Ibrahim Fibres Limited (PSX: IBFL) was incorporated in Pakistan as a public limited company in 1986.

The company is engaged in the manufacturing and sale of Polyester staple fibre (PSF) and yarn. Ibrahim Holdings (Private) Limited is the parent company of IBFL.

Pattern of Shareholding

As of December 31, 2025, IBFL has a total outstanding share volume of 310.507 million shares outstanding which are held by 2031 shareholders. Ibrahim Holdings (Private) Limited, the parent company of IBFL, holds 91.81 percent of its shares followed by local general public having a stake of 4.29 percent in the company.

Foreign companies account for 3.80 percent shares of IBFL. The remaining shares are held by other categories of shareholders.

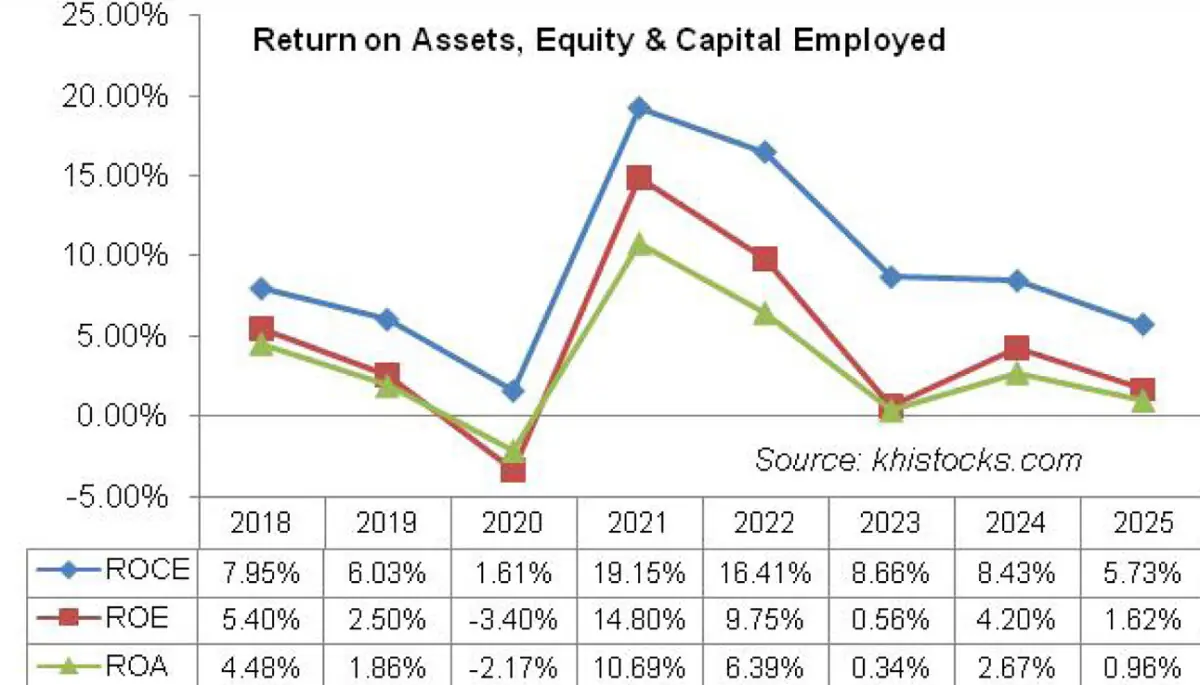

Performance Trajectory (2021-25)

Except for a nosedive in 2025, IBFL’s topline followed an inclining trend over the period under consideration. Conversely, its bottomline posted net loss in 2020. In 2021, IBFL’s bottomline registered staggering rise only to recede in the following two years. In 2024, IBFL’s bottomline posted a phenomenal growth followed by a slump in 2025.

The margins also followed the similar pattern as the bottomline. The detailed performance review of the period under consideration is given below.

IBFL’s topline which dipped by 28.93 in 2020, recovered and posted 49.98 percent rise in its net sales which clocked in at Rs. 70,607.07 million in 2021. This was the result of 27 percent growth in the sales volume of PSF which clocked in at 267,037 MT and 125 percent growth in the sales volume of yarn which clocked in at 70,607 MT in 2021.

High crude oil prices pushed the PSF prices up, resulting in improved margins. Although high raw material prices tried to dilute the gross profit, however, with robust sales volume and upward price revisions, IBFL was able to multiply its gross profit by 538.81 percent in 2021, with GP margin reaching its optimum level of 17.65 percent versus GP margin of 4.1 percent recorded in 2020. Distribution and administrative expense grew by 12.94 percent and 41 percent respectively.

High freight and forwarding and elevated payroll expense were the main culprits behind elevated operating expense in 2021. Other expense multiplied by 2112.78 percent in 2021 due to higher provisioning booked for WWF and WPPF.

