FDI: still waiting for a turn

Pakistan's foreign direct investment remains weak, marked by declining net inflows, high outflows, and concentration in a few sectors and countries, due to an unpredictable investment climate.

- Declining net foreign direct investment and high outflows.

- FDI concentration in specific sectors and a few countries.

- Unpredictable policies and regulatory hurdles for investors.

It has been ages since foreign direct investment brought genuinely good news for Pakistan. Every now and then, a slightly better monthly number creates a headline of hope, but the larger picture remains bleak: weak inflows, high outflows, a narrow investor base, and an economy still struggling to convince long-term investors that Pakistan is a safe and predictable place to put capital.

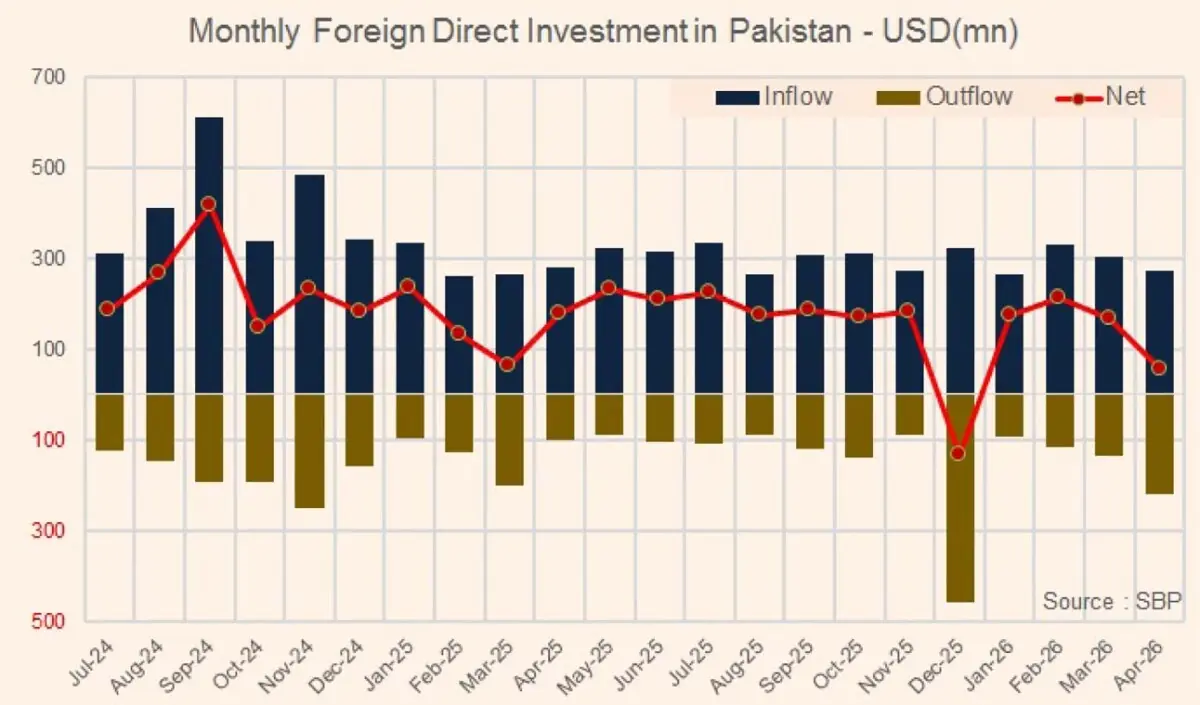

April 2026 summed up the problem. Pakistan received FDI inflows of USD273.4 million during the month, but outflows of USD218.9 million brought net FDI down to just USD54.5 million. That is hardly a confidence-building number. For a country that desperately needs foreign capital, technology, jobs, and export capacity, this is not the kind of investment story that inspires comfort.

