Merit Packaging Limited (PSX: MERIT) was incorporated in Pakistan as a public limited company in 1980. The principal activity of the company is the manufacturing and sale of printing and packaging material.

The company caters to a wide range of sectors including food & beverages, surgical instruments, consumer goods, textile etc. The company belongs to The Lakson Group of companies.

Pattern of Shareholding

As of June 30, 2025, MERIT has a total of 199.96 million shares outstanding which are held by 2114 shareholders. Associated companies, undertaking and related parties have the largest stake of 81.54 percent in the company followed by local general public holding 14.18 percent shares. NIT & ICP have 2.30 percent stake in MERIT.

The remaining ownership is distributed among other categories of shareholders.

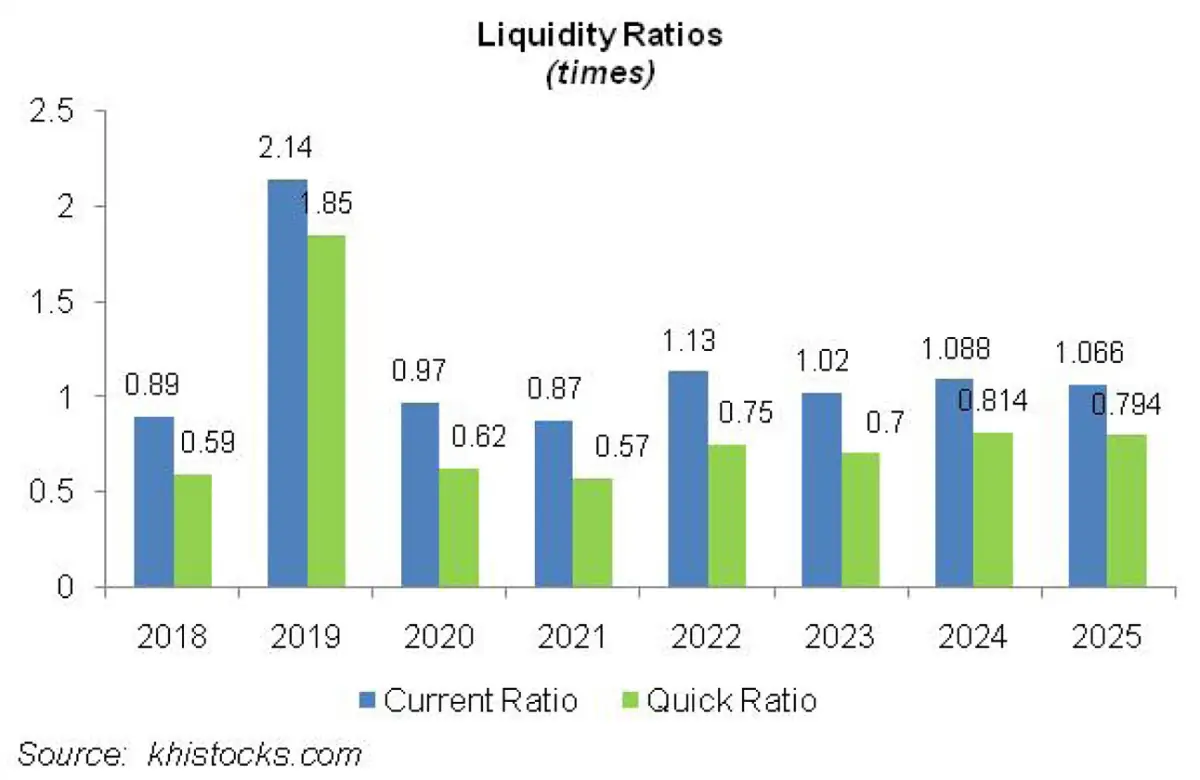

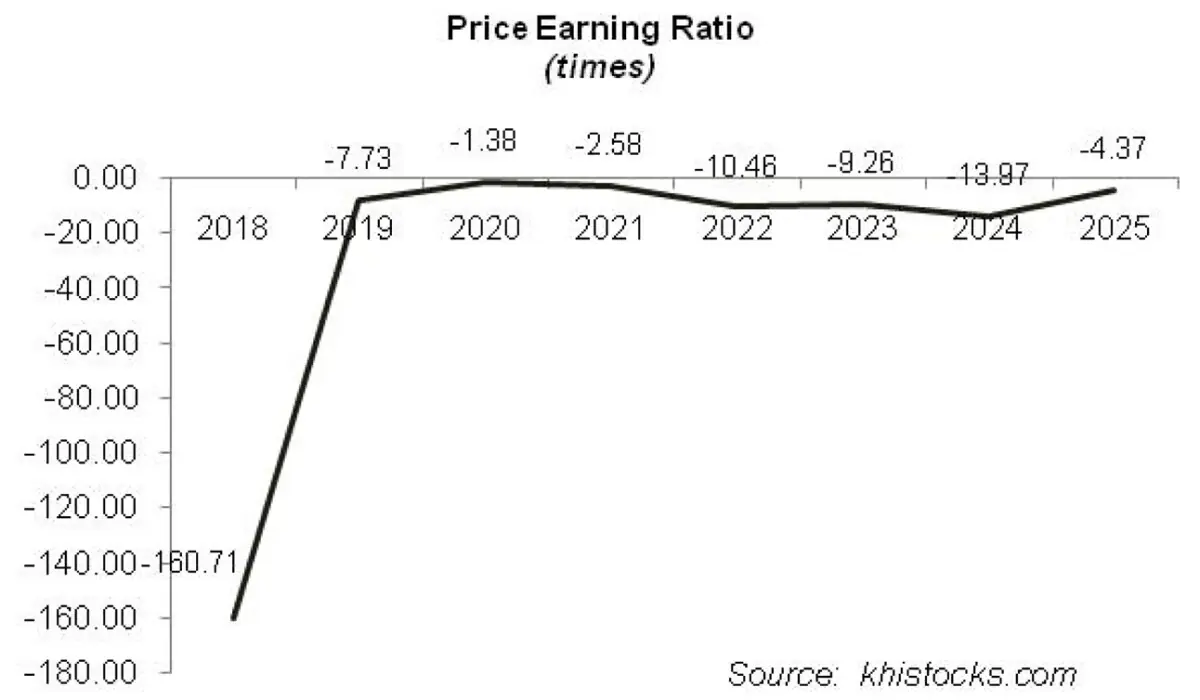

Financial Performance (2021-25)

Barring year-on-year decline in 2025, MERIT’s topline rode an upward trajectory over the period under consideration. However, the company never posted net profit during this period.

The company’s gross margin dived into negative zone in 2020 and 2021 and then recovered thereafter only to post a negative value again in 2025. Its operating margin which stayed in the negative territory until 2021 rebounded thereafter only to fall back in 2025. The detailed performance review of the period under consideration is given below.

After a dip in 2020, MERIT’s topline resumed its uphill journey in 2021 with 34.48 percent year-on-year rise to clock in at Rs.2902.559 million in 2021. As economic activities began to recommence after the lockdown period, MERIT started receiving new orders resulting in a healthier topline.

