Fauji Cement Company Limited (PSX: FCCL) is operating in the north zone of the cement industry, supplying cement to domestic markets in the north as well as exporting markets including Sri Lanka, India, Afghanistan, South Africa, and the MENA region. The company operates two cement lines located in the Jhang Bahtar district of Attock. It started operations in 1997 with a capacity of over 3000 tons per day subsequently enhancing it in 2005 to 3,885 tons per day, which is approximately 1.2 million tons. Another production line was added in 2011 and through a series of capacity expansions; the company raised this capacity to 3.27 million each year with major equipment supplies from leading Germany and Swiss companies.

The company also installed a refuse derived fuel processing plant in 2009 and set up 12 MW of waste heat recovery unit (WHR) that started to produce electricity in 2015 utilising waste. This is a common practice amongst cement manufacturers and is meant to ease the pressure on grid based electricity. Together the captive power based on gas and dual fuels is 22MW.

In 2016, the company had an accident on site that destroyed the raw meal cement silo for line-II and the coal mill it collapsed on. The company had to rehabilitate its plant and decided to enhance the capacity of the line from 7200 tons to 7600 tons per day (or from 2.16 million tons to 2.28 million tons annually). The new line came back online in Oct-17. Together with that, a 9 MW WHR and a 12.5 MW of captive solar power are being introduced to be commissioned by mid-2019.

The company is owned by the Fauji group with 36 percent of the shares by the Committee of Admin Fauji Foundation while another 13 percent are held by other associate companies in the group including Fauji Fertilizer and Fauji foundation. More than 30 percent of the shares are held by the general public while the rest are distributed amidst modarabas, mutual funds, joint stock companies, banks, DFIs and foreign companies.

Operational and financial performance

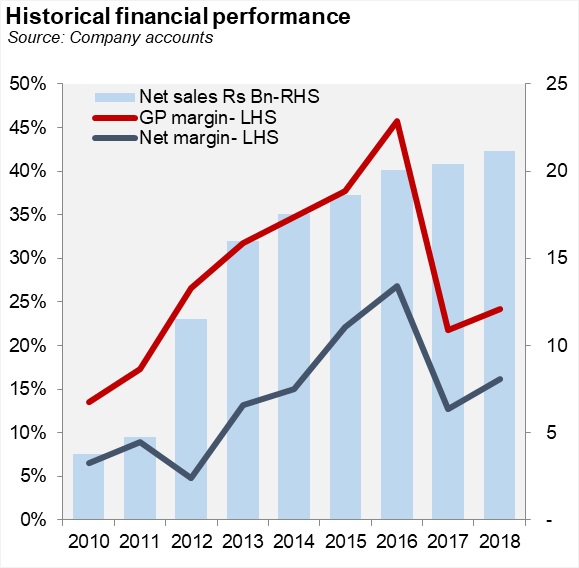

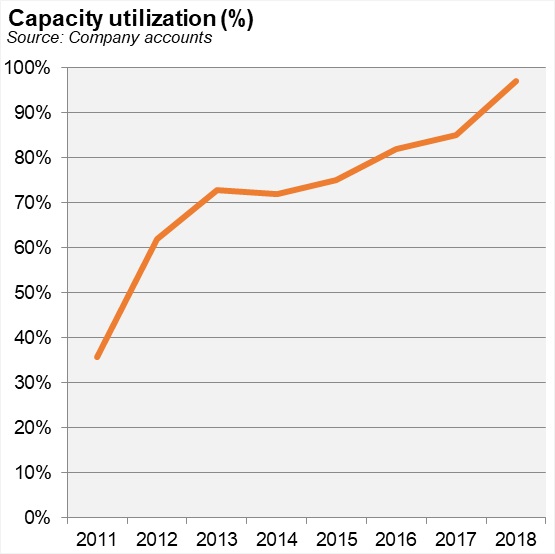

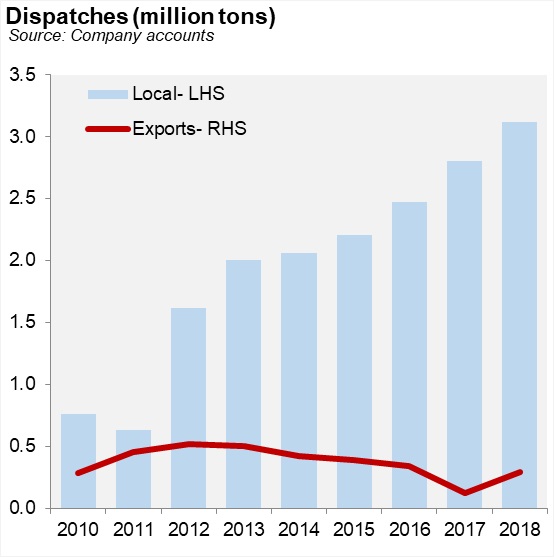

Fauji is one of the bigger cement manufacturers with a market share of 8 percent based on capacity in 2017-however, which should have fallen to 6 percent since new expansions have come in. In terms of dispatches, in the outgoing FY18, Fauji grabbed a 7 percent market share. The company has also had improving levels of capacity utilisation which speaks for growing efficiency of its plant and its strong market presence. It grew from 36 percent in FY11 to 75 percent in FY15, 85 percent in FY17 and 97 percent in FY18. Soon after the accident, the company opted to buy clinker from nearby locations to keep its utilisation levels and market share on the same level as before, though at a big hit to their margins.