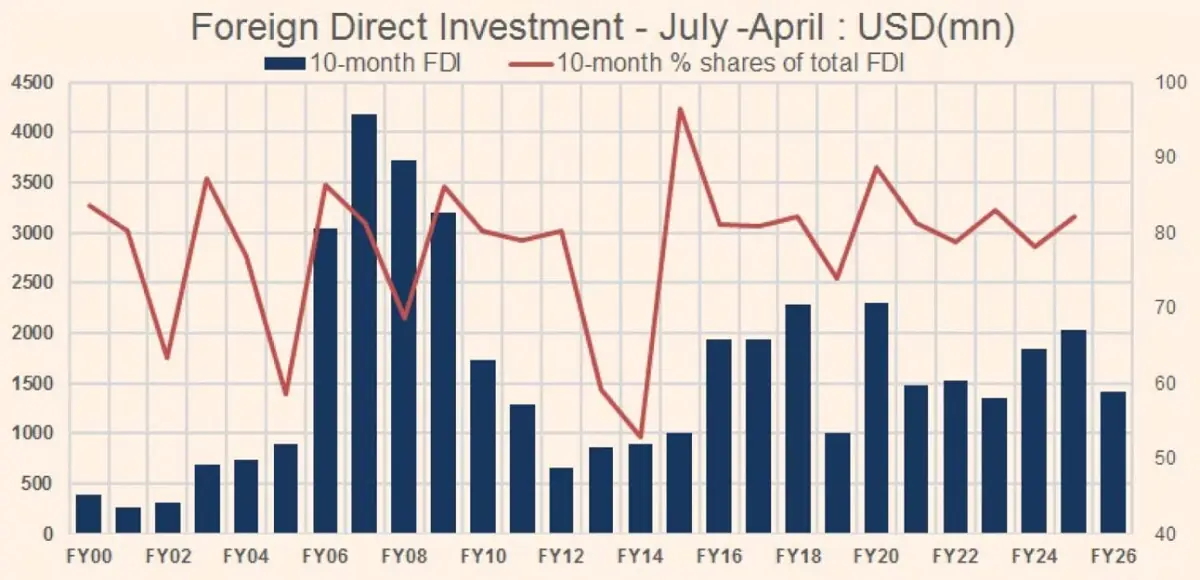

The 10-month numbers are even more sobering. Net FDI in July-April FY26 stood at USD1.409 billion, compared to USD2.035 billion in the same period last year — a decline of around 31 percent. Gross inflows also fell, from USD3.632 billion to USD2.978 billion, while outflows remained high at USD1.569 billion. In plain terms, Pakistan is attracting less investment and retaining too little of what it attracts.

