Nishat Power Limited (PSX: NPL) was incorporated in Pakistan as a public limited company in 2007. The company owns, operates, and maintains a fuel fired power station having gross capacity of 200MW in Jamber Kalan, Tehsil Pattoki, District Kasur, Punjab, Pakistan. The company is a subsidiary of Nishat Mills Limited.

Pattern of Shareholding

As of June 30, 2024, NPL has a total of 354.089 million shares outstanding which are held by 4743 shareholders. Nishat Mills Limited, the parent company of NPL, holds 51.0135 percent of its shares followed by local general public holding 35.45 percent shares.

Banks, DFIs and NBFIs have 6.80 percent stake in the company while Modarabas & Mutual Funds account for 2.24 percent shares. Around 1.39 percent of the company’s shares are held by insurance companies and 0.97 percent by foreign general public. The remaining share is held by other categories of shareholders.

Financial Performance (2019-24)

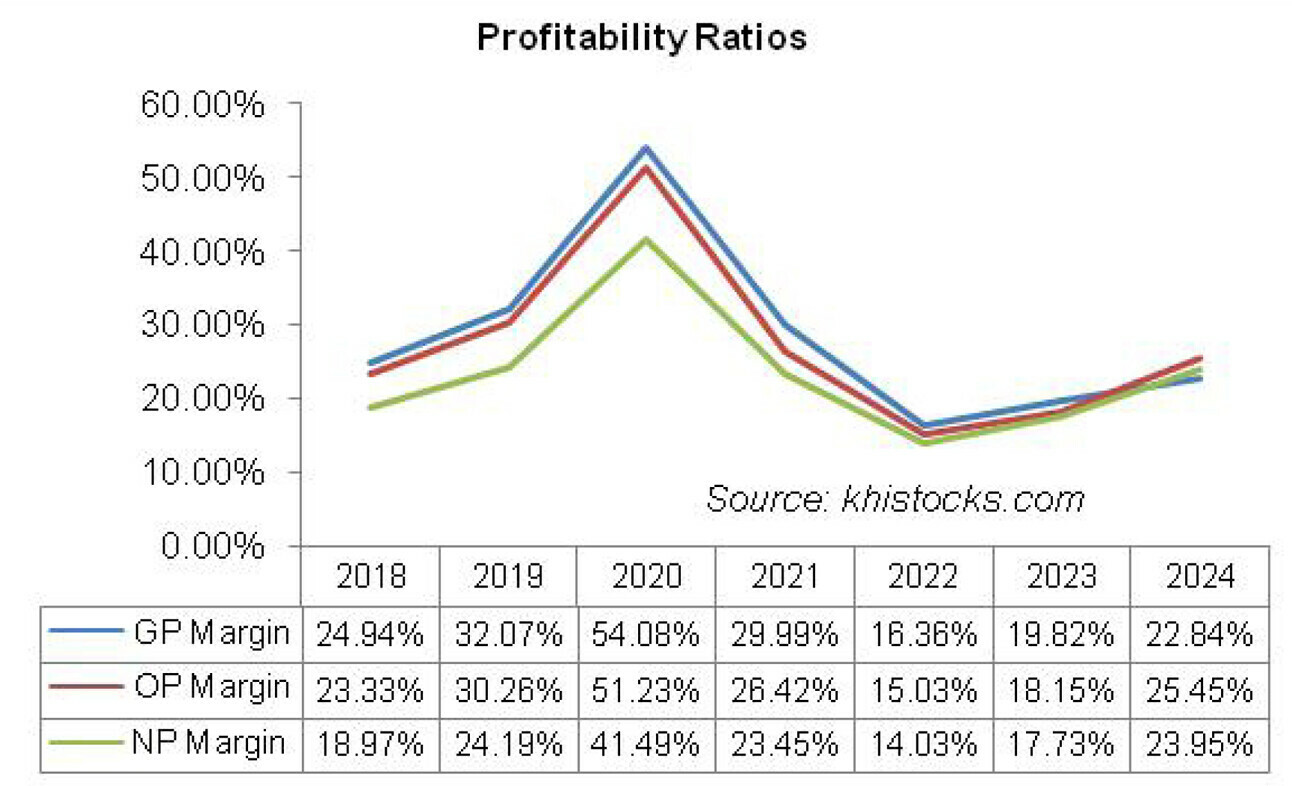

NPL’s topline posted year-on-year growth only in 2022, yet its bottomline was able to muster significant growth in all the years under consideration except 2021. Its margins took a steep upward flight until 2020 followed by a decline in the subsequent two years. In 2023 and 2024, NPL’s margins posted uptick. The detailed performance review of the period under consideration is given below.

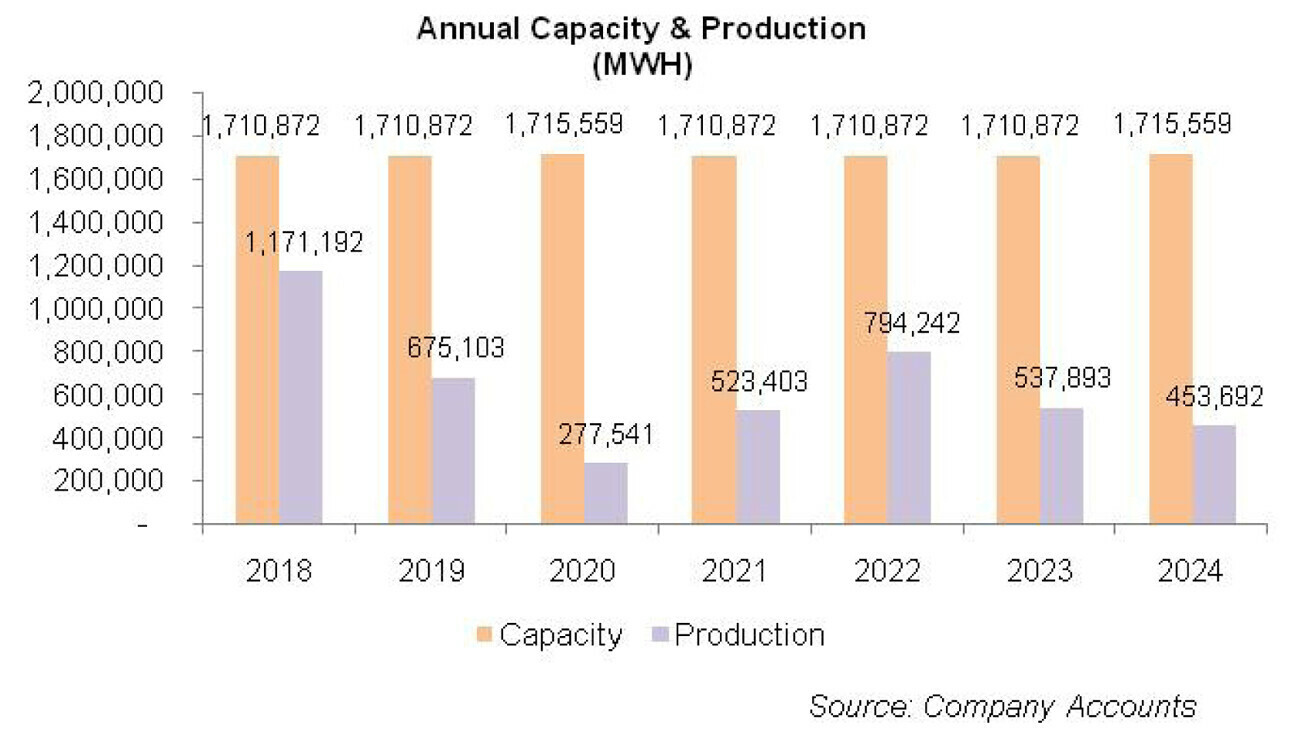

In 2019, NPL’s topline slid by 7.96 percent year-on-year to clock in at Rs.15,581.92 million. During the year, the plant operated at a capacity of 39.46 percent and dispatched 675 GWh of electricity to National Transmission & DispatchCompany Limited (NTDCL). This was against the capacity utilization of 68.27 percent achieved in 2018 which translated into 1171 GWh of electricity provided to NTDCL.