However, topline growth couldn’t trickle down to produce a healthier bottomline amid high cost of raw materials, Pak Rupee depreciation, hike in energy prices and lesser productivity and efficiency of company’s old printing machines. While MERIT couldn’t register gross profit in 2021, it was able to significantly curtail its gross loss by 78.63 percent year-on-year in 2021 which clocked in at Rs.42.40 million.

Administrative expense ticked down by 2.93 percent year-on-year in 2021 as the company trimmed down its workforce from 264 employees in 2020 to 206 employees in 2021. Conversely, distribution expense spiked by 14.54 percent on account of higher outward carriage charges incurred due to recovery of sales volume.

Other income greatly propelled the operating performance of MERIT in 2021 as it grew by 387.30 percent on the back of insurance claim, capital grant income, exchange gain, impairment reversal and scrap sales.

The company’s operating loss narrowed down by 47.71 percent year-on-year in 2021 to clock in at Rs.217.75 million. Lower discount rate helped MERIT cut down its finance cost by 7.38 percent in 2021. This translated into 18.44 percent lower net loss to the tune of Rs.564.98 million in 2021. Loss per share also plummeted to Rs.6.84 in 2021 from Rs.8.59 in 2020.

In 2022, MERIT witnessed 44.1 percent year-on-year rise in its net sales which clocked in at Rs. 4181,647 million. This was backed by both upward price revision and increased sales volume. This enabled the company to register gross profit of Rs.252.92 million in 2022 after two sustained years of gross loss.

GP margin clocked in at 6.05 percent in 2022. Administrative expense surged by 14.78 percent year-on-year in 2022 due to higher payroll expense on account of inflationary pressure despite drop in number of employees to 188 in 2022.

Higher sales volume and increase prices of POL products also drove up the distribution expense by 44.21 percent in 2022. MERIT posted operating profit of Rs.92.77 million in 2022 with OP margin of 2.22 percent. The company was able to record positive operating result in 2022 after three unrelenting years of operating loss.

