Sardar Chemical Industries Limited (PSX: SARC) was incorporated in Pakistan as a private limited company in 1989 and was converted into a public limited company in 1993. The company is engaged in the manufacturing and sale of dyestuffs for leather, paper and textile industries.

Pattern of Shareholding

As of June 30, 2025, SARC has a total of 6 million shares outstanding which are held by 1798 shareholders. Local general public has the majority stake of 69.74 percent in the company followed by Directors, CEO, their spouse and minor children holding 22.47 percent shares. Around 4.06 percent of SARC’s shares are held by joint stock companies and 3.28 percent by NIT & ICP. The remaining shares are held by other categories of shareholders.

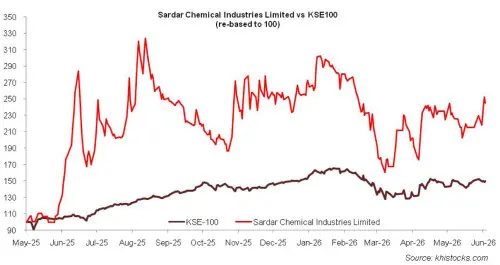

Historical Performance (2019-25)

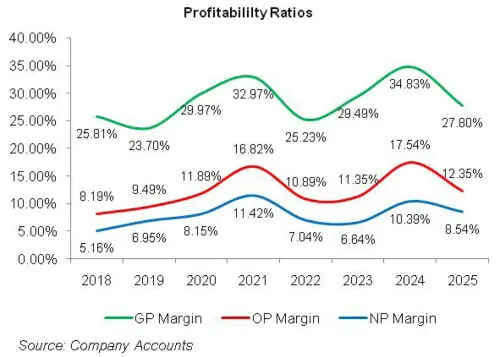

During the period under consideration, SARC’s topline dipped in 2020 and 2023. Conversely, its bottomline plunged in 2022, 2023 and 2025. Its margins portray a fluctuating pattern over the period. In 2019, gross margin plummeted while operating and net margins rose. This was followed by two successive years of growth in margins.

In 2022, the margins significantly eroded while in 2023, gross and operating margins improved while net margin continued to decline. In 2024, margins reached their optimum level followed by a downtick in 2025 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, SARC’s topline grew by 31.05 percent year-on-year to clock in at Rs.268.43 million. This was on account of 1.79 percent increase in the sales volume of the company which clocked in at 386.160 M tons. The company also revised its selling prices in line with elevated prices of energy, transportation, essential raw materials as well as Pak Rupee deprecation. Despite increase in the prices, SARC couldn’t completely pass on the onus of cost hike to its customers, which is evident in the fall of GP margin from 25.81 percent in 2018 to 23.70 percent in 2019.

This was despite 20.34 percent year-on-year growth in gross profit in 2019. Administrative and distribution expenses surged by 4.02 percent and 7.34 percent respectively in 2019 which was on account of higher payroll expense, depreciation as well as travel & conveyance charges. Operating profit improved by 51.88 percent in 2019 with OP margin climbing up from 8.19 percent in 2018 to 9.49 percent in 2019.

Finance cost escalated by 29.85 percent in 2019 on account of higher discount rate as well as increased borrowings. This resulted in a hike in SARC’s debt-to-equity ratio from 19 percent in 2018 to 24 percent in 2019. Net profit strengthened by 76.62 percent in 2019 to clock in at Rs.18.65 million with EPS of Rs.3.11 versus EPS of Rs.1.76 recorded in 2018. NP margin picked up from 5.16 percent in 2018 to 6.95 percent in 2019.

SARC registered 3.9 percent year-on-year shortfall in its topline which clocked in at Rs.257.96 million in 2020. This was on account of drop in sales volume due to COVID related lockdown imposed during the year as well as decline in demand. During the year, SARC operated at 35 percent capacity versus 53 percent capacity utilization achieved in the previous year.

This culminated into production of 230 M tons in 2020. Due to Pak Rupee depreciation, imported chemicals became much more expensive during the year. This coupled with higher electricity and gas prices could have marred the gross profit had the company not implemented effective cost control and price modification strategies.

During 2020, SARC’s gross profit improved by 21.54 percent resulting in GP margin jumping up to 29.97 percent. Administrative expense multiplied by 32.11 percent in 2019 due to increased salaries (including directors’ remuneration), repair & maintenance, rent, rates & taxes as well as loss allowance booked during the year. Distribution expense dropped by 3.4 percent in 2020 on the back of lower carriage & cartage as well as travel & conveyance charges incurred during the year.

