Soon after the General Elections 2018, the rupee recovered against the US dollar. Some enthusiasts called it the ‘Naya Pakistan’ effect, alluding to the confluence of factors that helped PKR climb back up against the USD.

These factors included the bringing back of dollars by dollar-hoarders who felt that the PTI’s economic team might soon grab the bull by its horns to solve the external account crisis leaving little room for further currency depreciation.

Since then, a host of good news has been making rounds that should at least soften, if not ease, immediate balance-of-payments (BoP) concerns: funding from China, funding from Islamic Development Bank, and the potential raising of money from diaspora bonds. Rupee’s recovery is a manifestation of that. But the stock market remains bearish to neutral.

Some argue that the equities bazaar is nervous because of external account concerns. But if external accounts really mattered this much, why did the benchmark index of Pakistan Stock Exchange had risen quite sharply during the 2013 transition from PPP to PML-N? Those days weren’t rosy for external accounts either; the BoP – and recourse to the IMF – was on PML-N’s top agenda back then. And similar is the situation today.

Granted that this time around, Uncle Sam is tough-talking Pakistan, which is why the IMF may give a tough time, if and when the negotiations begin. But surely, no one is expecting Pakistan to default; there is a sense of confidence that things will be under control, a reliable signal of which is PKR-USD’s stable movement of late in the interbank market.

Does this signal the equities players’ lack confidence on the PTI’s ability? Without pretending to know what lies in their hearts, one would imagine that the business sector has at least as much confidence on the PTI as it had in the PML-N, at least it in its early years.

The PTI’s would-be finance minister has a business background; his speech on economic affairs was well-received even by critics; and some top business names – such as Abdul Razak Dawood, and other professionals – are touted to form a technocratic-like setup. On paper, these developments should give confidence to the market. Yet, the KSE-100 remains mum.

What does the market exactly want? A few months ago, there were some who feared the elections would be delayed, if not scrapped altogether; then there were some who feared a hung parliament, followed by fears of nation-wide protests on alleged rigging – all leading to economic indecision and delays. But none of these fears have materialised. The negative news has bottomed out; be it weak banking results or weak FX reserves, none of this is new.Despite this, when the MNAs took oath this Monday, the KSE-100 index fell further instead of taking heart from a smooth transition of power.

The outflow of foreign portfolio investments is indeed hurting investor sentiments. And the same can be expected to continue as the gradual strengthening of the USD may nudge investors to pull money out of emerging markets. But that is not a valid explanation for weakness at the bourse, which has previously ignored and absorbed FIPI outflows on many occasions. FY17 is one recent such example, when the KSE-100 grew about 23 percent and foreign investors pulled out north of $500 million from the market.

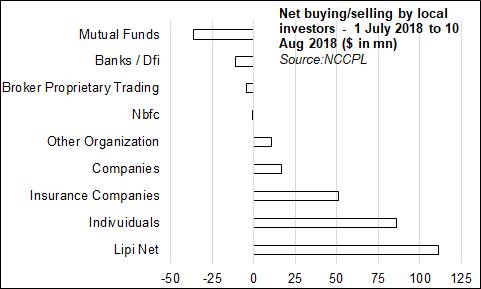

Unless all of the above reasoning is flawed, there could be two reasons why the KSE-100 isn’t taking off: The market (especially asset management companies) is really scared of the external account situation, and Uncle Sam’s rap on the knuckles. Or they are all waiting for a leader – an institution or two that can lead the herd to greener pastures. Regardless, one can’t help but notice that the smart money – from high-net-worth-individuals and insurance companies – have been accumulating while the rest mostly sell or remain timid buyers.

Comments

Comments are closed for this article.