Despite hiking discount rate, the company was able to reduce its finance cost by 19.51 percent year-on-year in 2022 due to lesser external borrowings obtained during the year. The company registered net loss of Rs.168.17 million, down 70.23 percent year-on-year. Loss per share also dropped to Rs.0.84 in 2022.

The company registered topline growth of 51.63 percent in 2023. Net sales clocked in at Rs. 6340.624 million in 2023. Besides higher sales volume, the company was able to pass on the impact of cost hike to its customers in 2023 which improved its margins.

Moreover, the company has also been undertaking massive CAPEX for the installation of new plant & machinery to increase its productivity and cut down its cost. This resulted in 94.37 percent rise in gross profit with GP margin jumping up to 7.75 percent in 2023.

Administrative expense escalated by 9.98 percent year-on-year in 2023 due to higher payroll expense as number of employees grew to 194 in 2023. Distribution expense hiked by 22.49 percent in 2023 on the back of higher sales volume which pushed up the freight charges.

Other income strengthened by 63.29 percent in 2023 on account of hefty scrap sales made during the year. However, its impact was nullified by 389.29 percent surge in other expense in 2023 which was the result of enormous provisioning done for ECL.

Operating profit magnified by 200.47 percent in 2023 with OP margin climbing up to 4.40 percent. Finance cost surged by 30.82 percent year-on-year in 2023 due to unparalleled level of discount rate, This was despite the fact that the company paid two long-term loans in 2023.

Net loss of Rs.189.91 million posted by MERIT in 2023 was 12.93 percent higher than that of 2022. Loss per share also surged to Rs.0.95 in 2023.

MERIT’s topline inched up by 4.70 percent to clock in at Rs.6638.477 million in 2024. During the year, the company also received an export order worth Rs. Higher cost of sales resulted in 6.81 percent decline in gross profit in 2024 with GP margin falling down to 6.90 percent.

Administrative expense surged by 36.36 percent in 2024 due to higher payroll expense on account of inflationary pressure. This was despite the fact that the company streamlined its workforce from 194 employees in 2023 to 181 employees in 2024.

Elevated travelling & conveyance as well as repair & maintenance charges also inflated administrative expense in 2024. Distribution expense also inched up by 10.69 percent during the year due to hefty carriage outward charges incurred during the year.

The transaction of sale and leaseback of land and building with SIZA Services (Private) Limited, an associated company, resulted in gain on sale of fixed assets in 2024 which pushed up other income by 53.37 percent in 2024. Other expense contracted by 69.11 percent in 2024 due to high-base effect as the company recorded massive allowance for ECL in 2023.

MERIT’s operating profit declined by 10.83 percent to clock in at Rs.248.57 million in 2024 with OP margin diving down to 3.74 percent. Finance cost inched up by just 2.16 percent in 2024 due to higher discount rate while the company’s outstanding borrowings significantly shrank during the year.

MERIT’s net loss tumbled by 1.87 percent to clock in at Rs.186.361 million in 2024 with loss per share of Rs.0.93.

In 2025, MERIT recorded 20.45 percent thinner topline to the tune of Rs.5280.933 million. This was the first time after 2020 that the company’s net sales deteriorated year-on-year.

While the export sales significantly increased during the year, local sales receded due to increased competition and reduced demand. During the year, the company entered into an agreement to dispose its flexible packaging unit which also squeezed the sales volume. MERIT’s export sales comprised of sales made to Kenya.

Lower sales volume coupled with constricted margins proved to be a double whammy for MERIT and translated into gross loss of Rs.28.733 million in 2025. This was the first time after 2021 that the company posted gross loss. Administrative expense spiked by 44.24 percent in 2025 primarily due to higher payroll expense and software license and implementation fee incurred during the year. Increased salaries were despite the fact that the company further rationalized its workforce to 170 employees in 2025.

Distribution expense surged by 28.33 percent in 2025 due to increased carriage outward charges incurred on the back of export sales. High-base effect due to gain recognized on the disposal of fixed assets in the previous year pushed down other income by 45.58 percent in 2025.

Lesser legal & professional charges squeezed other expense by 28.44 percent in 2025. MERIT posted operating loss of Rs.350.305 million in 2025. Finance cost lowered by 47.95 percent in 2025 due to monetary easing and repayment of sponsor loan during the year. Net loss mounted by 221.78 percent to clock in at Rs.599.667 million in 2025. This translated into loss per share of Rs.3.00 in 2025.

