Large-Scale Manufacturing is beginning to look less like a comeback story and more like a return to normalcy.

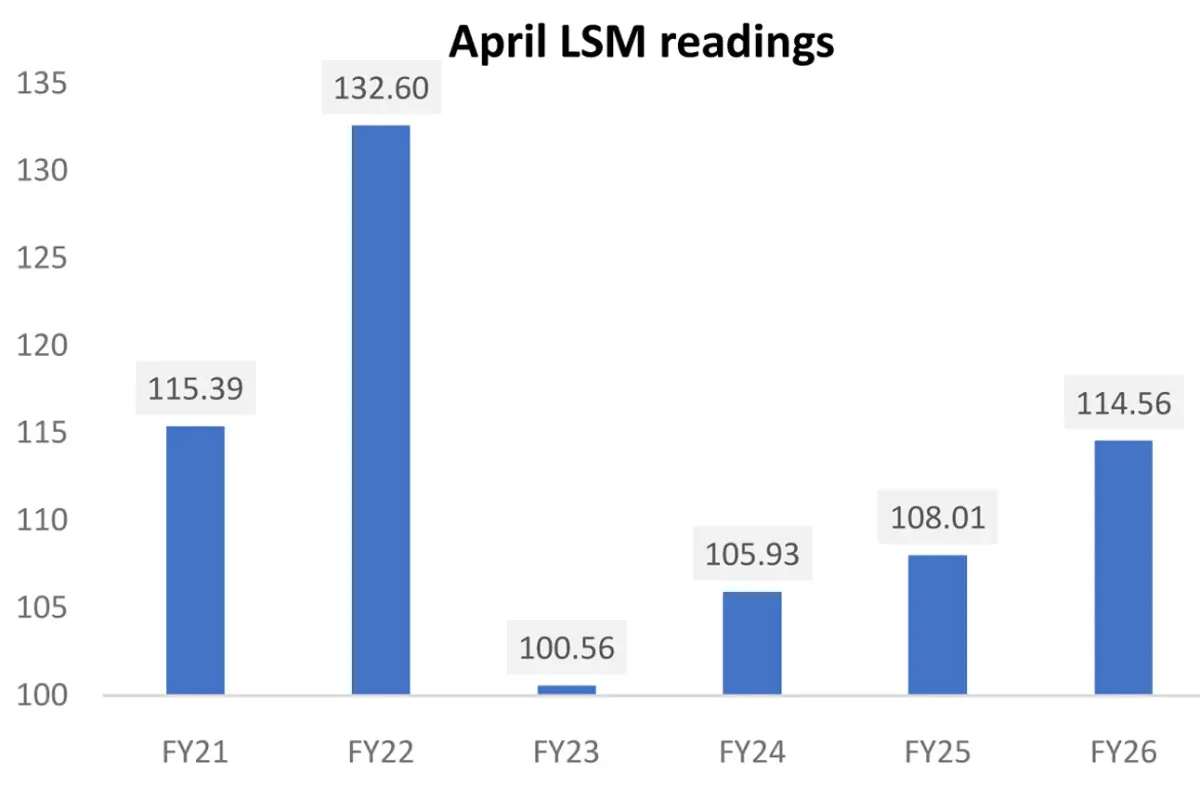

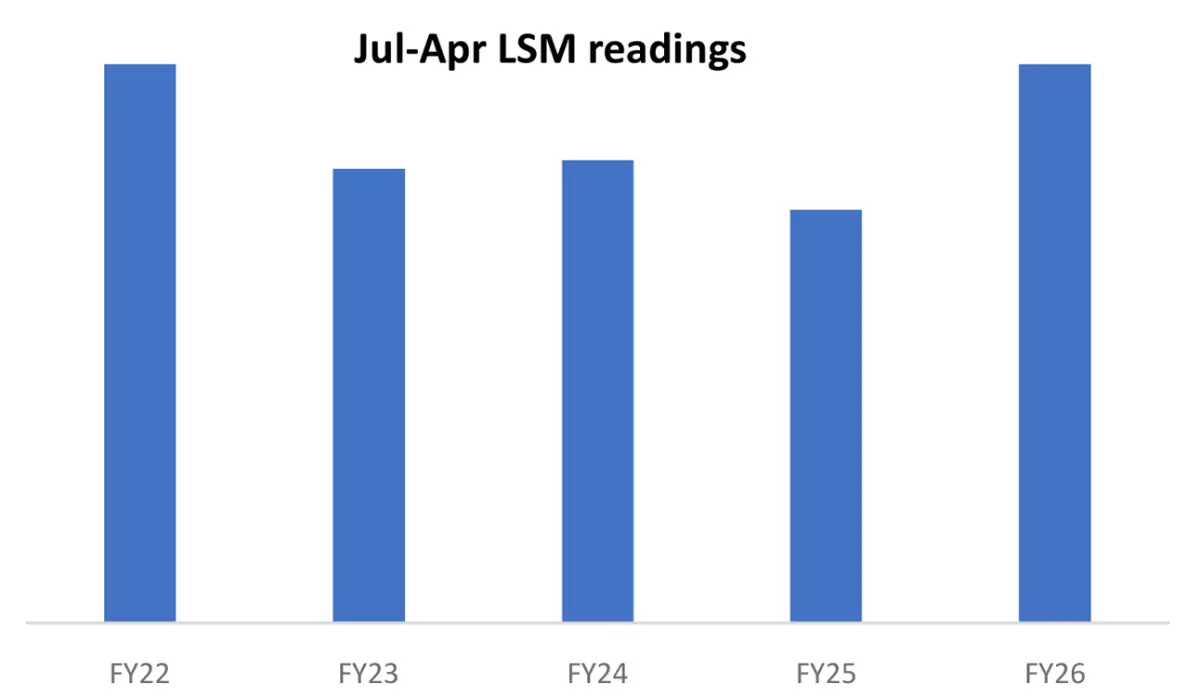

April 2026 marked another month of healthy expansion, with LSM growing 6.06 percent year-on-year. Cumulative growth for 10MFY26 now stands at 6.44 percent, comfortably keeping the sector on course to meet the broader annual target.

The pace may have settled below the double-digit prints seen in January and March, but the consistency is becoming the more compelling story.

The recovery continues to rest on a much wider foundation than in previous cycles. Sixteen of the 22 LSM sub-sectors are now in positive territory, leaving only six in contraction.

More importantly, the laggards largely carry smaller weights, suggesting the expansion is no longer hostage to the fortunes of one or two industries.

Perspective, however, remains important. Despite the improvement, both the monthly and cumulative LSM indices remain around 14 percent and 4 percent below the highs recorded in FY22. That gap has narrowed, but it also serves as a reminder that the current cycle is more about reclaiming lost industrial ground than breaking into uncharted territory. FY22 remains the benchmark, and there is little to suggest it will be matched this year.

The composition of growth also continues to evolve. Automobiles remain the largest contributor on a cumulative basis, followed by food and wearing apparel. April’s monthly story, however, was led by automobiles and wearing apparel, with furniture unexpectedly making its way into the top contributors. Given furniture carries barely half a percent weight in the overall index, its contribution is more of a statistical curiosity than a signal of a broader structural shift.

Food continues to provide an important cushion. Sugar production remains on course for its strongest season in years, reinforcing the sector’s contribution to overall manufacturing growth. Meanwhile, cigarettes have staged a notable comeback, with production touching a 36-month high. The improvement is widely attributed to lower illicit sales, helped by tighter movement restrictions during the recent period of regional tensions.

