Exide Pakistan Limited (PSX: EXIDE) was incorporated in Pakistan as a private limited company in association with Chloride Group PLC of United Kingdom and was later converted into a public limited company.

The principal activity of the company is the manufacturing and sale of batteries, chemicals and acid as well as solar energy solutions. EXIDE acquired Furukawa Battery in 1991 which further strengthened its position in the industry.

Pattern of Shareholding

As on March 31, 2025, EXIDE has a total of 7.769 million shares outstanding which are held by 2825 shareholders. Directors, CEO & children have the majority stake of 75.54 percent in EXIDE followed by mutual funds holding 10.27 percent shares of the company. Local general public accounts for 7.38 percent shares of EXIDE while foreign companies hold 1.48 percent shares.

Around 1.47 percent of the company’s shares are held by insurance companies. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-25)

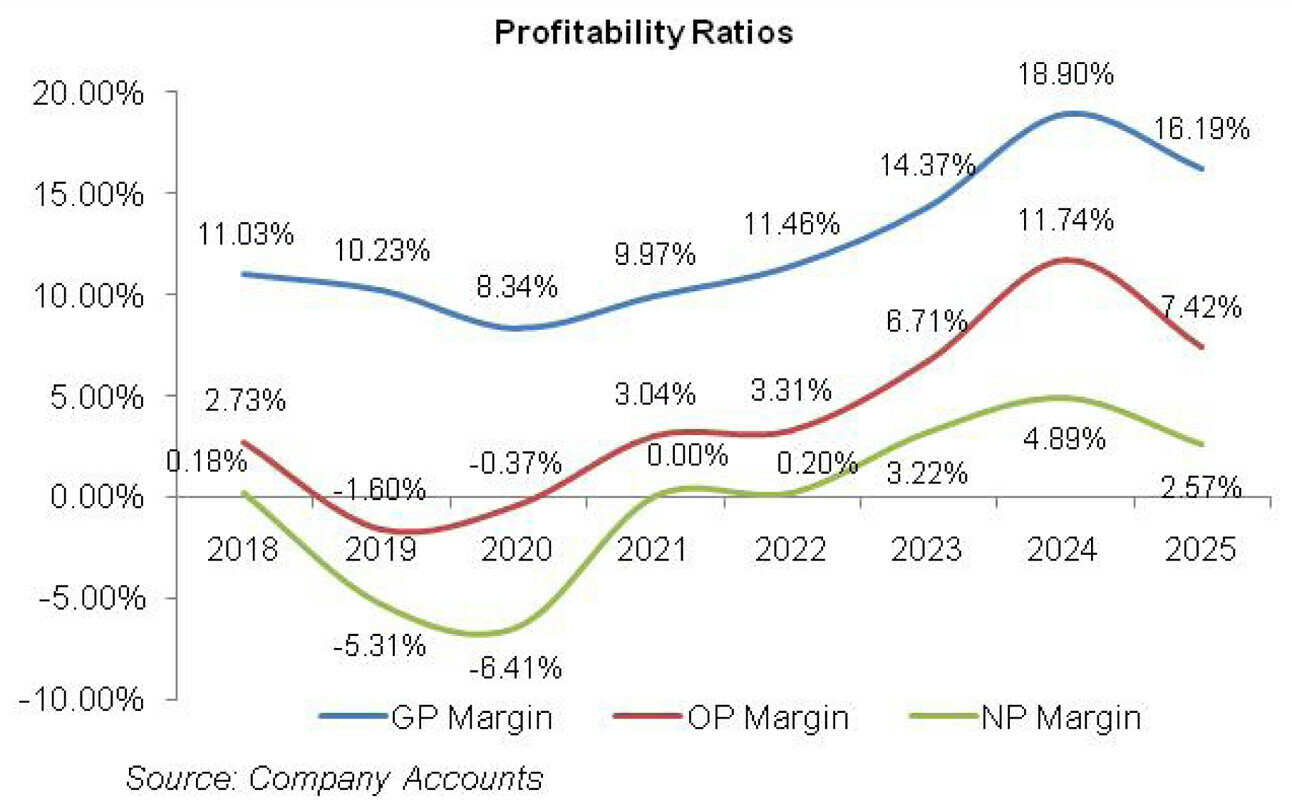

EXIDE’s topline slid in 2019 and 2020 but embarked on an uphill journey thereafter except for a downtick recorded in 2025. During the period under consideration, the company posted net losses until 2021. Subsequently, it started making profits to boast its highest ever net profit in 2024.