Operating profit built up by 20.41 percent in 2020 with OP margin rising up to 11.89 percent. Finance cost mounted by 117 percent in 2020 due to higher discount rate for most part of the year coupled with increased borrowings. This drove up the debt-to-equity ratio to 55 percent in 2020. Net profit progressed by 12.67 percent in 2020 to clock in at Rs.21.02 million with EPS of Rs.3.5 and NP margin of 8.15 percent.

SARC posted 32 percent year-on-year growth in its net sales which clocked in at Rs. 340.50 million in 2021. This was mainly on account of upward revision in the prices of the company’s products due to hike in raw material prices, energy tariff, freight charges as well as Pak Rupee depreciation. The increase in prices was not well received by the customers and hence SARC couldn’t attain any significant growth in its off-take during the year. Capacity utilization stood at 40 percent resulting in the production volume of 267 M tons. Due to passing on the onus of cost hike to its customers, SARC registered 45.19 percent growth in its gross profit with GP margin rising up to an unprecedented level of 32.97 percent in 2021. Administrative expense magnified by 18.72 percent in 2021 on account of higher payroll expense as number of employees grew from 108 in 2020 to 122 in 2021 and also because of higher depreciation expense incurred during the year.

Distribution expense inched up by 2.39 percent in 2021 due to higher utility charges and carriage & cartage charges on account of increased prices of petroleum products. Higher profit related provisioning drove up other expense by 116.19 percent in 2021 while profit recognized on sale of fixed assets resulted in 123.27 percent rise in other income.

All these factors translated into 86.72 percent higher operating profit recorded by SARC in 2021 with OP margin clocking in at 16.82 percent. Finance cost shrank by 26.25 percent in 2021 on account of monetary easing and settlement of all the outstanding short-term borrowings during the year. This took down debt-to-equity ratio to 20 percent in 2021. Net profit improved by 84.93 percent in 2021 to clock in at Rs.38.87 million with EPS of Rs.6.48 and NP margin of 11.42 percent.

SARC’s topline grew by 21.20 percent to clock in at Rs.412.69 million in 2022. This was primarily due to upward price revision with no significant movement in sales volume. Capacity utilization stood at 60 percent, resulting in the production volume of 394 M tons. Despite price modification, the company couldn’t completely pass on the impact of cost hike to its customers. This resulted in 7.26 percent lower gross profit in 2021 with GP margin dropping to 25.23 percent. Administrative and distribution expense grew by 8.73 percent and 9.48 percent respectively in 2022 mainly on account of higher payroll expense (including directors’ remuneration), increased depreciation expense as well as carriage & cartage charges.

Operating profit nosedived by 21.54 percent in 2022 with OP margin contracting to 10.89 percent. Finance cost raised its head yet again and surged by 39 percent owing to monetary tightening. This was despite the fact that SARC replaced its short-term external loans with loans from directors which had 1 percent lesser mark-up than the existing KIBOR. Debt-to-equity ratio stood at 39.66 percent in 2022. Net profit tumbled by 25.26 percent year-on-year in 2022 to clock in at Rs.29.05 million with EPS of Rs.4.84 and NP margin of 7.04 percent.

SARC’s topline withered by 11.24 percent year-on-year to clock in at Rs.366.29 million in 2023. This was on account of closure of industries on account of high inflation, elevated cost of borrowings, crippling demand as well as import restrictions. Capacity utilization stood at 49 percent resulting in the production volume of 322 M tons. SARC increased the prices of its products to compensate for the soaring cost of sales. This resulted in a paltry 3.76 percent uptick in gross profit with GP margin climbing up to 29.49 percent in 2023. 10.52 percent higher administrative expense incurred in 2023 was the result of higher payroll expense and directors’ remuneration as well as bad debts written off during the year. Distribution expense escalated by 32.50 percent year-on-year in 2023 as high prices of petroleum drove up carriage & cartage charges as well as travelling expense. Higher salaries also contributed in driving up the distribution expense in 2023. Operating profit dwindled by 7.49 percent in 2023, however OP margin inched up to 11.35 percent. Finance cost surged by 133.20 percent in 2023 on the back of higher discount rate. Debt-to-equity ratio lowered to 31.23 percent in 2023. SARC recorded 16.26 percent lower net profit to the tune of Rs.24.33 million in 2023 with EPS of Rs.4.05 and NP margin of 6.64 percent.