The decline was on account of increased power generation in the country which increased the avenues available to the Ministry of Energy. Cost of sales slid by16.71 percent in 2019, resulting in18.38 percent higher gross profit with GP margin of 32 percent versus GP margin of 24.94 percent attained in 2018.

Administrative expense slumped by 14.45 percent in 2019 due to a massive fall in legal & professional charges during the year. 88.44 percent thinner legal & professional chargeincurred during 2019 was partially offset by higher payroll expense, travelling & conveyance charges, and depreciation expense.

Other expense mounted by a whopping 473.43 percent in 2019 on account of loss of disposal of operating fixed assets recorded in 2019. Other income shrank by 85.69 percent in 2019 due to high-base effect as NPL recorded insurance receipts against business interruption loss in 2018.

All these factors resulted in 19.38 percent year-on-year increase in operating profit in 2019. This translated into OP margin of 30.26 percent versus OP margin of 23.33 percent registered in 2018.

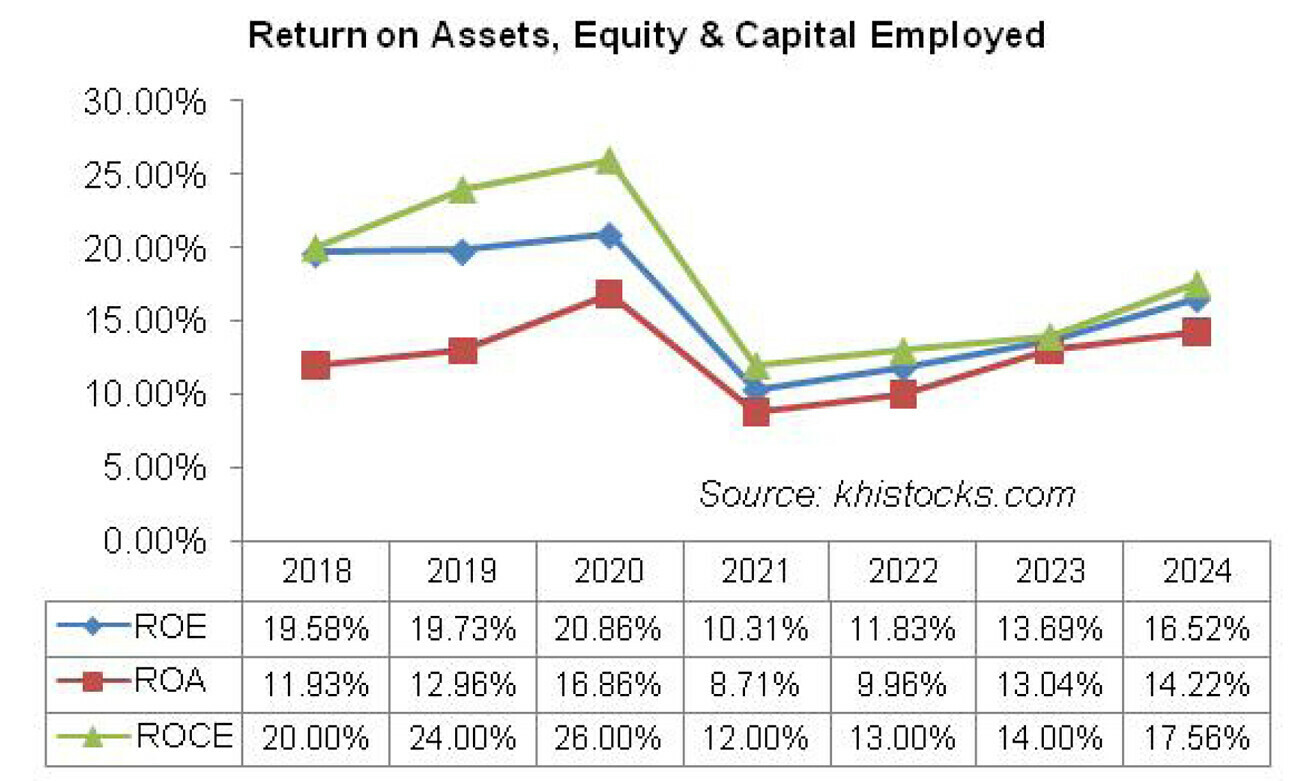

Finance cost surged by 28.25 percent in 2019 due to monetary tightening as well as increased running finances obtained during the year. NPL’s gearing ratio mounted to 49 percent in 2019 as against gearing ratio of 36.75 percent posted in the previous year.

The company recorded net profit of Rs.3769.549 million in 2019, up 17.38 percent year-on-year. This culminated into EPS of Rs.10.646 in 2019 versus EPS of Rs.9.07 recorded in 2018. NP margin stood at 24.19 percent in 2019 versus NP margin of 18.97 percent posted in 2018.

In 2020, NPL’s revenue tumbled by 24.67 percent to clock in at Rs.11,738.49 million This was on account of low demand from NTDC due to increased power generation in the country coupled with depresseddemand due to COVID-19.

NPL’s plant operated at a thin capacity of 16.18 percent in 2020 and dispatched 278 GWh of electricity to NTDC. Cost of sales slipped by 49 percent, translating into 27 percent higher gross profit and GP margin of 54 percent recorded by NPL in 2020.

