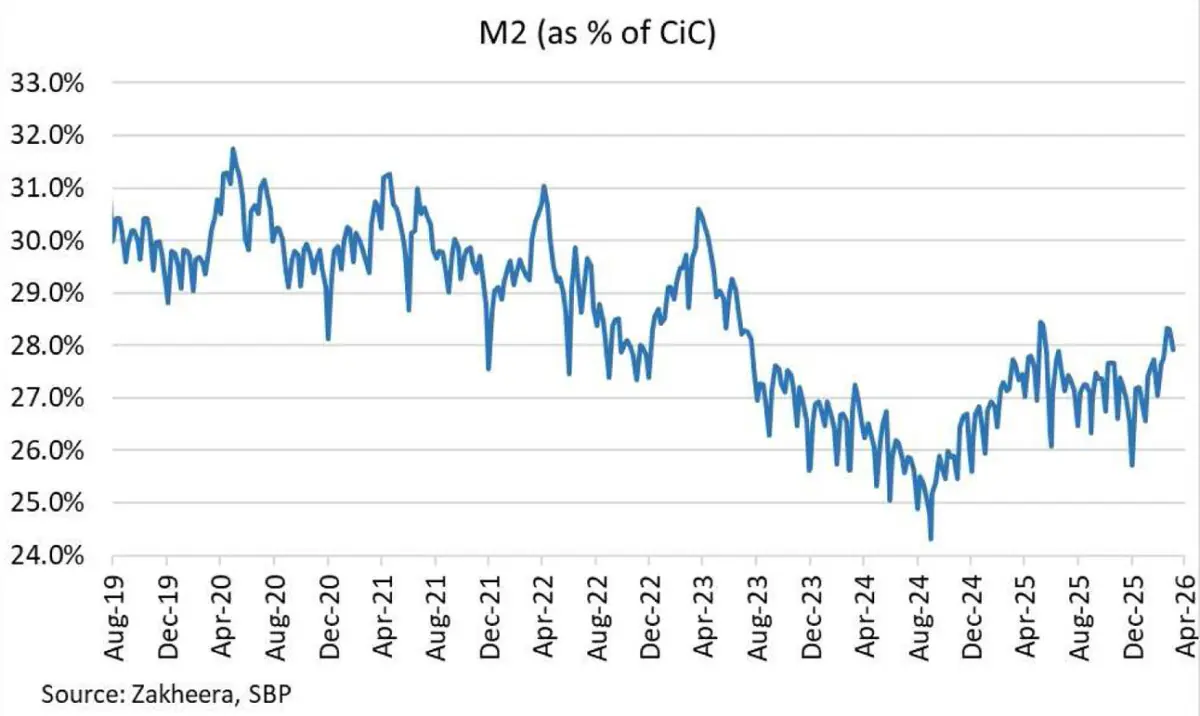

In days of growing digitization and cashless economy, seeing the currency in circulation (CIC) to its highest absolute level (and close to the peak in percentage of M2) is a point of concern. There are seasonal factors (such as Eid) to explain the growth, but barring that, its spikedepicts growing anxiety around economic outlook, low interest rates and mistrust with the taxman.

A snapshot of the last few years depicts clearly that when real interest rates fall the CIC grows. It peaked (in percentage terms) in April 20 when the interest rates were lowered significantly in response to COVID slowdown.

The real rates were negative and economic outlook was bleak. In such scenarios, people tend to take the money out of the banking system.

A similar spike was seen in April-June 2022 – when after the vote of no confidence the newly formed PDM government did not pass on the increase of petroleum prices to the consumers.

Real rates were negative and economic outlook was bleak. A similar episode repeated in 2023 when the economy was on the verge of default on its external debt and PKR was kept artificially appreciated.

Memories of these crises are fresh, and the markets reactto them. No one was expecting a similar trend to come back in 2026, as so-called stabilization was cemented and economy was moving towards growth while the political system is stable. However, CIC trend suggests that it’s not all hunky-dory.

There appears to be growing anxiety on the Pakistan economic outlook due to ongoing Iran-US war. Inflationary expectations are building and the opportunity cost of taking money out of the system is falling, as perhaps participants think that the real rates (on a forward-looking basis) are negative and they may have a view that PKR may depreciate.

Plus, the mistrust between the tax authority and businesses is growing, the tax rates are exuberantly high and the incentive to become informal is growing. That may result in chunks of business activities move out of the formal system.

There is a cost the government pays. Overall banking system deposits fall – as M2 mainly constitutes of CIC and bank deposits. Hence, when CIC grows, bank deposits fall. In days of growing government borrowing needs, which are to be filled by domestic banking system, the open market operations (OMO) injections spike, as banks would have less deposits (labilities) to invest in government papers (assets). Hence, OMO injections increase which has crossed Rs15 trillion whose impact is like government borrowing from the central bank.

The bottom line is that informality is growing. The first line of defense is interest rates. If interest rates are raised, the opportunity cost of holding cash will grow, and liquidity may revert to the system.

SBP must be seeing this trend carefully and should include it in its presentation to the monetary policy committee which is meeting on Monday.

Comments