Consumer demand is also showing tentative signs of broadening. Motorcycle and bicycle production climbed to 48-month and 70-month highs, respectively, while white goods are quietly making a comeback. Refrigerator and deep freezer production during April stood roughly one-third above their average monthly levels over the previous four years, hinting at improving household demand. Construction-linked industries, however, continue to disappoint, with little evidence yet of a meaningful pickup in building materials.

Forward indicators present a mixed picture. Business confidence remains subdued, inflation expectations are still elevated, and manufacturing capacity utilization continues to hover around 66 percent without breaking decisively higher. In other words, output is recovering faster than sentiment.

The policy backdrop, however, is becoming increasingly supportive. Industrial electricity tariffs have fallen meaningfully over the past year, improving Pakistan’s manufacturing competitiveness. Should calm on the Iran-US front hold, lower energy prices would provide another tailwind. Monetary policy also appears close to an inflection point. Assuming oil prices remain contained, the current pause in the interest rate cycle could give way to easing later in the year, providing further support to industrial activity.

Early signals for the current month are encouraging. Wearing apparel exports have already posted around 18 percent growth in May, suggesting the sector will remain a major contributor to 11MFY26. Automobile sales also continue to build momentum despite increasingly demanding base effects.

The industrial recovery still has considerable distance to cover before it can rival FY22. But that is becoming a less useful benchmark for judging current performance. What matters more is that the gains are proving durable, sectorally diverse and increasingly supported by improving macro fundamentals. That makes this recovery look considerably more sustainable than the false starts of recent years.

Comments