Administrative expense grew by 22.81 percent in 2020 due to higher payroll expense, travelling & conveyance charges, legal & professional charges as well as depreciation on operating fixed assets.

The company streamlined its workforce to 209 employees in 2020 from 218 employees in 2019 due to curtailed operations. Other expense dwindled by 66.17 percent in 2020 as the company didn’t incur any exchange loss and loss on disposal of operating fixed assets in 2020. Other income stayed afloat due to gain recorded on the disposal of operating fixed assets in 2020 which offset lower profit earned on bank deposits.

NPL recorded 27.53 percent higher operating profit in 2020, culminating into OP margin of 51.23 percent. Finance cost surged by 20.82 percent in 2020 despite drop in the outstanding liabilities as the company paid its entire long-term debt to banks. Debt servicing was a part of tariff resulting in corresponding reduction in capacity purchase price (CPP) revenue for the following years.

Gearing ratio dropped to 20 percent in 2020. NPL’s net profit strengthened by 29.21 percent in 2020 to clock in at Rs.4870.585 million with EPS of Rs.13.755 and NP margin of 41.49 percent.

In 2021, NPL’s net revenue nosedived by 2.61 percent year-on-year to clock in at Rs.11,432.57 million. While capacity utilization greatly increased to 30.59 percent during the year, reduced CPP revenue due to the repayment of long-term debt in the previous year resulted in a plunge in NPL’s topline in 2020.

The company dispatched 523 GWh of electricity to NTDC in 2021. Cost of sales escalated by 48.48 percent in 2021 due to elevated price of raw materials consumed during the year, particularly fuel. This resulted in 46 percent weaker gross profit recorded by NPL in 2021 with GP marginfalling drastically down to 30 percent.

Administrative expense plummeted by 10.22 percent in 2021 primarily due to lower payroll expense and legal & professional charges. The company further trimmed down its workforce to 205 employees in 2021. 2928.42 percent higher other expense incurred by NPL in 2021 indicated capacity receivables of Rs.162.717 million written off during the year. This was due to the under utilization of plant capacity on account of non-availability of fuel owing to non-payment by NTDC.

