Interloop (PSX: ILP) commenced operations in 1992 as a private limited company and subsequently it was converted into public limited company on 18th July, 2008. The company through an Initial public offering (free float of 12.5 percent) was later listed on Pakistan Stock Exchange on 5th April, 2019.

ILP is a vertically integrated hosiery manufacturer primarily involved in the manufacturing of socks and tights. The company is also involved in the production of yarn (approximately 40 percent of which is consumed internally), as well as yarn dyeing services. In recent light, the company has ventured into the denim business, which is expected to yield about 40,000 jeans per day. Client portfolio of the company includes multinational companies such as Nike, Adidas, H&M and Levis to name a few. ILP generates bulk of its revenue through exports, which constituted about 90 percent of total sales during FY19. The customer base is mainly concentrated in Europe and America.

At inception the company consisted of 10 knitting machines which as of now have turned to 5,000 knitting machines. The company currently owns 4 hosiery production facilities in Pakistan and 1 in Bangladesh through its associate IL Bangla Limited. The sheer size of the company can be gauged from its massive revenue stream which clocked in above Rs.30 billion during the period under review. The company also provides employment to over 17,000 people.

IL Apparel (Private) Limited is a wholly owned subsidiary of the Company which entails knitwear and active-wear business of the company. It commenced operations in January of 2019, while its knitwear pilot project at Faisalabad exported the first shipment in March 2019.

Current financial performance

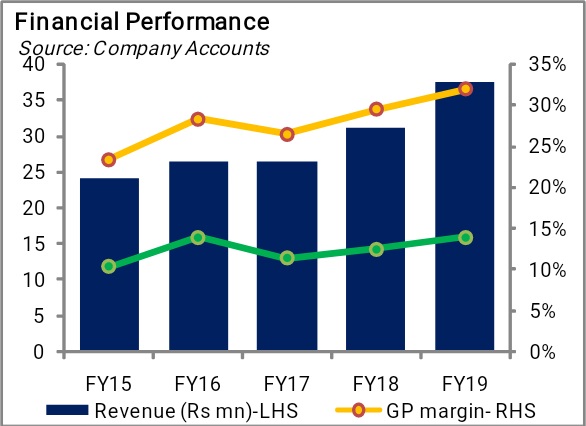

The company witnessed a 20 percent growth in top line for the year ended June 30, 2019, recording revenue at Rs.37.7 billion-highest to date. It managed to achieve the record revenues on the back of higher exports, which increased 23 percent year on year and accounted for 90 percent of total sales during the year. Despite facing a lower per unit price on exports, higher volumetric sales kept the revenues on positive trajectory. Currency witnessed a devaluation of about 20 percent during this period that contributed Rs2.2 billion currency exchange gain on the books of the company.