In 2025, EXIDE’s net profit shrank to almost half of its optimum level recorded in 2024. The company’s margins dropped until 2020 but rebounded in the subsequent years to attain their optimum level in 2024 after which it posted a dip in 2025. The detailed performance overview of the period under consideration is given below.

In 2019, EXIDE’s topline nosedived by 22.72 percent year-on-year to clock in at Rs. 9,506.58 million. This was due to massive decline in the battery sales on account of lackluster performance of automotive industry.

While rising inflation and dropping purchasing power of the consumers appeared to be the major culprits behind tamed automobile sales in 2019, restrictions on non-filers to purchase new vehicles also played its due role in suppressing the auto industry’s volumes. This created a direct impact on the sale of batteries.

While the chemical division performed better in 2019 and its net sales grew by 15 percent year-on-year in 2019, however, it constituted only 3.6 percent of the net revenue of EXIDE in 2019 and hence couldn’t produce much of a difference in its topline.

Owing to high prices of refined and recycled lead coupled with the depreciation of Pak Rupee, gross profit dropped by 28.33 percent year-on-year, with GP margin clocking in at 10.23 percent in 2019, down from GP margin of 11 percent posted in 2018. 8 percent higher distribution expense incurred in 2019 was the result of higher provisioning against battery warranty claims coupled with increased advertising and promotion budget dedicated to cope up with the intense competition prevailing in the market.

Administrative expense also grew by 11.51 percent year-on-year in 2019 due to higher payroll expense on account of inflation. The rise in payroll expense was despite considerable drop in the number of employees from 477 in 2018 to 374 in 2019 due to low capacity utilization.

Other income grew by 54.33 percent year-on-year in 2019 due to reversal of rent and higher scrap sales made during 2019. Other expense also mounted by 50.27 percent year-on-year in 2019 mainly on the back of exchange loss. This culminated into operating loss of Rs.151.73 million in 2019 as against operating profit of Rs.336.22 million registered in 2018.

