Oil shock from ME tensions threatens to widen Pakistan’s C/A

- Analysts say Pakistan remains highly vulnerable to energy shocks

Rising tensions between Iran, Israel and the United States have pushed global oil prices well above the $100 per barrel, raising fresh concerns over Pakistan’s fragile external account, with experts alarmed at a sharp deterioration if the conflict continues.

Analysts say Pakistan remains highly vulnerable to energy shocks due to structural inefficiencies and a heavy reliance on imported fuels.

Ali Khizar, Director Research at Business Recorder, noted that Pakistan’s energy-to-GDP efficiency is significantly lower than that of regional peers, including Bangladesh and India, making the economy more exposed to price spikes.

He maintained that Pakistan’s key industries, such as textiles, cement and fertilisers, are energy-intensive, which amplifies the impact of higher fuel costs.

“Therefore, energy price shocks in Pakistan are higher as we are energy inefficient.”

Khizar pointed out that energy prices have already surged by around 60% compared to last year, warning that at current levels, Pakistan’s oil import bill could rise by nearly 50% this fiscal year.

He estimated that every $10 per barrel increase in oil prices adds roughly $1.5 billion to the country’s annual oil bill, putting immediate pressure on the current account.

While Pakistan has benefited from reduced reliance on imported LNG due to improved domestic gas production, Khizar cautioned that “Pakistan still requires 3-4 cargoes monthly”.

“If we don’t get these cargoes, our growth will be impacted,” he said.

On the external inflows side, risks are also building. Khizar warned that a prolonged conflict in the Middle East could reduce remittances by 15–20%, as economic uncertainty affects overseas Pakistani workers.

Experts warn that if the conflict affects expatriate employment, particularly in Saudi Arabia and the UAE, which account for a large share of inflows, remittances would be impacted.

According to State Bank of Pakistan (SBP) data, workers’ remittances totalled $3.3 billion in February 2026. Cumulatively, remittances reached $26.5 billion during the July–February fiscal year 2026.

Highlighting the policy trade-offs, Khizar said Pakistan’s reliance on the International Monetary Fund programme remains critical, adding that meeting its conditions may require currency depreciation and higher interest rates to stabilise the external account.

Echoing similar concerns, Saad Hanif, head of research at Ismail Iqbal Securities, said petroleum imports account for roughly one-fourth of Pakistan’s total import bill, highlighting the economy’s sensitivity to oil price movements.

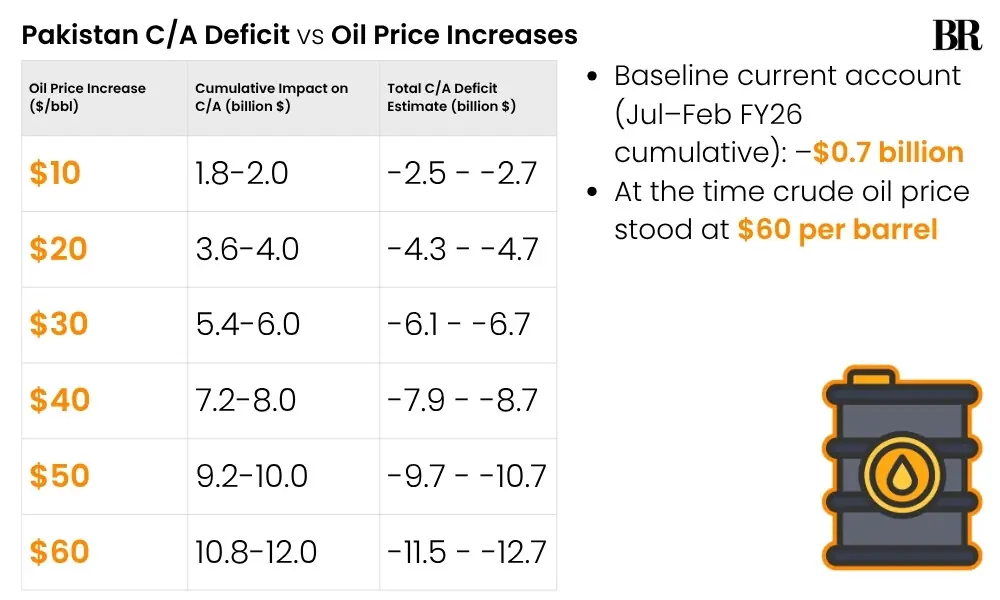

“With oil already above $100 per barrel, the pressure on the current account has effectively materialised,” Hanif said, noting that while prices around $60 per barrel are manageable, the current surge significantly weakens the external balance.

“Based on established sensitivities, every $10 per barrel increase in oil prices widens Pakistan’s current account deficit by approximately $1.8–2 billion annually, implying a cumulative impact of nearly $5-6 billion at current levels.

“This significantly elevates Pakistan’s external financing requirement, particularly if higher prices persist alongside elevated freight and supply chain disruptions stemming from the conflict.”

Pakistan recorded a current account surplus of $427 million in February 2026.

However, on a cumulative basis, the country posted a current account deficit of $700 million during Jul-Feb FY26.

Hanif also highlighted that remittances may not provide the same cushion this time.

“Given that a large share of Pakistan’s workforce is based in the Middle East, a prolonged conflict could disrupt labour markets, delay payments, or slow new hiring, thereby tempering remittance inflows over time.

“This reduces the effectiveness of remittances as a buffer compared to past oil price cycles,” he said.

To a query, Hanif stated that although IMF inflows and support from other multilaterals can provide short-term liquidity and help stabilise reserves, “they primarily address financing needs rather than offset the structural imbalance”.

Meanwhile, Fitch Ratings has flagged broader regional risks, noting that Asia-Pacific economies, including Pakistan, face heightened downside pressures from a prolonged conflict.

“Large net fossil-fuel importers, such as India, South Korea, Pakistan, the Philippines, the Maldives and Thailand, would face the sharpest deterioration in external balances and real incomes if energy prices rise and shipping disruptions persist,” the rating agency noted in its latest report.

As per the rating agency, nearly 90% of Pakistan’s oil imports come from the Middle East, while the country has less than 30 days of oil reserve coverage, both strategic and commercial.

With geopolitical tensions showing little sign of easing, economists warn that Pakistan’s current account outlook could deteriorate rapidly.

“As such, in a scenario of sustained geopolitical tensions and elevated oil prices, Pakistan’s current account is likely to remain under pressure, with both key supports, remittances and external financing facing a more uncertain outlook than usual,” said Hanif.

Comments