Metropolitan Steel Corporation Limited (PSX: MSCL) was incorporated in Pakistan as a public limited company in 1955. The company is engaged in the manufacturing of steel products such as torsteel, ribbed bars, bailing hoops, wire rods, transmission towers, mild and special steel wires etc.

Pattern of Shareholding

As of June 30, 2024, MSCL has a total of 30.978 million shares outstanding which are held by 3609 shareholders. Directors, CEO, their spouse and minor children are the major shareholders of MSCL holding 75.23 percent shares of the company followed by local general public having a stake of 24 percent in the company. The remaining shares are held by other categories of shareholder.

Historical Performance (2019-24)

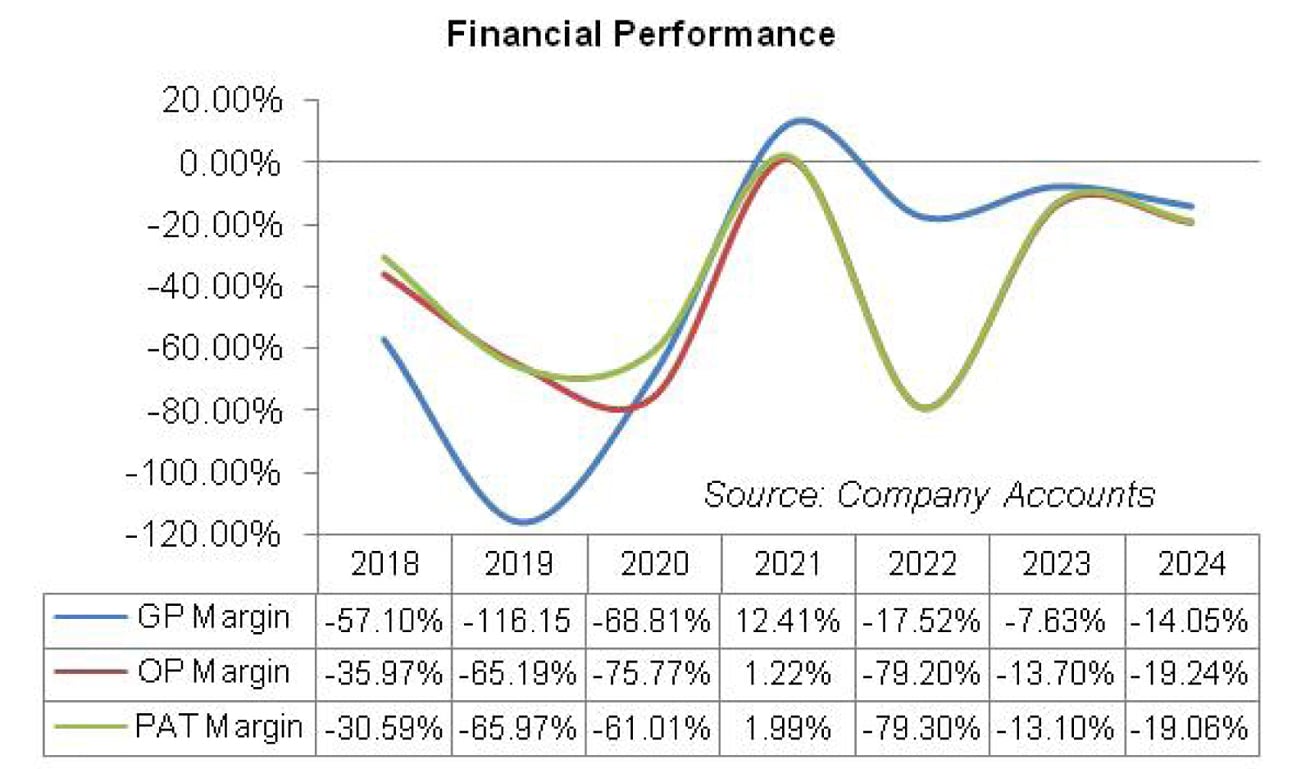

MSCL’s topline dropped in 2019 and 2020 and then posted a staggering year-on-year growth in 2021. The growth trajectory continued in the subsequent year, however with a significantly lesser magnitude. In 2023, MSCL’s net sales ticked down followed by a rebound in 2024.

Among all the years under consideration, the company posted net profit only in 2021. In rest of the years under consideration, the company was not even able to post gross profit, let alone positive bottomline. In 2022, MSCL posted the highest net loss despite topline growth. The detailed performance review of the period under consideration is given below.

In 2019, MSCL’s net sales dropped by 48.94 percent year-on-year to clock in at Rs.28.229 million. During 2019, the company imported various products at competitive prices and dispatched them in the local market. While cost of sales also slid by 29.75 percent year-on-year, yet, couldn’t culminate into gross profit in 2019.