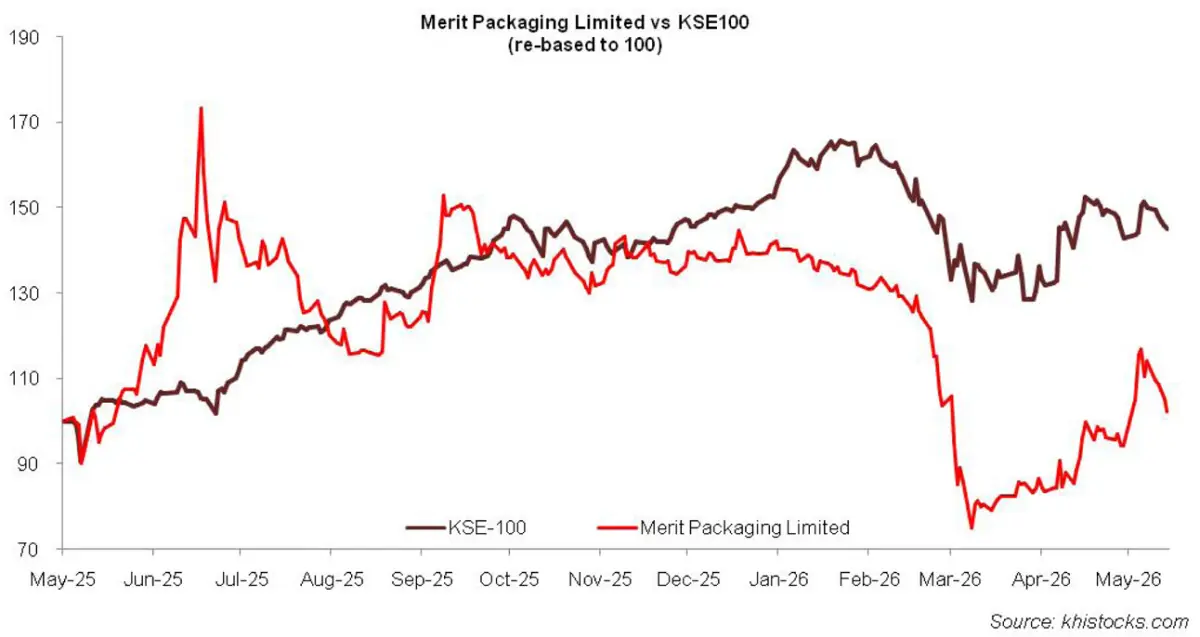

Recent Performance (9MFY26)

During the nine-month period of the ongoing fiscal year, MERIT recorded 43.55 percent decline in its net sales which clocked in at Rs.2537.79 million. This was mainly on the back of disposal of Flexible packaging unit. Decline in sales coupled with consistent cost increase squeezed gross profit by 67 percent in 9MFY26 with GP margin clocking in at 3.17 percent versus GP margin of 5.43 percent recorded in 9MFY25.

Constant workforce rationalization and limited operations post divesture of Flexible packaging unit pushed down administrative expense by 3 percent in 9MFY26. Lower sales volume also compressed distribution expense by 23.89 percent in 9MFY26.

Other income strengthened by 45.19 percent in 9MFY26 due to gain recognized on the disposal of Gravure machinery pertaining to Flexible packaging unit. Other income was greatly offset by 55.87 percent spike in other expense in 9MFY26 likely due to provisioning done for WWF and ECL.

MERIT posted operating loss of Rs.109.31 million in 9MFY26 versus operating profit of Rs.28.42 million posted in 9MFY25. What turned tables for MERIT was gain worth Rs. 505.66 million recognized on the disposal of assets classified as held for sale.

Finance cost also shrank by 44.30 percent in 9MFY26 due to reduced reliance on external financing post liquidity injection by asset sale. This enabled the company to register net profit of Rs.80.55 million in 9MFY26 with EPS of Rs.0.40 versus net loss of Rs.169.548 million and loss per share of Rs.0.85 recorded in 9MFY25.

Future Outlook

Due to consistent losses, the company’s accumulated loss stood at Rs.1435.621 million as of March 30, 2026, down 18.74 percent year-on-year. The company is utilizing the funds received from the sale of its land and buildings to pay off its debt and get rid of a large portion of finance cost as a strategy to push its bottomline into positive zone.

The company is also diligently working to enhance its customer base in order to ensure regular stream of revenues. This is evident in the expansion of its export sales. These strategic moves warranty new chapter of growth and turnaround for MERIT.

Comments