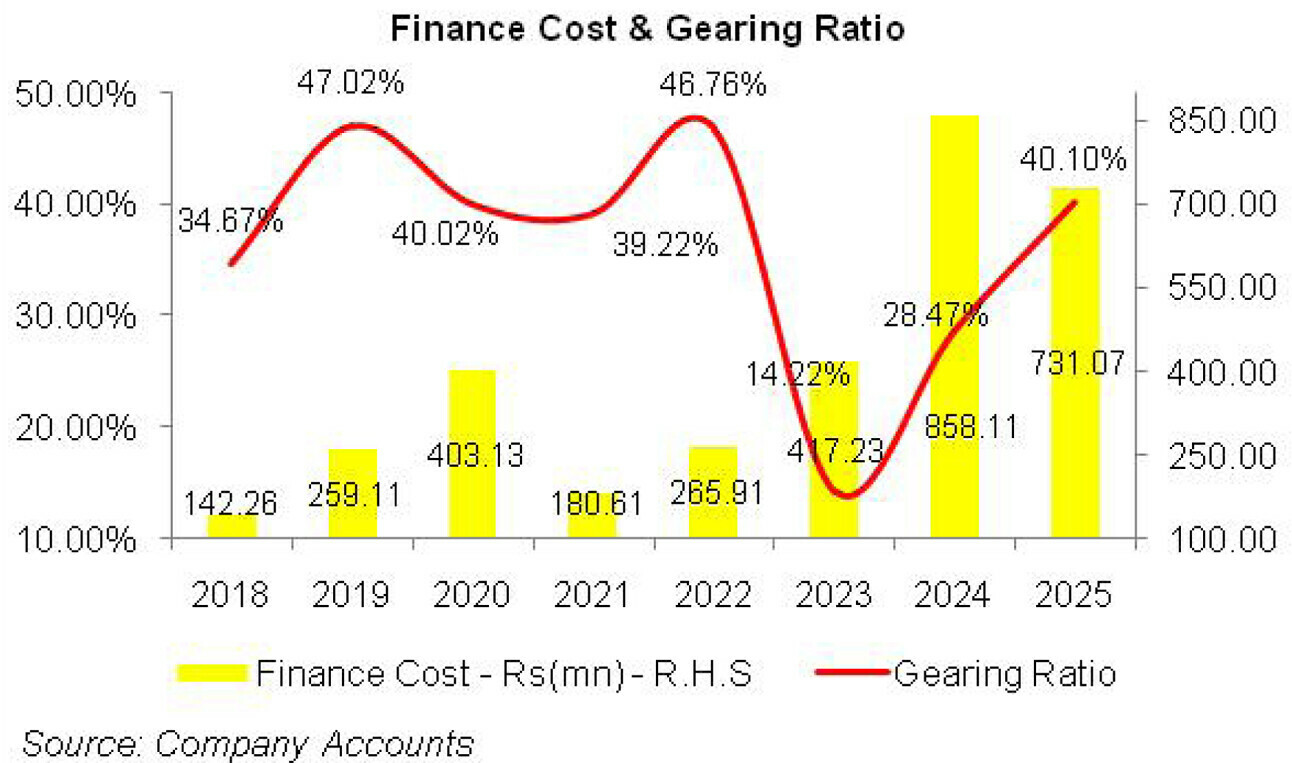

To make things worse, finance cost also posted 82.14 percent year-on-year spike in 2019 due to higher discount rate coupled with increased short-term borrowings to meet working capital requirements. EXIDE’s gearing ratio grew from 34.67 percent in 2018 to 47.02 percent in 2019.