The company raised this issue in London Court of International Arbitration (LCIA); however, it had to forgo certain amount and hence wrote it off during the year. Other income grew by 676.74 percent in 2021 due to massive gain recognized on the disposal of operating fixed assets during the year.

The company recorded 49.77 percent lower operating profit in 2021 with considerably lower OP margin of 26.42 percent. Finance cost dipped by 70.31 percent in 2021 due to monetary easing and reduced borrowings. Gearing ratio also fell to 13 percent in 2021.

Higher fuel chargeselevated other expense and reduced CPP revenue led to 44.95 percent decline in NPL’s net profit in 2021 which stood at Rs.2681.13 million with EPS of Rs.7.57 and NP margin of 23.45 percent.

As compared to previous year, NPL’s topline grew by a staggering 107.17 percent to clock in at Rs.23,684.34 million in 2022. This was on account of increased capacity utilization of 46.42 percent recorded in 2022 which translated into dispatch of 794 GWh of electricity to NTDC.

Cost of sales surged by 147.5 percent in 2022 due to increased raw material prices coupled with currency depreciation. Gross profit inched up by 13 percent in 2022, however, GP margin fell down to 16.36 percent – the lowest among all the years under consideration. 10.62 percent year-on-year hike in administrative expense in 2022 was primarily the effect of elevated payroll expense.

Other expense shrank by 55 percent in 2022 as the company wrote off capacity receivables during the last year. Other expense was conveniently offset by 61.3 percent higher other income recorded by NPL in 2022. Improved other income was the result of higher profit on bank deposits, increased scrap sales and gain on disposal of operating fixed assets.

NPL’s operating profit inched up by 17.83 percent in 2022; however, OP margin fell to 15 percent. Despite soaring discount rate, NPL was able to cut down its finance cost by 30.48 percent in 2022. Gearing ratio was recorded at 14 percent in 2022. Net profit grew by 23.93 percent year-on-year to clock in at Rs.3322.606 million in 2022 with EPS of Rs.9.38 and NP margin of 14 percent.

The upward journey of NPL’s topline reversed yet again as it posted year-on-year fall of 2.6 percent in its net sales which clocked in at Rs.23,068.96 million in 2023.

The slowdown of economic activity resulted in reduced power generation demand in the country. Hence, NPL operated at a reduced capacity of 31.44 percent and transmitted 538 GWh of electricity to NTDC in 2023. Cost of sales plunged by 6.63 percent in 2023, resulting in 18 percent higher gross profit with GP margin moving up to 19.82 percent.

Administrative expense surged by 20 percent in 2023 due to higher salaries as well as travelling & conveyance charges incurred during the year. The company enhanced its workforce from 207 employees in 2022 to 214 employees in 2023.

Other expense magnified by a whopping 122.41 percent in 2023 on account of massive exchange loss, loss on disposal of short-term investments and trade debts written off during the year. Other expense was set off by 95.57 percent higher other income recorded by NPL in 2023 due to improved profit on bank deposits and TDRs, increased scrap sales and insurance claims. Operating profit grew by 17.67 percent in 2023 with OP margin inching up to 18.15 percent.

Finance cost dipped by 62.50 percent in 2023 as the company paid off its entire short-term and long-term liabilities during the year which drove its gearing ratio down to 0 percent.

While the core income of the company is exempt from income tax levy, higher other income translated into income tax of Rs.8.06 million in 2023, up 2037.67 percent year-on-year. NPL’s net profit grew by 23.13 percent in 2023 to clock in at Rs.4091.029 million with EPS of Rs.11.56 and NP margin of 17.73 percent.

NPL’s revenue continued to fall with a decline of 2.44 percent recorded in 2024. Net sales clocked in at Rs.22,505.489 million in 2024. Due to reduced power generation demand, the company operated at a capacity of 26.45 percent and dispatched 454 GWh of electricity to the national grid in 2024.