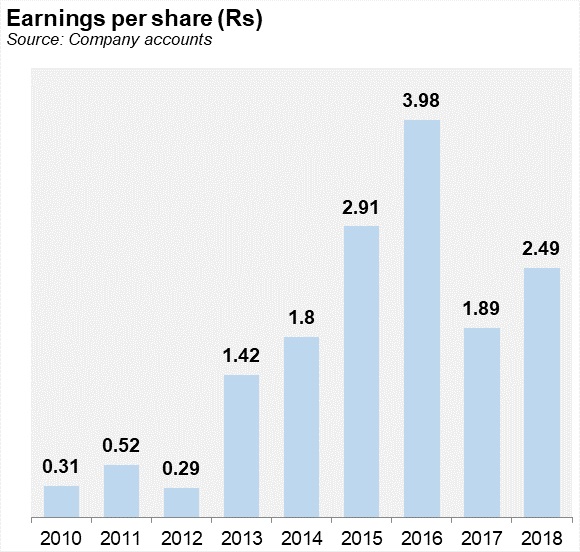

The company's accident did however come at a rather in opportune time. The FY17 saw massive demand coming from domestic market particularly driven by mega infrastructure projects and development expenditure doled out by government. Simultaneously, economy expansion led to greater activity in the construction and housing sector as well. Though Fauji was able to grow its sales, the higher cost of clinker purchase led the company to lose majorly on the bottom line. Margins dropped to 22 percent in FY17 from 46 percent in FY18. Clinker purchase costs during FY17 were about 53 percent of cost of goods sold.

Once the plant was rehabilitated though, the golden period for the cement sector was nearly over. Higher competitive pricing in the north due to greater capacity led to retention prices dropping while costs of coal and other fuels were also headed up. At a time when the company was producing at maximum capacity utilisation, margins could only improve to 24 percent in FY18 but that too because it was producing clinker again. The rest of the industry started to see their margins drop.

During the outgoing year, aside from the 12000 tons of capacity enhancement, the company also upgraded its yard clinker feeding system at line-I to increase plant reliability, replaced the old premising bin with a new one at raw mill-I, installed a waste clink hopper to handle the waste clinker moving out of the system, upgraded the cooler system, brought a new bucket elevator at silo-I for material transportation, added cement packing capacity in line-II and improved its coal stacking system. This will no doubt improve the efficiency of the plants while the new WHR and captive facilities will further bring down production costs.

Recent operations and future outlook

The silver lining for Fauji is that despite the accident, it has retained its market share in the north at 6-7 percent. It kept buying clinker till October when the new silo came into operation at plant-II. In 1HFY19, the company saw its revenue grow by only 2 percent, but everything else shows drastic improvement. The company is no longer buying clinker so cost of goods came down by 8 percent during the first half of the current fiscal. This has allowed margins to grow to 29 percent from 22 percent during this time last year.

All other costs despite higher exports have remained stable which led to a growth in the bottom line by 43 percent. This year would level Fauji with the rest of the industry after its 2-year blip as the plants become fully operational. The captive power based on solar energy is particularly inspiring and could set itself up as an example for successful application of renewable energy into captive power. For an industry that has gone in the direction of coal based power plants, the success of this project could turn motivate others to follow suit.

Afghanistan and India are becoming tougher markets for Pakistani cement-particularly taking into account the political tensions that Pakistan maintains with both. This will hurt cement players in the north especially at a time when local domestic market is experiencing a slump. Moreover, coal prices, the depreciation of the rupee have already wreaked havoc to costs and further movement upwards will adversely impact cement manufacturers. Even if they pass on the costs to the consumers, the demand is simply not there, and may even get displaced by imported cement if the prices are not managed. From here on out, Fauji is the in the same boat as other players located in the north and hasn't seen the end of its tough times.

======================================================== Pattern of Shareholding (as on June 30, 2018) ======================================================== Categories of Shareholders Share ======================================================== Directors and their spouse(s) and minor children 0.05% Associated Companies 48.9% Committee of Admin Fauji Foundation 35.87% Fauji Foundation 3.53% Fauji Fertilizer Bin Qasim 1.36% Fauji Oil terminal 1.36% Fauji Fertilizer 6.79% Modarabas 0.02% Mutual Funds 1.81% Insurance Companies 1.28% Investment Companies 0.27% Joint Stock Companies 6.67% Foreign Companies 4.21% Pension Funds 0.24% Others 0.92% Banks, development finance institutions, 4.30% non-banking finance companies etc. General Public 31.32% Total 100% ========================================================

Source: Company accounts

========================================================= Fauji Cement- 1HFY19 ========================================================= Rs (mn) 1HFY19 1HFY18 YoY ========================================================= Sales 10,431.14 10,268.49 1.6% Cost of Sales 7,383.31 8,040.36 -8.2% Gross Profit 3,047.84 2,228.13 36.8% Distribution costs 120.72 119.99 0.6% Administrative 192.39 174.40 10.3% Other operating expenses 189.76 137.40 38.1% Other income 83.33 35.15 137.1% Finance cost 53.38 73.94 -27.8% Profit before tax 2,574.91 1,757.55 46.5% Taxation 751.12 489.76 53.4% Net profit for the period 1,823.80 1,267.80 43.9% Earnings per share (Rs) 1.32 0.92 43.5% GP margin 29% 22% 34.7% NP margin 17% 12% 41.6% =========================================================

Source:PSX notice

Comments

Comments are closed for this article.