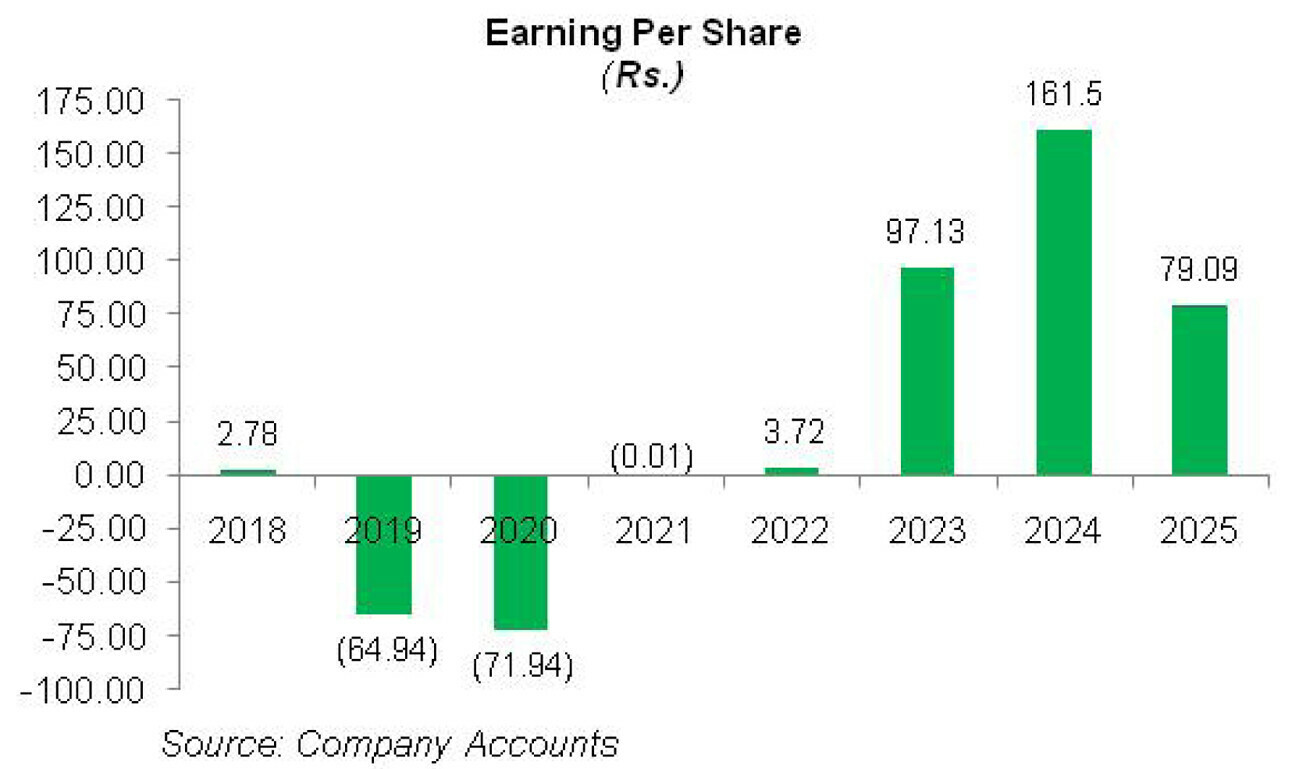

The company made net loss of Rs.504.51 million in 2019 as against net profit of Rs.21.62 posted in 2018. Loss per share stood at Rs.64.94 in 2019 versus EPS of Rs.2.78 recorded in 2018.

In 2020, EXIDE’s topline further shrank by 8.25 percent year-on-year to clock in at Rs.8,722.28 million. This was on the back of 55 percent slippage in the automobile sales during the year due to high inflation and discount rates which kept the prospective buyers at bay. This translated into weak performance of the battery division in 2020.

Low sales coupled with high cost of production resulted in 25.21 percent year-on-year erosion in EXIDE’s gross profit with GP margin ticking down to 8.34 percent in 2020.

Distribution and administrative expense also shrank by 19.22 percent and 4.46 percent respectively in 2019. This was due to considerably lesser advertisement and promotion charges as well as provision against battery warranty claims.

The number of employees was further streamlined to 354 in 2020 which also kept the payroll expense in check. Other income posted a staggering rise of 799.40 percent year-on-year in 2020 due to gain recognized on the disposal of property, plant and equipment.

Other expense, on the other hand, plummeted by 36.87 percent year-on-year in 2020 due to lesser exchange loss as the company imported lesser raw materials due to reduced demand. Operating loss tapered off by 78.45 percent year-on-year in 2020 to clock in at Rs.32.69 million in 2020.

Finance cost grew by 55.58 percent year-on-year in 2020 due to higher borrowings and increased discount rate. During 2020, the company also restructured its running finance facility into a term loan as consistent losses rendered the company unable to settle its short-term financial commitments.

Gearing ratio fell to 40.02 percent in 2020. Higher finance cost resulted in 10.77 percent year-on-year intensification in EXIDE’s net loss which clocked in at Rs.558.85 million in 2020 with loss per share of Rs.71.94.

The net sales of EXIDE which had been declining since 2019 rebounded to the tune of 34.32 percent to clock in at Rs. 11,715.57 million in 2021. This was on account of encouraging performance of the automotive industry on the back of low discount rate and better farm income.

Gross profit improved by 60.60 percent year-on-year in 2021 with GP margin marching up to 9.97 percent. Despite better sales volume, distribution expense sank by 9.46 percent year-on-year in 2021 on account of a steer on the advertisement and promotion charges, lower carriage and forwarding charges and lower provisioning against battery warranty claims.

Administrative expense inched up by 11.83 percent year-on-year in 2021 due to market induced increase in salaries despite a downtick in the number of employees to 343.

Other income slipped by 76.81 percent year-on-year in 2021 due to one-off gain recognized on the sale of property, plant and equipment in the previous year. This diluted the impact of exchange gain of Rs.22.7 million recognized by EXIDE in 2021 on account of appreciation in the value of local currency.

Stronger Pak Rupee also trimmed down other expense by 35.26 percent year-on-year in 2021 due to no exchange loss incurred during the year. After two years of booking operating losses, the company was able to post operating profit of Rs.356.30 million in 2021 which culminated into OP margin of 3 percent. Finance cost also proved to be favorable as it contracted by 55.20 percent year-on-year in 2021 due to monetary easing and reduced borrowings during the year.

Gearing ratio further lowered to 39.22 percent in 2021. While EXIDE made profit-before-tax of Rs. 175.69 million in 2021, 43 percent higher taxation resulted in net loss of Rs.0.04 million in 2021 with loss per share of Rs.0.01.

The growth trajectory continued in 2022 as EXIDE’s topline rose by another 22.59 percent year-on-year to clock in at Rs.14,362.60 million. This was due to superior performance of automotive industry as well as considerable upward revision in prices. Cost of sales grew by 20.56 percent year-on-year, yet gross profit improved by 40.93 percent year-on-year, culminating into GP margin of 11.46 percent in 2022.

