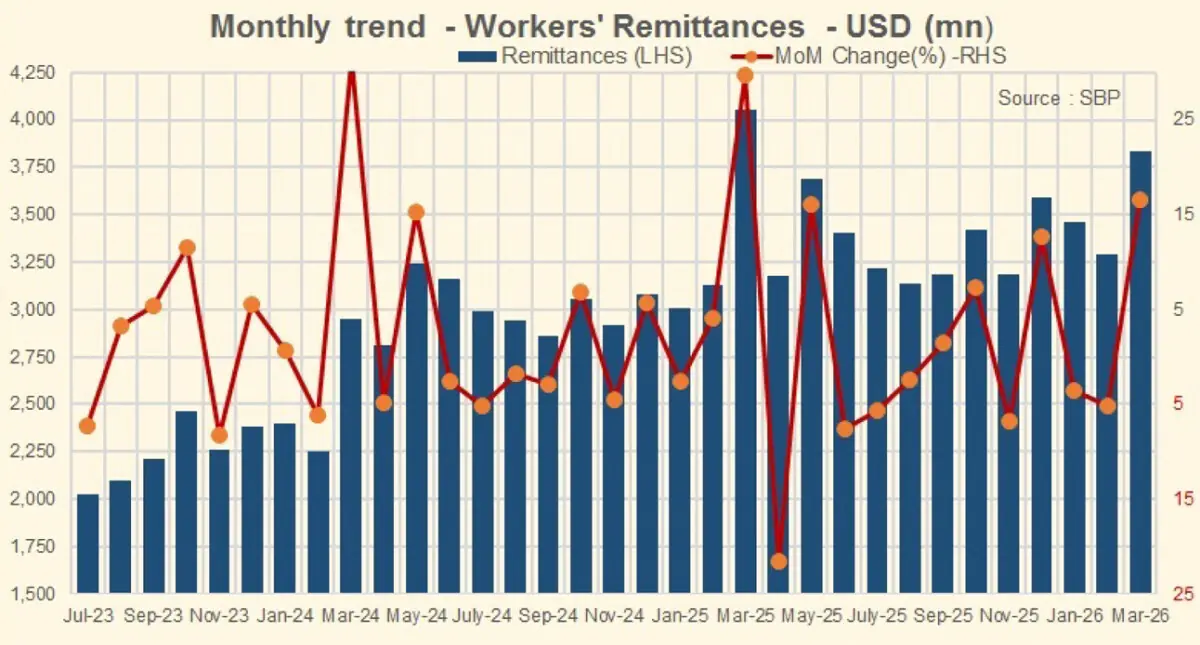

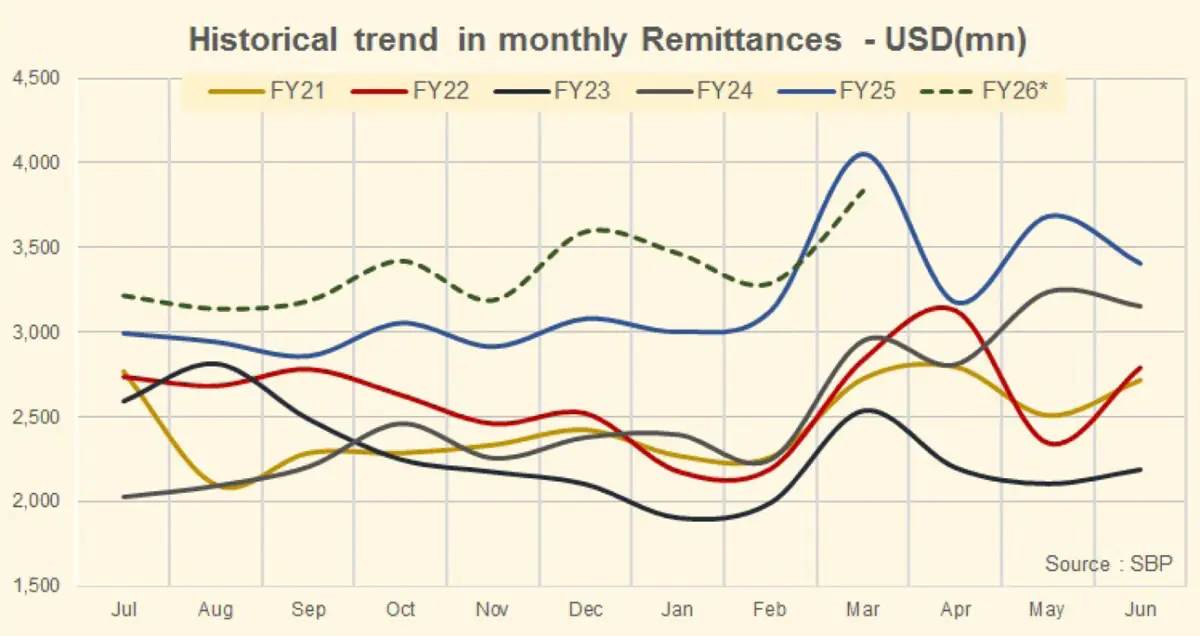

Pakistan’s remittances offered welcome relief in Mar-26, but the comfort came with a warning. Overseas Pakistanis sent home $3.8 billion during the month, a strong 16.5 percent jump over Feb-26 and the highest monthly inflow of FY26 so far. Yet the same number was still about 5.5 percent lower year-on-year.

The month-on-month rise was hardly surprising. March captured much of Ramzan and the run-up to Eid, a period when overseas workers usually send more money to support household spending back home. That seasonal uplift mattered, but the real significance lies beyond the calendar effect.

It came at a time when Pakistan’s external account is again under pressure and when regional geopolitical tensions had begun to raise questions about the durability of Gulf-linked inflows.

In that context, the March number was reassuring, but not enough to end the debate.