In fact, MSCL’s gross loss grew by 3.85 percent year-on-year in 2019 to clock in at Rs.32.788 million. This was mainly due to the payments made to K-Electric and SSGC for the installation of new connections as the company modernized its plant and machinery and undertook expansion of its furnaces.

Moreover, cost of sales was also pushed up by depreciation charge recorded on building, plant and machinery in 2019. Administrative charges dropped by 12.40 percent year-on-year in 2019 on the back of lower payroll expense, legal and professional charges, utility charges etc incurred during the year.

Selling and distribution expense which merely included depreciation charge also slid by 54 percent year-on-year in 2019. In the previous year, the company wrote down its stock-in-trade to net realizable value and also wrote off guarantee margins and reversal of liabilities which wasn’t done in 2019.

Hence no other expense was recorded in 2019. Other income also declined by 51.29 percent year-on-year in 2019 as the company incurred realized and unrealized loss on its investments in 2019.

MSCL’s operating loss dropped by 7.45 percent year-on-year in 2019 to clock in at Rs.18.513 million. Finance cost which only included bank charges in 2018 grew by 909 percent year-on-year in 2019 mainly on the back of commission paid on Letter of Credit and Letter of Guarantee.

Net loss grew by 10.12 percent year-on-year in 2019 to clock in at Rs.18.62 million. This translated into loss per share of Rs.0.60 versus loss per share of Rs. 0.55 recorded in 2018.

MSCL’s topline continued its downward trajectory in 2020 and dropped by 2.94 percent year-on-year to clock in at Rs.27.399 million. Owing to the outspread of COVID-19, the economic activities came to a standstill which put a dent on the demand of steel and related products.

Although the company kick-started 2020 on a robust note and introduced spoke wires for the automobile industry which was well received by the market, however, the lockdown imposed in the last quarter of 2020 took its toll on the overall sales of the company.

Cost of sales dipped by 24.20 percent year-on-year on account of lesser utility charges which amplified in the previous year as the company paid for the installation of new connections. Gross loss dipped by 42.5 percent year-on-year in 2020 to clock in at Rs.18.85 million.

Administrative expenses shrank by 35.31 percent year-on-year in 2020 on the back of lower travelling and conveyance, fee and subscription and utility charges incurred during the year. Distribution expense grew by 1094.12 percent to clock in at Rs. 0.2 million due to forwarding and transportation charges incurred during the year. Other income contracted by 85.49 percent year-on-year in 2020 due to high-base effect as the company wrote back its liabilities in 2020.

Owing to higher distribution charges and lower other income, operating loss magnified by 12.82 percent year-on-year in 2020 to clock in at Rs.20.76 million.

Finance cost declined by 13.51 percent year-on-year in 2020 which included only bank charges as the company was meeting its working capital requirements by acquiring interest free loan from company’s directors. MSCL’s net loss dropped by 10.24 percent year-on-year in 2020 to clock in at Rs. 16.717 million with loss per share of Rs.0.54.

In 2021, MSCL’s topline boasted a massive year-on-year growth of 238.23 percent to clock in at Rs.92.67 million. As the signs of COVID-19 began to subside, the market responded positively. MSCL’s sales mainly grew on the back of vigorous demand from automobile and foaming industry and also because of upward revision in the prices of MSCL products. Pak Rupee depreciation greatly increased the cost of sales; yet, MSCL was able to post gross profit of Rs. 11.504 million after successive years of gross losses.

GP margin clocked in at 12.41 percent in 2021. Administrative and distribution expenses rose by 7.95 percent and 80.3 percent year-on-year respectively in 2021 on the back of higher payroll expenses due to high capacity utilization and also because of hefty forwarding and transportation charges.

After two consecutive years, the company incurred other expense of Rs.7.589 million in 2021 as it sustained bad debts, loss on sale of machinery and also booked provision for obsolete store and spares.

Other income ticked down by 10.29 percent year-on-year in 2021 due to lesser realized gain on short-term investment and lesser profit on TDRs. Operating profit clocked in at Rs.1.128 million in 2021 with OP margin of 1.22 percent. Finance cost further climbed down by 40.63 percent year-on-year due to lesser bank charges. The company reported a positive bottomline of Rs.1.845 million in 2021 with EPS of Rs. 0.06 and NP margin of 2 percent.

The sales growth continued in 2022, however, with a considerably lower degree of 8.7 percent year-on-year. MSCL’s net sales were recorded at Rs.100.734 million in 2022. The sales growth was driven by the demand of spoke wire, MS wire, spring wire, high carbon wire and MS products. However, high cost of sales due to commodity super cycle in the global market coupled with Pak Rupee depreciation culminated into gross loss of Rs.17.65 million in 2022.

Administrative and selling expenses grew by 26.25 percent and 14.48 percent respectively in 2022 due to higher salaries, fee and subscription charges and freight charges incurred during the year.