Other income also grew by 173.75 percent during 2021 on account of higher scrap sales and gain on disposal of property, plant and equipment during the year.

Operating profit grew by 1189.84 percent in 2021 with OP margin jumping up to 14.75 percent from 1.71 percent in 2020. Finance cost slid by 42.19 percent year-on-year in 2021 which was the result of low discount rate and significantly lower borrowings as the company was able to improve its liquidity to a great extent in 2021.

IBFL was able to post net profit of Rs.6,578.95 million in 2021 with NP margin of 9.32 percent and EPS of Rs.21.19. This was against the net loss of Rs. Rs.1295.48 million and loss per share of Rs.4.17 recorded in 2020.

(In 2022, IBFL, in compliance with the regulations of SECP, changed its financial year from July-June to January-December.

Comparing the year-ended June 30, 2021 to year-ended December 31, 2022 is paradoxical as the period of Jan-Jun, 2022 is included in the annual reports of both 2021 and 2022. To ignore this overlapping, the analysis of 2022 is presented on an irrelative basis)

In 2022, IBFL’s topline was recorded at Rs.115,581 million. During the year, the company sold 285,540 MT of PSF and 53,511 MT of yarn. The year proved to be a challenging one due to deteriorating macroeconomic and political scenario and devastating floods in the country.

Commodity super cycle in the global market owing to Russia-Ukraine crisis coupled with steep deprecation of Pak Rupee and high indigenous inflation pushed up cost of sales and resulted in GP margin of 11.68 percent in 2022.

Higher freight and forwarding charges due to surging fuel cost and increased sales volume played an important role in suppressing the operating profit during the year.

Administrative expense also spiked on the back of higher payroll expense on account of inflation. The OP margin turned out to be 9.16 percent in 2022. Higher finance cost on account of excessive monetary tightening and elevated borrowings culminated into net profit of Rs.5310,545 million in 2022 with NP margin of 4.6 percent and EPS of Rs.17.10.

In 2023, IBFL’s net sales posted a paltry 3.62 percent year-on-year rise to clock in at Rs.119,761.93 million. PSF sales dropped by 20 percent year-on-year in 2023 to clock in at 228,940 MT in 2023 and yarn sales posted 4 percent year-on-year uptick to clock in at 55,813 MT.

While high inflation had already squeezed the demand in the local market, incentives given by the GoP to the PSF importers further harmed the local PSF manufacturers.

High raw material and conversion cost due to elevated prices of raw materials, Pak Rupee depreciation and high energy tariff resulted in 33.58 percent lower gross profit recorded by IBFL in 2023. GP margin fell to 7.49 percent in 2023. Selling & distribution expense registered 26.9 percent year-on-year surge in 2023 due to high freight & forwarding charges.

Administrative expense multiplied by 12.81 percent in 2023 primarily on account of higher payroll expense on account of inflation. IBFL streamlined its workforce from 3490 employees in 2022 to 3203 employees in 2023. Considerably lower provisioning for WWF and WPPF resulted in 60 percent lower other expense incurred by the company in 2023.

Other income also slid by 76 percent in 2023 because of high-base effect as the company recorded dividend income, gain on sale of fixed assets and gain on redemption of short-term investments in the previous year.

Operating profit declined by 44.98 percent in 2023 with OP margin of 4.86 percent. Finance cost escalated by 215.42 percent in 2023 due to high discount rate and increased borrowings. Net profit dwindled by 94.28 percent to clock in at Rs.303.53 million in 2023 with EPS of Rs.0.98 and NP margin of 0.25 percent.

In 2024, IBFL posted an uptick of 0.76 percent in its topline which was recorded at Rs.120,667.93 million. Sales volume of PSF dipped by 6 percent to clock in at 214,334 M tons while sales volume of yarn nosedived by 2 percent to clock in at 54,898 M tons in 2024.

Export sales also eroded by 92.27 percent to clock in at Rs.31.66 million in 2024. This was due to regional conflicts and the ongoing recession in the major export destinations of the company. While local sales volume also dipped, an uptick in the prices resulted in topline growth.

Cost optimization measures such as plant modernization and diversification of energy sources resulted in 8.65 percent year-on-year improvement in gross profit in 2024 with GP margin inching up to 8 percent. Inflationary pressure resulted in 6.53 percent and 13 percent spike in distribution expense and administrative expense respectively in 2024.

The main culprits were higher salaries & wages, directors’ remuneration, travelling & conveyance as well as repair & maintenance charges incurred during the year. Other expense mounted by 156.16 percent in 2024 mainly on account of balances written off during the year.

Other income diminished by 56.71 percent in 2024 due to lower scrap sales, no balances written back and no exchange gain recognized during the year. Operating profit ticked down by 1 percent in 2024, however, OP margin largely remained intact at 4.8 percent.