Distribution expense multiplied by 42.69 percent year-on-year in 2022 due to significantly higher provision booked against battery warranty claims coupled with high carriage and forwarding charges. Administrative expense also grew by 17.10 percent year-on-year in 2022 due to higher salaries and wages despite the fact that the number of employees climbed down to 325 in 2022.

Other income narrowed down by 51.71 percent year-on-year in 2022 as the company recognized no exchange gain and no scrap sales during the year. Other expense grew by 43.66 percent year-on-year in 2022 due to exchange loss incurred during the year. Operating profit picked up by 33.56 percent year-on-year in 2022 with OP margin jumping up to 3.31 percent.

Finance cost grew by 47.24 percent year-on-year in 2022 due to higher working capital requirements and upward revision in discount rate. With increased borrowings, gearing ratio again swelled up to 46.76 percent in 2022.

However, after three years of sustained net losses, 2022 proved to be a breath of fresh air for EXIDE as it witnessed net profit of Rs.28.86 million. EPS clocked in at Rs. 3.72 while NP margin was recorded at 0.20 percent.

The lucky streak continued in 2023 whereby the company boasted a staggering 62.94 percent year-on-year growth in its topline which clocked in at Rs.23,402.18 million. The automobile sales were not encouraging in 2023 due to Pak Rupee depreciation, import restrictions, commodity super cycle in the global market as well as high auto financing rates during the year.

While automobile and industrial batteries didn’t perform well owing to economic and political turmoil and slowdown of business activity, household batteries seem to have performed well due to increased hours of electricity load shedding.

The company was also able to drive its prices upward to make the most of high demand. Gross profit improved by 104.34 percent year-on-year in 2023 with GP margin climbing up to 14.37 percent.

Distribution and administrative expenses widened by 34.79 percent and 35 percent respectively in 2023. This was due to higher carriage and forwarding charges coupled with increased provisioning against warranty claims. The company further drove down its human resource count to 323 in 2023, yet elevated inflation resulted in higher payroll expense.

Other income posted a marginal 1.97 percent rise on the back of improved profit on bank accounts. Other expense posted 253.59 percent year-on-year growth due to higher provisioning done for WWF and WPPF as well as higher exchange loss. During 2023, EXIDE also booked an allowance of Rs.160.64 million against expected credit losses.

Despite elevated expenses, operating profit magnified by 229.86 percent year-on-year in 2023 with OP margin of 6.71 percent. Finance cost posted 56.90 percent year-on-year growth in 2023 due to higher borrowings and discount rate. Gearing ratio slid down to 14.22 percent in 2023 due to increase in cash and bank balances as of March 2023 on account of better profitability.

EXIDE posted net profit of Rs.754.56 million in 2023, up 2514.29 percent year-on-year with NP margin of 3.22 percent. EPS jumped up to Rs.97.13 in 2023.

In 2024, EXIDE posted 9.68 percent year-on-year rise in its topline which climbed up to Rs.25,667.602 million. Auto industry posted its multi-year low volumes in 2024 due to economic headwinds, unrelenting energy shortfalls and high financing rates, however, high energy cost and rising demand of solar power projects provided impetus for increased battery sales during the year.

Higher demand allowed the company to attain price rationalization which translated into 44.27 percent improved gross profit in 2024 with GP margin climbing up to its highest level of 18.90 percent.

Distribution expense inched up by 7.5 percent in 2024 due to higher carriage & forwarding charges, advertising & promotion expense as well as payroll expense of sales force. Battery warranty claims although posted a downtick in 2024, however, still constituted 46.91 percent of EXIDE’s overall distribution expense.

Administrative expense mounted by 39.85 percent in 2024 primarily due to higher payroll expense while number of employees stood at 322 versus 323 in the previous year. Other income posted a paltry 4.24 percent growth in 2024 due to gain on the disposal of property, plant and equipment recorded during the year. EXIDE booked 76.67 percent lower allowance for ECL in 2024.

While the company booked significantly higher provisioning for WWF and WPPF in 2024, it was greatly offset by lower exchange loss. This translated into a thin 3.90 percent rise in other expense in 2024.

