IMF macroeconomic projections for FY27

The article critiques IMF's 2026-27 macroeconomic projections for Pakistan, finding external balance forecasts overly optimistic due to geopolitical factors, while fiscal projections are largely more realistic.

- IMF's optimistic external balance projections for Pakistan.

- Geopolitical factors impacting Pakistan's foreign exchange reserves.

- IMF's more realistic public finance outlook for Pakistan.

This is the second article on the IMF Mac roeconomic Proj ections for 2026-27 as contained in the IMF Staff Mission report on the third review of the IMF Program.

The first article last week had highlighted that despite the on-going Middle East war and a shortage and quantum jump in oil prices, the projections for GDP growth and the rate of inflation in 2026-27 by the IMF are unduly optimistic.

This article focuses on the external balance of payments position of Pakistan in 2026-27 and the consolidated budgetary outcome of the federal and the provincial governments next year.

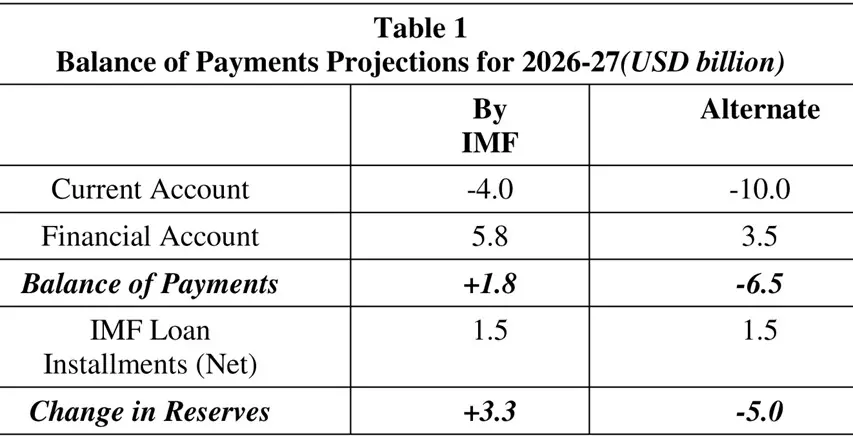

We first highlight the key projected magnitudes in the different accounts in the balance of payments.

The current account deficit is expected to rise from USD 2 billion in 2025-26 to USD 4 billion in 2026-27. The financial account is projected to show a sizeable surplus of USD 5.8 billion, with a big jump expected in foreign direct and portfolio investment inflows and loans.

Overall, the, foreign exchange reserves, after receipt of IMF loan installments, are projected to increase from USD 17.3 billion at the end of 2025-26 to USD 20.2 billion by the end of 2026-27.

This implies that Pakistan would finally attain a secure position financially of over three months of equivalent import cover of foreign exchange reserves. The IMF Programme can then be declared as being exceptionally successful and Pakistan can avoid going again into an IMF Programme.

The IMF projections for the external balance of payments position of Pakistan in 2026-27 are extremely optimistic. They ignore the negative consequences of the Middle East war if it persists and the Strait of Hormuz remains closed.

Already, the negative impacts have become visible. The monthly current account has turned from positive to negative in April 2026. Exports have declined while imports have gone up by as much as 14 percent. Remittances have fallen by over 7 percent in relation to the level in March.

Foreign direct investment in Pakistan has plummeted in the first ten months of 2026-27 by over 44 percent. There has also been a sizeable exit of portfolio funds. Overall, the balance of payments has been deficit. The reserves increased marginally due to the receipt of a loan installment from the IMF.

There is clearly a strong need for reflecting the impact of the Middle East war and the blockage of the Strait of Hormuz as follows:

(i) Rise in the import bill in 2026-27 due to continued higher price of crude oil and petroleum products.

(ii) Some sliding down of exports due to a global recession, especially in the European Union, which is the major market for Pakistani exports.

(iii) Fall in remittances, especially from the UAE and Saudi Arabia.

(iv) Continuation of low foreign investment inflows.

Overall, a careful projection of the balance of payments implies a fall in foreign exchange reserves by the end of 2026-27 by USD 5 billion, as shown in Table.

Therefore, there is a stronger likelihood of a big drop in foreign exchange reserves of USD 5 billion, which could take Pakistan’s reserves to USD 12 billion by the end of 2026-27.

Turning to the projected state of public finances of Pakistan in 2026-27 by the IMF, these are on the more realistic side.

The growth rate in FBR revenues is projected to approach almost 14 percent, more or less, in line with the growth rate this year. The only real question is about the 54 percent growth in provincial tax revenues, with additional taxation of Rs 400 billion.

The IMF Programme has been pushing, in particular, for development of the agricultural income tax by the provincial governments. Accordingly, changes have been made in the law. But this has not translated into higher revenues.

The process of state capture by the elite of large agricultural landowners has continued. The fundamental question is whether efforts will be made by the provincial governments to generate revenues from this source in 2026-27. The revenue potential is sizeable at over Rs 800 billion, with the same tax treatment of agricultural income as other personal income.

Non-tax revenues are expected to show a big drop. of over 25 percent in 2026-27, due particularly to a big fall in SBP profits, with the fall in interest rates from the peak level in 2022-23. However, this has simultaneously also reduced the cost of debt servicing by almost 18 percent in 2025-26. However, the expenditure under this head is anticipated to rise once again by over 7 percent, as SBP gets back to raising interest rates on the back of much higher inflation in 2026-27.

An ambitious target accepted by the IMF is 26 percent increase in the level of development expenditure by the federal and provincial governments combined in 2026-27. Hopefully, the emphasis will be on augmentation especially of water resources through earlier completion of the on-going projects.

The underlying fiscal balance is expected is to be 3.5 percent of the GDP in 2026-27, compared to 4.1 percent of the GDP in 2025-26. The primary positive balance is projected to increase by almost 40 percent to Rs 2830 billion in 2026-27.

The fiscal projections by the IMF indicate a significant improvement in the consolidated financial position in 2026-27. The only target which is challenging in nature is the increase in provincial tax revenues by 54 percent.

Overall, the IMF projections of the balance of payments in 2026-27 are far too optimistic. They are on the more realistic side on the consolidated fiscal position of the federal and provincial governments next year, with the exception of the much larger provincial tax revenues target.

Copyright Business Recorder, 2026

The writer is Professor Emeritus at BNU and former Federal Minister

Comments