Other expense drastically grew by 969.76 percent year-on-year as the company booked provision worth Rs. 81.18 million for doubtful debt. Other income performed well and registered growth of 814.31 percent year-on-year to clock in at Rs.26.14 million as director loan of Rs.18.55 million was written back during the year and the company also made scrap sales of Rs.7.3 million in 2022. Due to significantly high other expense, the company posted operating loss of Rs. 79.779 million, the highest among all the years under consideration.

Finance cost also grew by 21percent year-on-year. MSCL posted the highest net loss of Rs.79.88 million in 2022 with loss per share of Rs.2.58.

In 2023, MSCL’s topline slid by 1.52 percent to clock in at Rs.99.203 million. This was due to subdued demand from both automobile and construction sectors on account of ongoing economic and political crisis. Due to sluggish demand, the company’s capacity utilization stood at 6.11 percent in 2023 versus 7.21 percent in 2022.

Cost of sales dropped by 9.81 percent in 2023, yet the company posted gross loss of Rs.7.573 million, down 57 percent year-on-year. Administrative expense multiplied by 34.95 percent in 2023 due to higher payroll expense as well as legal & professional charges incurred during the year. MSCL significantly downsized its workforce to only 9 employees in 2023 from 27 employees in the previous year.

Distribution expense nosedived by 1.43 percent in 2023 due to lower forwarding and transportation charges amid thin demand. Other expense dropped by 86.83 percent in 2023 due to lesser provisioning done for doubtful debts. Other income also slumped by 46.12 percent in 2023 due to high-base effect as the company wrote off directors’ loan in 2022 and also because of scrap sales made in 2022.

Operating loss contracted by 82.96 percent to clock in at Rs.13.594 million in 2023. Finance cost surged by 278.26 percent in 2023 on account of higher bank charges & commission and also because of LC charges incurred during the year. MSCL posted net loss of Rs.13 million in 2023, down 83.73 percent year-on-year. Loss per share stood at Rs.0.42 in 2023.

In 2024, MSCL’s topline grew by 23.46 percent year-on-year to clock in at Rs.122.475 million. During the year, the company didn’t produce any mild steel wires due to sluggish demand in the market on account of political and economic instability.

Conversely, the production of high carbon steel wires grew by 11.84 percent to clock in at 425 tons which is still very low when compared to the rated capacity of 5000 tons. Pak Rupee depreciation, elevated energy cost and escalated raw material prices resulted in 30.82 percent higher cost of sales in 2024. Low demand in the market and idle plant capacity didn’t allow MSCL to pass on the impact of cost hike to its consumers.

This resulted in 127.29 percent higher gross loss to the tune of Rs. 17.213 million incurred during the year. Administrative expense escalated by 14.86 percent in 2024 due to inflationary pressure. Distribution expense surged by 50.85 percent in 2024 due to higher forwarding and transportation charges incurred during the year. Other income shrank by 67.29 percent in 2024 due to high-base effect as the company wrote back liabilities in 2023.

Operating loss mounted by 73.33 percent to clock in at Rs.23.56 million in 2024. Finance cost dwindled by 26.44 percent in 2024 due to lower bank commission and charges paid during the year. Net loss multiplied by 79.55 percent to clock in at Rs. 23.34 million in 2024. This translated into loss per share of Rs.0.75 in 2024.

Recent Performance (9MFY25)

During the nine months of the ongoing fiscal year, MSCL recorded 13.32 percent year-on-year decline in its topline which was recorded at Rs.74.28 million. This was on account of sluggish demand. Cost of sales dwindled by 28.25 percent due to stability in the value of local currency and decline in international steel prices due to lackluster demand from key economies like China and India. This resulted in 67.28 percent plunge recorded in the gross loss of the company which clocked in at Rs.10.73 million in 9MFY25.

Administrative expense mounted by 63.73 percent in 9MFY25 mainly on account of higher payroll expense as well as legal & professional charges incurred during the period. Other income eroded by 36.39 percent in 9MFY25 probably due to lower markup income on account of monetary easing. Operating loss tapered off by 44.95 percent to clock in at Rs.20.34 million in 9MFY25. Finance cost ticked up by 4.76 percent in 9MFY25 due to higher bank charges incurred during the period.

MSCL recorded 43.19 percent thinner net profit to the tune of Rs.20.08 million in 9MFY25. This translated into loss per share of Rs.0.00648 in 9MFY25 versus loss per share of Rs.0.01141 recorded in 9MFY24.

Future Outlook

Gradual economic recovery witnessed in the recent months coupled with the rebound of local automobile, white goods and construction industries will provide impetus to improved demand of steel. The performance of local steel sector will also be buttressed by a dip in the rebar prices due to stable exchange rate and low international demand.

Comments

Comments are closed for this article.