lower interest rates and reduced short-term borrowings.

Other income rose 40 percent, supported by financial compensation on line-fill costs and stronger working capital management.

On the volume front, PSO’s Motor Spirit (MS) sales in 1QFY26 increased 1 percent year-on-year, while High-Speed Diesel (HSD) sales rose 6 percent. RLNG volumes, however, remained subdued.

The company’s liquidity position improved as receivables declined following the partial resolution of the power sector circular debt and timely payments from the gas company. This improvement eased working capital pressures, reduced reliance on borrowings, and contributed to the decline in finance costs.

The outlook for the remainder of FY26 remains broadly positive, supported by the proposed OMC margin increase by OGRA. If approved, this could provide a significant earnings uplift in the second half of the fiscal year. With liquidity already strengthening through power sector receivables and further gains expected from gas sector settlements, PSO’s profitability is expected to improve further. Gross margins are currently at their highest level in two years, while finance costs are at their lowest in several quarters.

Comments

Comments are closed for this article.