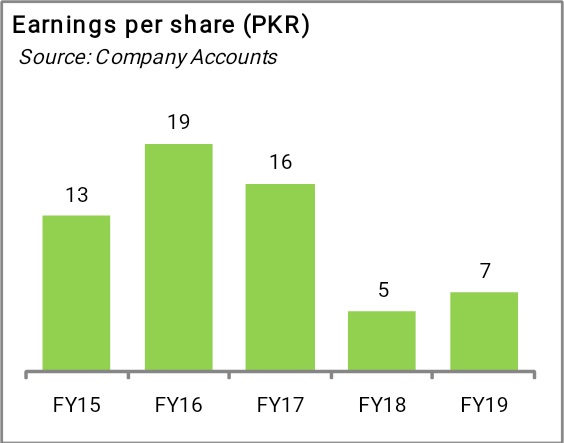

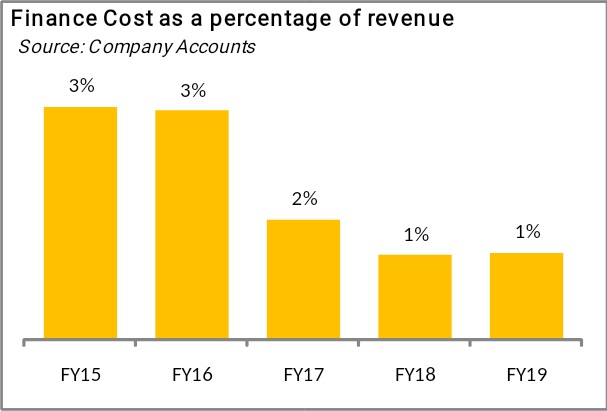

Gross Margins during the year clocked in at 32 percent, as compared to the corresponding period where margins were recorded at 29 percent. The increase is largely driven by efficient operations, and favourable exchange rate as mentioned in the company accounts. Interest rates during FY19 climbed up to 12.25 percent as opposed to 7.50 percent seen in July, 2018. The increase in debt servicing coupled with a higher effective tax rate of 4 percent (SPLY 3 percent) were not enough to drag the net profit margins down, which were recorded at 13.86 percent as opposed to 12.86 percent in the preceding year.

The company in its annual statement highlights the challenges it faced during the year entailing pressures on export selling prices, shortage of gas, and increase in minimum wages, lack of timely sales and tax refunds by Government etc.

Past performance

The revenue stream during the past five years has seen exponential growth. The CAGR for the period FY14-19 is calculated at 11 percent. The company was able to setup a spinning unit and a production facility for socks and tights in Faisalabad during the preceding 5-year period. A15.4 MW Interloop Power Plant based on Tri-Fuel Engines was also setup in Faisalabad to cater to energy requirements of existing facilities and new extensions. In FY18, it commissioned its hosiery plant while it established wholly owned subsidiary IL Apparel (Private) Limited. FY18 marked the company's demerger from non-business of Dairy, IT, Real Estate and Investments in Mutual Funds into a separate holding Company owned by Voting shareholders of Interloop.

Gross Margins during this period averaged about 28 percent, which is significantly higher compared to the giants of the industry. Finance costs as a percentage of sales have remained within a range of 1-4 percent in the past 5 years. As a result, stable net profit margins are seen during this time averaging about 12 percent. Liquidity position for the company as reflected in the past 5 years has remained largely stable and above 1.0x, except for FY18 where it dipped down to 0.8x, it reverted to 1.27x as of June 30, 2019. The company has remained highly leveraged during the 5-year period as reflected by its debt to equity ratio that averaged 1.2x. This however has not been an area of concern, one reason is that the industry dynamics support such a capital structure and is justified by the high setup costs. More importantly, the interest coverage ratios during the 5-year period are suggestive of sufficient coverage for its debt servicing, averaging at 10x for the preceding 5-year period.

Pattern of shareholding

Shareholding pattern of the company is concentrated mainly with the Directors, CEOs and their spouses holding about 82 percent of the company. This is followed by Banks, DFI, NBFC and insurance companies having 6 percent stake in company. Individuals constitute mostly domestic investors having a shareholding of 5 percent in the company. The company in its IPO made a free float of 12.5 percent.

Industry dynamics

The textile sector is of utmost importance to the economy as reflected by the scale at which it operates. To get some perspective on this, textile exports account for more than 50 percent of the total exports. As per the Pakistan economic survey FY 2016-17 the value added sector contributed one-fourth of industrial value added products and provided employment to about 40% industrial labor force.

The dynamics of the industry entail a value chain that is interconnected. At the base of it lies cotton which serves as the basic raw material. The process begins with the ginning process which requires separating cotton fiber from the seed. This is where spinning plays its role to turn the fiber into yarn which then moves over to weaving that turns it into fabric, Ready for dyeing, after which it goes to retail. The major exports by the industry are largely concentrated with downstream categories such as knit wear, bed wear and ready-made garments.

Currently, textile faces a rough business environment due to increased inflationary pressures, rising finance costs, sales refund delays and lowers per unit export prices. 20 percent devaluation in rupee during FY 19 resulted in higher costs for the imported input materials. On the domestic front, the incumbent government has rescinded the zero rated facility with the imposition of 17 percent sales tax. Debt servicing has become expensive for the companies as nominal interest rates have touched 13.25 percent. Industry sources say that the government in the form of refund has foot the bill with bonds.

Future outlook

The company will be subject to both external and internal pressures in the coming times. As the global landscape becomes more and more saturated the company aims at tackling the situation through efficiency improvements and interventions in supply chain, resultantly reducing lead times. The expansion into apparel and denim is likely to bear fruit in the coming times. The company may further face headwinds as the cost of doing business may impede the smooth functioning of the business.

Comments

Comments are closed for this article.