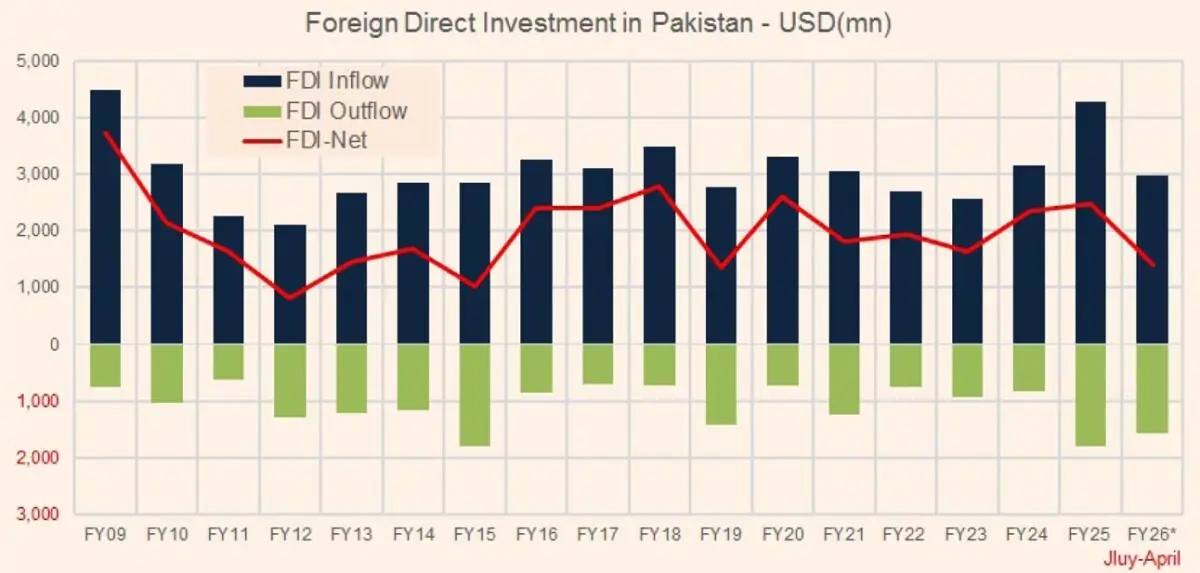

This is not just a bad month. It is part of a long pattern. Pakistan’s FDI has been stuck in a low-growth zone for years. In some years, the numbers improve slightly; in others, they fall back again. But the country has rarely seen the kind of sustained, broad-based foreign investment that can change the direction of the economy.

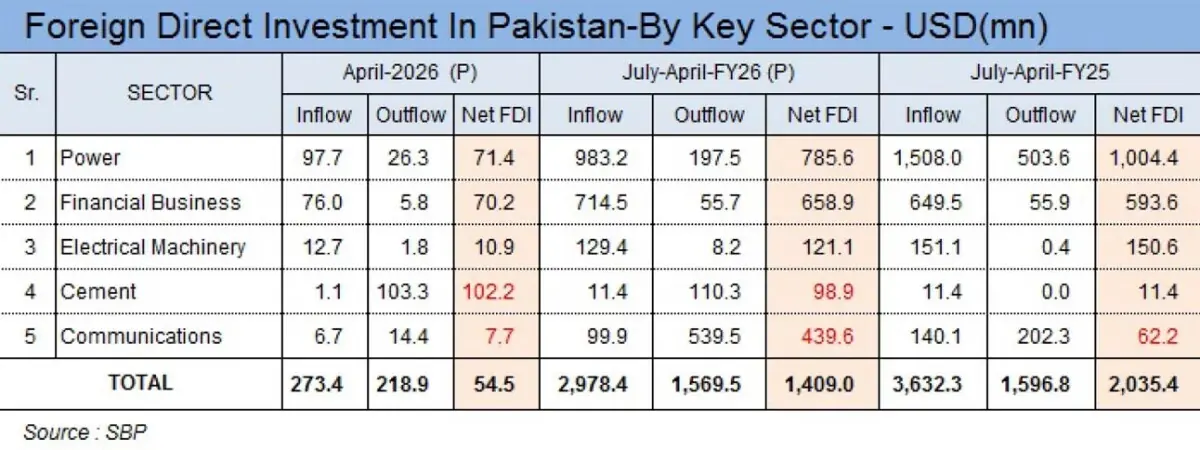

The sectoral breakup tells its own story. Power remained the largest recipient of FDI in 10MFY26 with net inflows of USD785.6 million, followed by financial business at USD658.9 million. Together, these two sectors carried most of the investment account. Electrical machinery received USD121.1 million, while communications stood at only USD43.9 million. Cement, meanwhile, saw a sharp reversal in April, with outflows of USD103.3 million, leaving the sector with a negative monthly net FDI of USD102.2 million.

That is the worrying part. Pakistan is not seeing a strong foreign push into export-oriented manufacturing, technology, engineering, pharmaceuticals, logistics, agribusiness, or high-value services.

The investment that comes in is still concentrated in a few regulated or infrastructure-linked sectors. That may help, but it does not create the diversified industrial base Pakistan needs.