Operating profit strengthened by 91.94 percent in 2024 with OP margin jumping up to 11.74 percent. Finance cost spiked by 105.67 percent in 2024 due to exorbitant discount rate and higher working capital related borrowings. Gearing ratio swelled to 28.47 percent in 2024. Net profit picked up by 66.27 percent in 2024 to clock in at Rs.1254.62 million with EPS of Rs.161.50 and NP margin of 4.89 percent.

2025 was the first year after 2020 where the company posted a decline in its topline. During the year, EXIDE’s net sales dropped by 6.91 percent to clock in at Rs.23,895.008 million. This was due to reduced sales volume and prices as domestic and industrial customers were discouraged by the government to switch to solar power projects in an effort to increase the utilization of the national grid. This pushed the battery manufacturers to reduce its prices, resulting in 20.25 percent decline recorded in EXIDE’s gross profit in 2025 with GP margin falling down to 16.19 percent.

Distribution expense spiraled by 19.97 percent in 2025 due to massive spike in battery warranty charge, carriage & forwarding charges, advertising & promotion expense as well as salaries of sales force.

Administrative expense also escalated by 21.64 percent in 2025 due to higher payroll expense which was on account of inflationary pressure as well as workforce expansion from 322 employees in 2024 to 327 employees in 2025.

Other income weakened by 82.28 percent in 2025 due to considerable decline in profit on bank deposits as well as one-off gain on the disposal of property, plant & equipment recorded in the previous year.

Allowance for ECL further dwindled by 16.24 percent in 2025. Substantial reduction in profit related provisioning brought about 47.31 percent diminution in other expense in 2025.

All these factors translated into 41.17 percent plunge in operating profit in 2025 with OP margin falling down from its optimum level to 7.42 percent. Finance cost was tapered off by 14.81 percent in 2025 due to monetary easing. This was despite increased borrowings obtained during the year which pushed up the company’s gearing ratio to 40.11 percent in 2025.

Net profit almost halved to clock in at Rs.614.436 million in 2025 with EPS of Rs.79.09 and NP margin of 2.57 percent.

Recent Performance (Quarter ended June 30, 2025)

During the first quarter ended June 30, 2025, EXIDE’s net sales dipped by 14.92 percent year-on-year dip in its net sales. This was mainly on account of reduction in sales prices. Reduced purchasing power of consumers and increased competition forced the company to adjust its prices in order to stay competitive. This resulted in 33 percent lower gross profit in 1QFY25 and GP margin clocking in at 14.65 percent versus GP margin of 18.63 percent recorded in 1QFY24.

Distribution and administrative expense dipped by 23.67 percent and 9.78 percent respectively in line with the company’s strategy to rationalize its operating expenses. 6.53 percent drop in other income during 1QFY25 appears to be the result of lower profit on bank deposits due to monetary easing. Other expense also thinned down by 29 percent due to lower provisioning done for WWF and WPPF.

EXIDE recorded 40 percent weaker operating profit in 1QFY25 with OP margin clocking in at 7.85 percent versus OP margin of 11.15 percent recorded in 1QFY24. Decline in discount rate translated into 11.58 percent diminution in finance cost in 1QFY25. The company recorded net profit of Rs. 223.335 million in 1QFY25, down 48.58 percent year-on-year. This translated into EPS of Rs. 28.75 in 1QFY25 versus EPS of Rs. 55.91 registered in 1QFY24. NP margin deteriorated from 5.24 percent in 1QFY24 to 3.17 percent in 1QFY25.

Future Outlook

The government is discouraging captive power plants and incentivizing the industries to return to the national grid by increasing the gas prices to the CPPs by up to 23 percent and imposing a grid levy. Furthermore, industries are also directed to ensure dual connectivity. This can put a dent on the sale of solar batteries.

While the auto industry registered significant improvement of-late due to better financing rates, easing inflationary pressure and strengthened customer confidence, reduction in additional customs duties and regulatory duties will foster the import of used vehicles, thereby taking a toll on the local manufacturing.

The introduction of NEV levy across all internal combustion vehicles including trucks & buses and restriction on the purchase of new vehicles by non-filers may take its toll on the automobile sales and ultimately automotive battery sales. While the downward pressure remains, the key to remain competitive is cost control, quality enhancement and better after sales support.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.