Remittance rush: Don’t miss the fine print!

Pakistan saw record remittances in May 2026, largely driven by UAE inflows and the Eid calendar effect, but this surge is likely a temporary windfall rather than a sustainable trend.

- Record $4.25 billion in workers' remittances in May 2026.

- Unprecedented surge in remittances from the UAE.

- The temporary nature of the current remittance windfall.

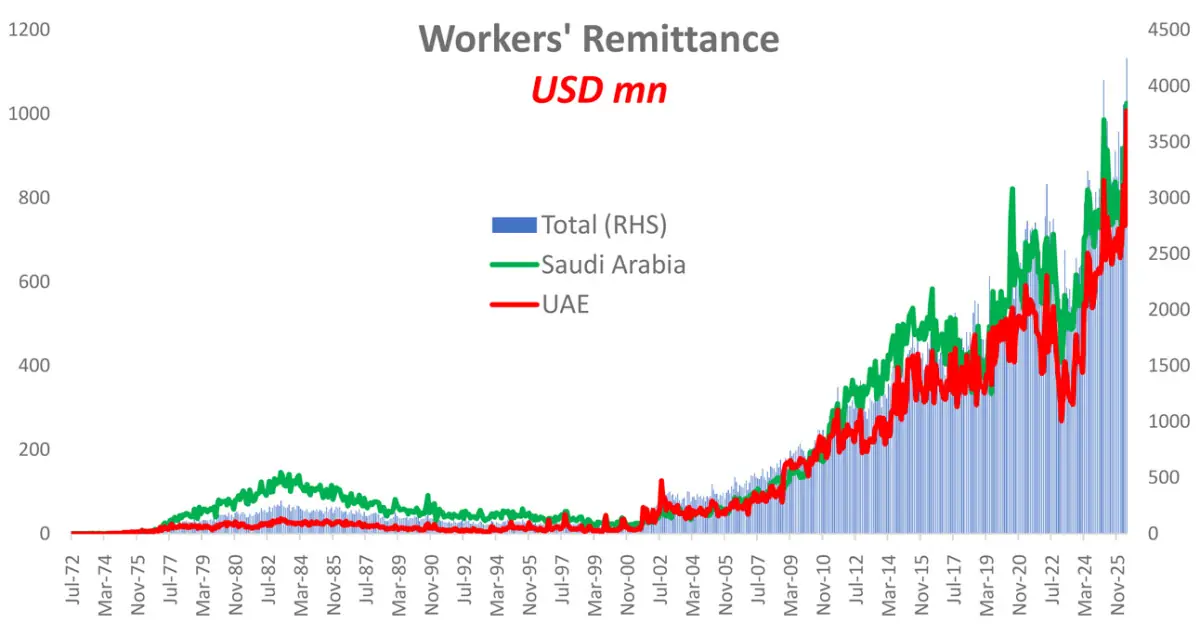

The headline number is hard to ignore. Workers’ remittances touched an unprecedented $4.25 billion in May 2026, the highest monthly inflow on record and only the second time the $4 billion mark has been breached.

Cumulative inflows for 11MFY26 now stand at nearly $38 billion, up 9 percent year-on-year.

Impressive, certainly. But not all of it should be read as a structural shift.

The first point to note is that May’s 15 percent annual growth is actually below the average growth rate seen over the previous two years.

The record owes much to the calendar. EidulAzha fell towards the end of May this year, concentrating almost the entire cycle of festive transfers into a single month. Last year, the effect was likely spread across two months.

Comparing the two without adjusting for this timing distortion risks overstating the underlying momentum.

That does not mean there is no organic growth. A stronger formal channel, exchange rate stability, and a still sizeable overseas workforce continue to support inflows. But the Eid effect deserves a meaningful discount before extrapolating the latest number into the future.

The real story lies elsewhere: the UAE.

Remittances from the UAE crossed the $1 billion mark in a single month for the first time ever, accounting for nearly one-fourth of Pakistan’s total inflows. The UAE has contributed a similar share before, particularly during FY20, but never at this scale. The latest reading is roughly 20 percent above the previous peak, making it difficult to attribute the surge to seasonal factors alone.

The market has no shortage of explanations. One view is that wealth parked in the UAE is gradually finding its way back to Pakistan as geopolitical uncertainty and a deterioration in regional conditions alter risk calculations. Another is that returning workers are repatriating accumulated savings before relocating permanently. The truth is probably a combination of both.

An analogy may help. Regular remittances are like a salary credited every month. What appears to be happening now is that a sizeable number of households are also withdrawing from their savings accounts. Both raise bank balances, but only one is recurring income.

That distinction matters because one-off capital repatriation can create a temporary windfall without altering the long-term trend. Once accumulated savings have been transferred, the flow naturally tapers off.

The labour market data also warrants caution. Even before the recent regional turmoil, Pakistan’s worker outflow to the UAE had slowed sharply. Bureau of Emigration and Overseas Employment figures show annual registrations dropping to nearly a quarter of the levels seen just three years ago and well below long-term averages. The UAE economy itself is facing a softer patch, reducing its capacity to absorb migrant labour at the pace seen in the past.

The immediate macroeconomic impact will depend on where the money ends up. If it feeds consumption, it could add to demand-side inflation pressures that are already beginning to re-emerge. If, as often happens in Pakistan, it is channeled into real estate and asset markets, the inflationary effect may be more contained but could inflate property valuations.

Either way, it would be risky to assume that the current pace of UAE-led remittance growth is sustainable. No one has a reliable estimate of the stock of savings or wealth that could still be repatriated, making it impossible to predict when the cycle will turn. But cycles do turn.

For now, Pakistan is enjoying a remittance windfall. Policymakers would be wise to treat it as exactly that: a welcome but temporary boost, not a new normal. The sun is shining. The challenge is to make use of the bonanza before the tide inevitably changes direction.

Comments