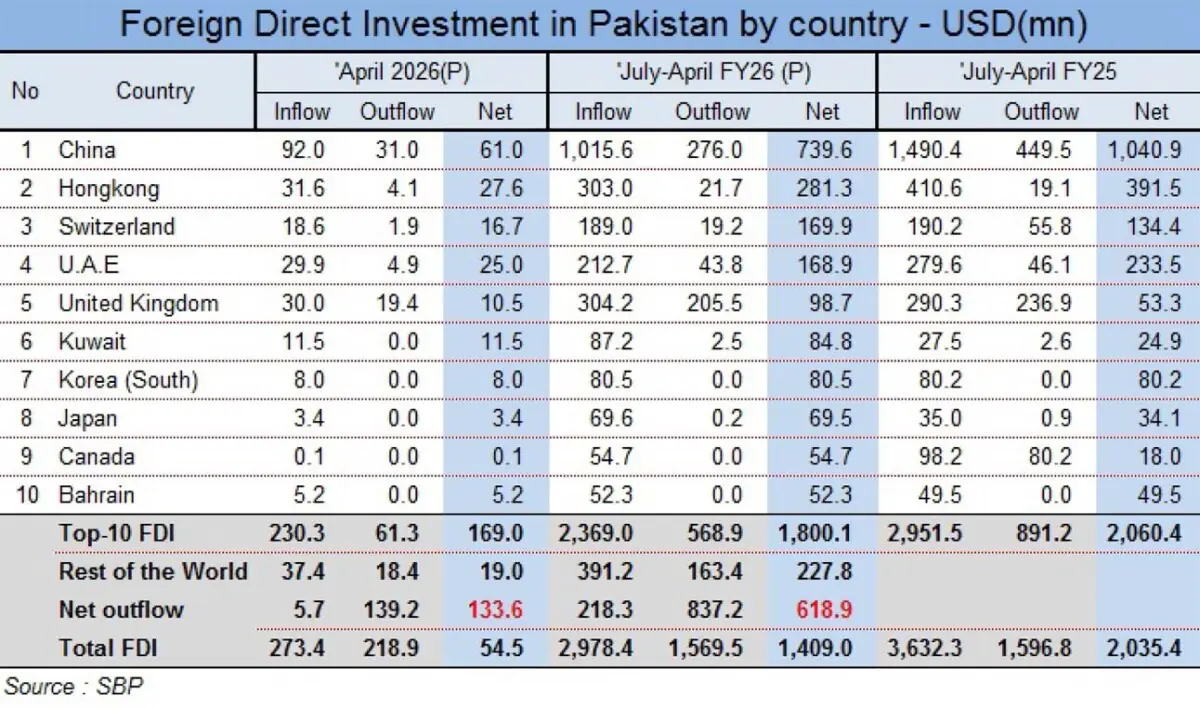

The country-wise numbers show the same narrowness. China remained the largest investor, with net FDI of USD739.6 million in 10MFY26, though this was down from USD1.041 billion in the same period last year. Hong Kong followed with USD281.3 million, the UAE with USD168.9 million, the UK with USD98.7 million and South Korea with USD80.5 million.

The top 10 countries accounted for USD1.800 billion, while the rest of the world contributed only USD227.8 million. Pakistan’s FDI story remains dependent on a small group of countries.

The reasons are not hard to understand. Investors can deal with difficult markets, but they struggle with unpredictable ones.

Pakistan has too many moving parts: frequent tax changes, uncertain energy pricing, approval delays, repatriation concerns, weak contract enforcement, circular debt, political noise, and regulatory overlap between federal and provincial authorities. For investors, each adds another layer of risk.

This is why macroeconomic stabilization alone is not enough. A better current account number may please lenders. An IMF programme may reduce default risk. Higher reserves may calm markets for a while.

But long-term investors look beyond the next quarter. They ask whether policies will remain stable, whether profits can be repatriated, whether contracts will be honoured, whether taxes will suddenly change, and whether they can expand without getting trapped in approvals.

Until Pakistan fixes that trust deficit, FDI will remain what it has been for far too long: occasional inflows, persistent outflows, narrow concentration, and recurring disappointment.

Comments