Cost of sales dipped by 6.11 percent during the year due to higher fuel and O&M savings. This translated into 12.40 percent improvement in gross profit and GP margin clocking in 22.84 percent in 2024. 20.15 percent higher administrative expense incurred in 2024 was the impact of higher payroll as well as travelling &conveyance charges incurred during the year.

NPL incurred higher payroll expense despite the fact that it streamlined its workforce from 214 employees in 2023 to 210 employees in 2024. Other expense shrank by 94.43 percent in 2024 as Pak Rupee strengthened against the greenback during the year, resulting in no exchange loss.

Moreover, unlike last year, NPL didn’t incur any loss on disposal of short-term investments and didn’t write off any trade debts in 2024.Other income strengthened by 504.54 percent in 2024 owing to dividend income recognized from the mutual funds of MCB Investment Management Limited, gain recorded on the disposal of government T-bills and PIBs as well as higher profit on bank deposits and TDRs.

NPL recorded 36.78 percent higher operating profit in 2024 with OP margin moving up to 25.45 percent. Finance cost marched down by 61.96 percent in 2024 due to lesser interest payment due on outstanding loans. Due to improvement in other income, tax expense grew by 3677.13percent in 2024. NPL was able to record 31.74 percent higher net profit to the tune of Rs.5389.574 million in 2024 with EPS of Rs.15.22and NP margin of 23.95 percent.

Recent Performance (9MFY25)

Although the company’s topline dipped in the previous years, it was able to make robust net profit. However, during 9MFY25, not only did NPL’s net sales drastically drop by 69.48 percent to clock in at Rs.5215.524 million, but the company also recorded a sizeable net loss. During the period under consideration, the government of Pakistan constituted a task force to make amendments in the power purchase agreement, implementation agreement and tariff.

NPL, along with other IPPs underwent several rounds of negotiations with the task force and the result was the conversion of existing tariff to “Hybrid Take & Pay Model.” During 3QFY25, all the parties fully implemented this model. As per the amendment agreement, the power purchaser also made full payment of overdue claims of the company.

However, due to adjustment in receivables from the power purchaser as per the amendment agreement, the company had to incur net loss in 9MFY25. NPL operated its plant at 4 percent capacity and dispatched only 51GWH of electricity in 9MFY25 versus capacity utilization of 26.57 and dispatch of 342 GWH electricity recorded in 9MFY24. Gross profit slid by 37.46 percent in 9MFY25; however, GP margin improved from 21.31 percent in 9MFY24 to 43.68 percent in 9MFY25.

Administrative expense mounted by 13.79 percent in 9MFY25 due to inflationary impact. Other income strengthened by 37.51 percent in 9MFY25 seemingly due to higher dividend income from investments. Operating profit dwindled by 28.46 percent in 9MFY25 with OP margin clocking in at 55 percent versus OP margin of 23.50 percent recorded in 9MFY24.

Finance cost escalated by 101.81 percent in 9MFY25 despite monetary easing. This was due to payment of its entire short-term liabilities during the period. What turned the tables for NPL in 9MFY25 was the adjustment made to balance payable by CPPA-G. This was on account of the company’s consent under the amendment agreement to waive off delayed payment mark-up invoices and delayed payment mark-up accrued with respect to the payments made by the power purchaser up to October 31, 2024.

Under the agreement, NPL also agreed to share prior years’ earnings relating to fuel and O&M up to June 30, 2023, with the power purchaser. As a result, the company recorded net loss of Rs.2112.848 million and loss per share of Rs.5.97 in 9MFY25 versus net profit of Rs.3857.575 million and EPS of Rs.10.89 recorded in 9MFY24.

Future Outlook

Power generation is likely to rise in the ongoing quarter due to seasonal impact. However, year-on-year, electricity generation has been waning due to demand destruction from domestic consumers on account of rooftop solar generation as well as sluggish demand from industrial and commercial consumers due to slowdown of economy.

Comments

Comments are closed for this article.