The broader nine-month picture remains solid. During 9MFY26, remittances reached $30.3 billion, up 8.2 percent year-on-year. That is still a robust performance by any recent standard and keeps Pakistan on track toward the official expectation of around $40 billion for the full year. To get there, the country would need $9-10 billion in the last quarter, slightly over $3 billion per month.

Despite the growth, that target looked difficult as the regional conflict intensified. However, with a ceasefire now in place, the odds of achieving it have improved, provided stability holds.

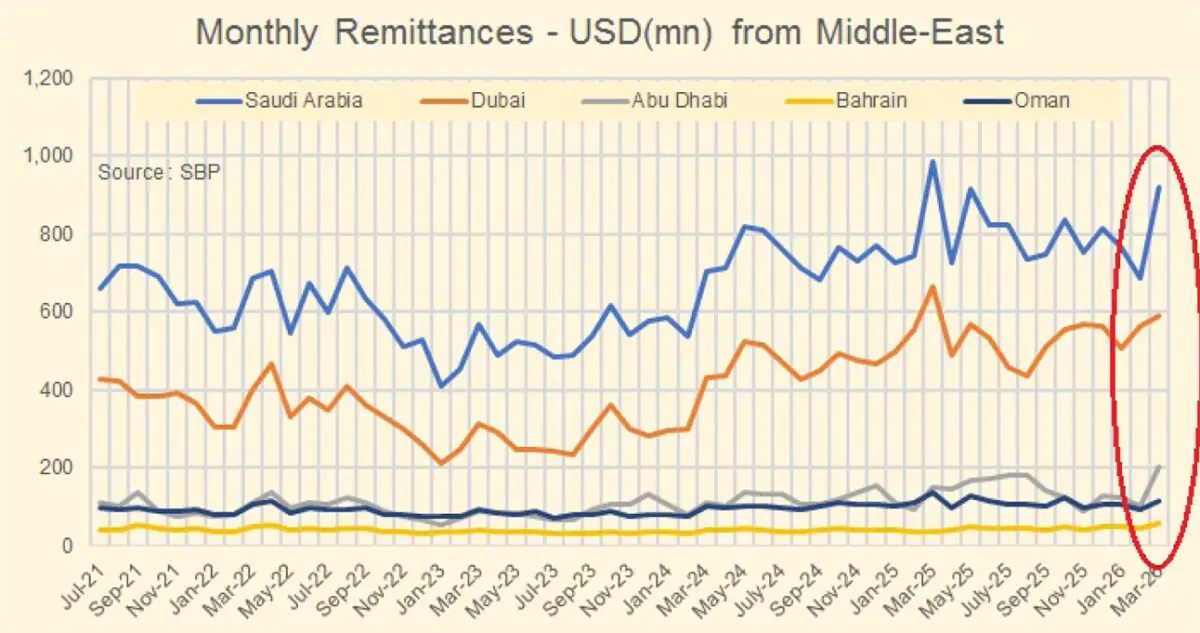

The corridor-level picture, however, is more mixed than the cumulative total suggests. Saudi Arabia remained the largest source of inflows in March, followed by the UAE, the UK, and the US. But on a year-on-year basis, remittances from Saudi Arabia, the UAE, the UK, and the US all declined during the month. The 9MFY26 data looks healthier: Saudi inflows were up 3 percent year-on-year, UAE inflows rose 10 percent, and the UK and EU posted solid gains. That tells us Pakistan’s remittance base has not weakened structurally, but it also shows that the monthly flow is becoming more vulnerable to swings in regional conditions.

