Cost of falling cotton production

Is the cost of falling cotton production restricted to bleeding dollars for raw material import? Critics often argue that loss in domestic cotton output is no excuse for struggling textile exports. This is considering that countries with little to no indigenous crop of their own – such as Bangladesh – have grown textile-based exports over 5 times during last 20 years.

Consider also that Bangladesh spends over thirty percent of its textile dollar earnings on importing raw material such as fibre, filament, and yarn, yet ballooning raw material bill has done little to limit its value-adding potential. Back home, textile continues to rely on low value-adding yarn and cloth to provide one-fourth of sectoral exports, especially in face of onslaught from southeast Asian exporters in apparel and RMG category during the last decade.

Does that mean Pakistan should stop worrying about falling cotton output – which according to BR Research estimate has fallen to its 26-year worst in the ongoing season? The accompanying three illustrations may help explain the creeping impact of declining cotton output downstream, particularly on the spinning segment.

Since reaching its peak volume in FY05, domestic cotton output has fallen by over two-fifths. Yet, because demand from textile has remained sticky – cloth production has stayed over 1 billion meters for most of past decade – the gap is met by importing raw material from international market. This is further confirmed from various governmental and private sector estimates that place annual domestic cotton demand between 15 to 16 million bales (or 2.7 million tons).

This is substantive – even more so because unlike popularly held notions, a shortfall in cotton has not exactly pushed spinners to man-made fibre. That’s because spinning is a demand-driven business; and for so long as buyer preference in value-add knitwear and RMG category remains tilted in favour of cotton-based fabric, spinners have little choice but to fill the gap by using imported fibre, rather than switching over to synthetic or blended.

The overarching risk to this equation, however, remains supply shock to worldwide cotton supply; that is, if cotton price in international market were to run amok due to global deficit. Domestic value adding segment may struggle to pass on the price impact, whereas lower value-add factor may mean that the RMG segment may earn lower bang for its buck due to lack of competitiveness.

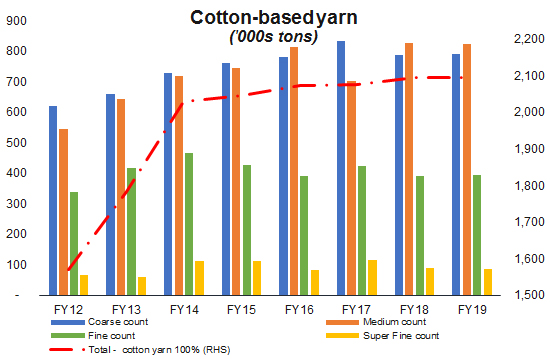

But here is a baffling fact: between FY12 and FY19, while man-made fibre production has remained flat-lined (in fact, declining by CAGR 0.6 percent), cotton-based filament has maintained a positive geometric growth of four percent per annum. That may sound like a win for domestic spinners, except when one recalls that total volume of cloth production has been on a flatline, as have the value-added exports of RMG and apparel. Where then, is increasing cotton-based yarn being consumed, if not towards cloth production?

To answer that mystery, look towards the breakdown of cotton-based yarn output. Turns out, during the intervening years the country has been producing a lot more coarse and medium count yarn – forty percent more, to be exact. In contrast, fine count yarn peaked in FY14, and has since been on a steady decline of CAGR 3 percent, as has super-fine count yarn which has been falling by 5 percent annually. Thus, even if surplus yarn production is adding towards exports, the incremental gain is to lower value-add coarse and medium counts.

It was for textile sector researchers to develop models to extrapolate the impact of increasing share of lower count yarn on value-added export potential of the country. But if intuition – coupled with export figures of past five years – is any guide, the correlation does not exactly appear positive.

Comments

Comments are closed for this article.