SARC posted the highest year-on-year topline growth of 37.56 percent in 2024. This resulted in net revenue of Rs. 503.87 million in 2024. Topline growth was due to increased sales volume as well as upward revision in the prices of the company products. Stable macroeconomic indicators in the home market provided stimulus to the local industry resulting in robust demand for SARC’s products. On the contrary, the company didn’t make any export sales in 2024. SARC utilized 55 percent of its total capacity and produced 362 M tons of products in 2024. Cost of sales surged by 27.14 percent in 2024, much lower than the topline growth. This was due to strengthening of Pak Rupee against the greenback as well as stable commodity prices. Moreover, the company also acquired solar system for its factory which resulted in lesser reliance on external energy sources. Gross profit heightened by 62.48 percent in 2024 with GP margin jumping up to its optimum level of 34.83 percent. Administrative expense multiplied by 32.71 percent in 2024 due to higher payroll expense and bad debts recorded during the year. Higher payroll expense was due to inflationary pressure as well as workforce expansion from 126 employees in 2023 to 131 employees in 2024. Distribution expense mounted by 25.30 percent in 2024 due to higher salaries of sales force as well as elevated cartage and carriage charges incurred during the year. Other expense surged by 149.51 percent in 2024 due to increased provisioning done for WWF and WPPF. Other income also rebounded by 295.61 percent in 2024 mainly on account of increased profit on bank accounts. SARC posted 112.5 percent improvement in its operating profit in 2024 with OP margin climbing up to 17.54 percent. Finance cost inched up by 6.37 percent in 2024 due to higher discount rate as well as long-term loan obtained under renewable energy (REEF) category. SARC recorded 115 percent higher net profit to the tune of Rs.52.33 million in 2024. This translated into EPS of Rs.8.72 and NP margin of 10.39 percent.

In 2025, SARC’s net sales ticked up by 5.95 percent to clock in at Rs.533.86 million. This was due to increased sales volume and prices. During the year, SARC’s capacity utilization was recorded at 71 percent, resulting in the production of 467 M tons. Cost of sales mounted by 17.39 percent in 2025 due to higher raw material prices. Elevated cost was despite the fact that the solar system installed during the last year became fully operational in 2025. Gross profit tapered off by 15.45 percent in 2025 with GP margin falling down to 27.80 percent. Administrative expense ticked down by 5.52 percent in 2025 due to high-base effect as the company registered bad debts of Rs.9.008 million in the previous year versus no bad debts recorded in 2025. Distribution expense multiplied by.4.95 percent due to higher salaries of sales force. Other expense tumbled by 30.60 percent in 2025 due to lower provisioning done for WWF and WPPF. Other expense was completely offset by 9.24 percent higher other income recorded in 2025 which was the result of greater deferred grant income recorded in 2025. SARC recorded 25.39 percent plunge in its operating profit in 2025 with OP margin falling down to 12.35 percent. Finance cost escalated by 9.57 percent in 2025 due to increased borrowings. Net profit eroded 12.85 percent to clock in at Rs.45.60 million in 2025. This translated into EPS of Rs.7.6 and NP margin of 8.54 percent in 2025.

Recent Performance (9MFY26)

During the nine-month period of the ongoing fiscal year, SARC’s net sales ticked up by 1.82 percent to clock in at Rs.403.06 million. Sales volume deteriorated during the period due to ongoing tensions in the Middle East. Cost of sales tapered off by 6.28 percent in 9MFY26 due to scaling back of operations. This resulted in 23.37 percent higher gross profit in 9MFY26 with GP margin clocking in at 33.11 percent versus GP margin of 27.33 percent recorded in 9MFY25. Administrative expense tumbled by 5.77 percent in 9MFY26 likely due to lower travelling & conveyance expense and payroll expense due to curtailed operations. Distribution expense mounted by 16.94 percent in 9MFY26 seemingly due to higher salaries of sales force as the company was looking for opportunities in other geographical markets. SARC recorded 59.76 percent greater operating profit in 9MFY26 with OP margin clocking in at 17.92 percent versus OP margin of 11.42 percent recorded in 9MFY25. Finance cost diminished by 25.58 percent in 9MFY26 due to monetary easing. Net profit strengthened by 76.81 percent to clock in at Rs.47.97 million in 9MFY26. This translated into EPS of Rs.7.99 and NP margin of 11.90 percent in 9MFY26 versus EPS of Rs.4.52 and NP margin of 6.85 percent recorded in 9MFY25.

Future Outlook

While local demand is stable, the company is unable to take the optimum benefit out of it on account of heightened sales tax imposed on its products. This also impedes the company from increasing its prices to pass on the onus of cost hike to its customers. However, the company is focusing on operational excellence and cost optimization to stay competitive and improve its profitability and margins. Alternatively, SARC is diversifying its sales mix by tapping new industries and geographical markets. This will result in sustained demand and profitability.

Comments