Finance cost plummeted by 13.34 percent in 2024 due to monetary easing as well as lower outstanding borrowings. After accounting for deferred tax, provision for taxation contracted by 49.66 percent in 2024. This translated into 677.62 percent year-on-year growth in bottomline which clocked in at Rs.2360,116 million in 2024. This translated into EPS of Rs.7.60 and NP margin of 1.96 percent.

IBFL recorded 13.43 percent year-on-year decline in its net sales which clocked in at Rs.104,457.36 million in 2025. While the sales volume of PSF posted 7 percent uptick during the year, yarn sales dropped by 32 percent. The PSF plant achieved capacity utilization of 65 percent in 2025 by producing 253,435 tons of PSF, up 1.93 percent year-on-year.

Conversely, the textile division recorded capacity utilization of 57 percent in 2025 which translated into production volume of 38,099 tons of different blended yarns, down 33.95 percent year-on-year.

Low capacity utilization of both polyester and textile division was the consequence of dumping of cheaper imported products in the local market.

IBFL’s export sales also nosedived by 44 percent to clock in at Rs.17.706 million in 2025 due to tariff wars among major economies which kept changing the dynamics of the global textile market.

Cost of sales slid by 13 percent in 2025 resulting in 17.52 percent thinner gross profit in 2025. GP margin also fell to 7.69 percent in 2025. Lesser freight & forwarding charges translated into 6.34 percent dip in distribution expense in 2025.

Conversely, administrative expense ticked up by 3 percent in 2025 due to higher payroll expense on account of inflationary pressure. This was despite the fact that IBFL rationalized its workforce from 3117 employees in 2024 to 3107 employees in 2025.

Lesser provisioning done for WWF and WPPF translated into 9.97 percent plunge in other expense in 2025. Other income grew by 33.73 percent in 2025; however, proportionally it was much smaller than other expense. Improved other income was the result of greater scrap sales, exchange gain and gain on disposal of fixed assets which offset the impact of lower profit on bank deposits due to monetary easing.

Operating profit diminished by 28.62 percent with OP margin sliding down to 3.94 percent. Despite increased short-term and long-term borrowings, finance cost plummeted by 29.75 percent in 2025 due to monetary easing.

Gearing ratio clocked in at 26 percent in 2025 versus 19 percent in the previous year. Net profit tapered off by 60.47 percent to clock in at Rs.932.915 million in 2025. This translated into EPS of Rs.3.00 and NP margin of 0.89 percent in 2025.

Recent Performance (1QCY26)

During the first quarter of CY26, IBFL recorded a marginal 4.20 percent year-on-year uptick in its net sales which clocked in at Rs.28,886.71 million. The company recorded production volume of 65,719 tons in 1QCY26, up 3.28 percent year-on-year. This translated into capacity utilization of 67 percent in 1QCY26.

The dumping of cheaper products in the local market didn’t allow the company to pass on the impact of cost hike to its customers. This coupled with increased oil prices due to Middle East crisis and elevated energy tariff in the local market resulted in 57 percent thinner gross profit in 1QCY26 with GP margin clocking in at 4.60 percent versus GP margin of 11.15 percent recorded in 1QCY25. Thinner export sales due to geopolitical tension resulted in 5.11 percent dip in distribution expense in 1QCY26.

Conversely, administrative expense surged by 5.10 percent in 1QCY26 due to inflationary pressure. Lower profit related provisioning appears to be the cause of 97.34 percent decline in other expense in 1QCY26.

Other income also deteriorated by 59.74 percent in 1QCY256 probably due to lower income from bank deposits due to monetary easing. Operating profit dwindled by 71.67 percent in 1QCY26 with OP margin clocking in at 1.72 percent versus OP margin of 6.33 percent recorded in 1QCY25. Finance cost surged by 54.52 percent in 1QCY26.

IBFL posted net loss of Rs.320.19 million in 1QCY26 versus net profit of Rs.1076.26 million recorded in 1QCY25. Loss per share was recorded at Rs.1.03 in 1QCY26 versus EPS of Rs.3.47 posted in 1QCY25.

Future Outlook

Cut-throat competition from imported yarn and PSF may impede the local manufacturers from grabbing a significant portion of market share in the absence of efficient inventory management, cost rationalization and concerted marketing efforts.

The company is undertaking various BMR projects to increase its operational efficiency. These include deploying latest technology for its PSF Plant II in partnership with T.EN Zimmer, Germany.

The company has already completed installation of another yarn manufacturing plant which commenced its commercial operations in the last quarter of 2025. The company has also been increasing its solar power capacity over the years and it now has the total solar capacity of 3.54 megawatts.

On the flipside, the global economic outlook looks gloomy on the back of ongoing tensions in the Middle East which has taken its toll over commodity markets – crude oil to be specific. This will put a major dent on the cost structure of manufacturing sector.

Copyright Business Recorder, 2026

Comments