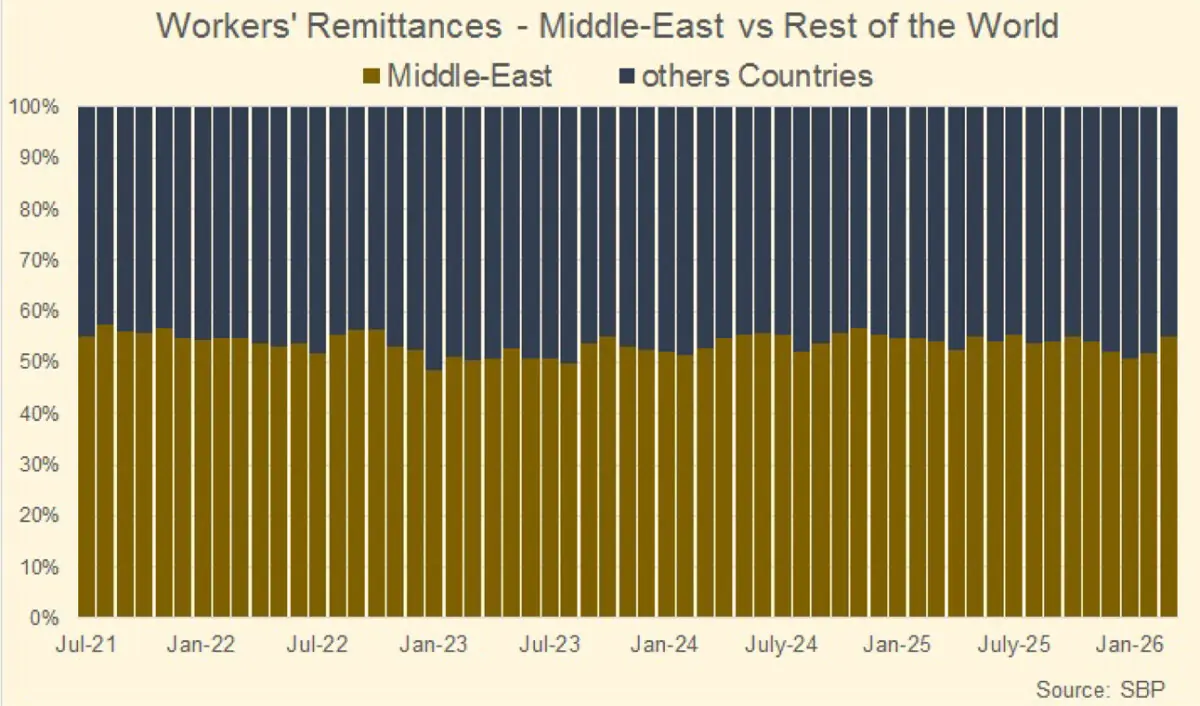

What matters more is the vulnerability underneath the headline number. Pakistan does not just rely heavily on remittances; it relies heavily on a very narrow set of markets. More than $20 billion a year, roughly half of total remittance inflows, comes from the Gulf. Saudi Arabia alone accounts for about a quarter, while the UAE contributes around one-fifth. With remittances now equal to roughly 9 to 10 percent of GDP, Pakistan is unusually dependent on the health of Gulf economies. That has always been a weak spot, but the latest regional tensions have made it much more visible.

The risk is easy to understand. If oil prices remain high, Pakistan’s import bill will rise further. But if the same regional stress also slows Gulf economies or disrupts activity there, remittance growth could begin to soften as well. That would leave Pakistan squeezed from both sides: higher payments going out for imports and weaker inflows coming in from overseas workers.

There is also a bigger lesson here. Comparative countries such as India and the Philippines have built more diversified remittance bases, both geographically and in terms of the kind of jobs their workers hold abroad. Pakistan, by contrast, still depends largely on low- and semi-skilled labour markets in the Gulf. That model has supported the economy for years and remains a lifeline for many households. But it also means Pakistan’s external stability rests too heavily on a small number of countries and sectors.

Comments