The ongoing and evolving crisis in the Gulf region presents significant implications for Pakistan’s economy, owing to its profound economic linkages with the area.

Two pivotal vectors through which Pakistan may be impacted are crude oil imports and remittances from overseas Pakistanis. Consequently, any geopolitical escalation in the region could influence global oil prices and disrupt labour markets in the host countries, thereby exerting dual pressures on Pakistan’s balance of payments (BoP) situation.

Amidst the Gulf crisis, Pakistan absorbed the crude oil price shock, despite the Minister of Energy stated that we have a stock sufficient for at least 25 to 30 days; hence, this price increase is inconceivable. Yet the Pakistani government increased petrol and diesel prices by 21 percent and 19.6 percent, respectively, a move expected to push CPI inflation for the current month by over 8 percent (petrol’s impact 3.12 percent and diesel’s 5.8 percent).

The decision has caused significant public outrage and created uncertainty. It is unclear whether this decision is intended to provide windfall profits to petrol dealers, and if so, why? Interestingly, the government also raised the petroleum levy on petrol by PKR 21 per liter while a similar amount was reduced for diesel, despite petrol’s consumption being higher by approximately 8.5 million liters per day. This move could further fuel inflationary pressures on people already facing hardships while generating an additional PKR 15 billion in revenue for the national tax revenue in the next four months.

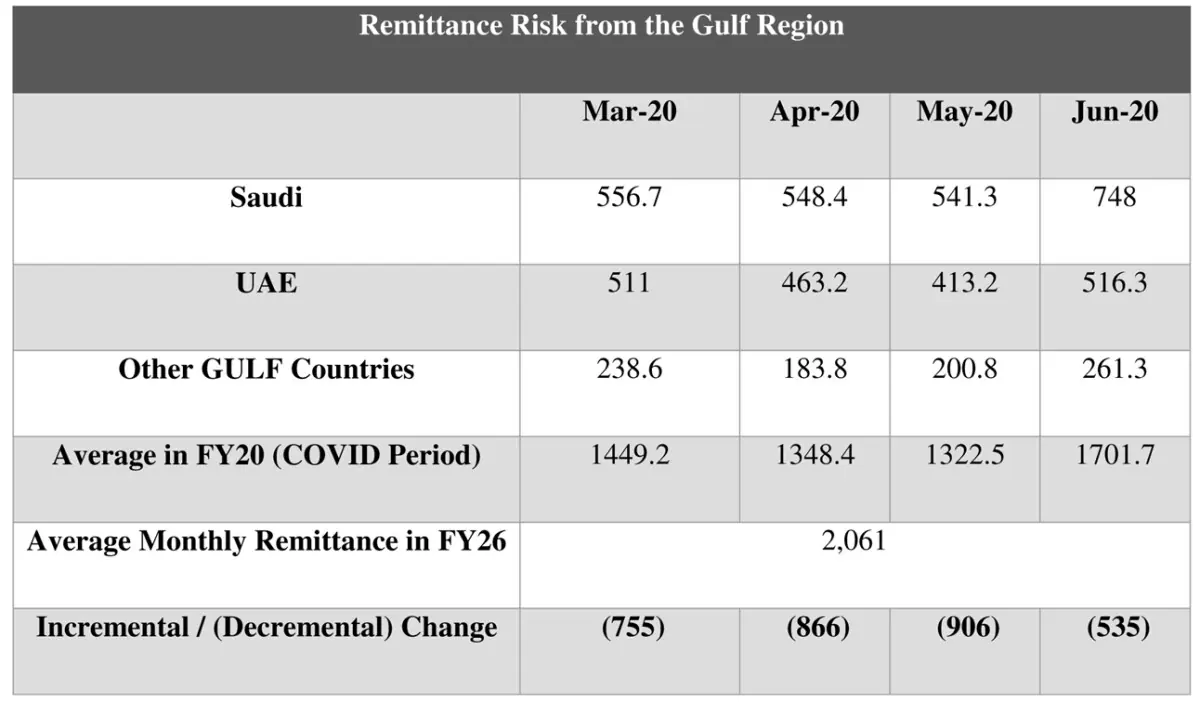

Remittances from the Gulf region. The table below compares the remittance levels observed during the Covid stress period with the current average monthly inflows of approximately USD 2.06 billion in FY26. Should similar external shocks occur due to geopolitical instability in the Gulf region, Pakistan could encounter a potential decline in remittances, ranging from USD 535 million to USD 906 million per month.

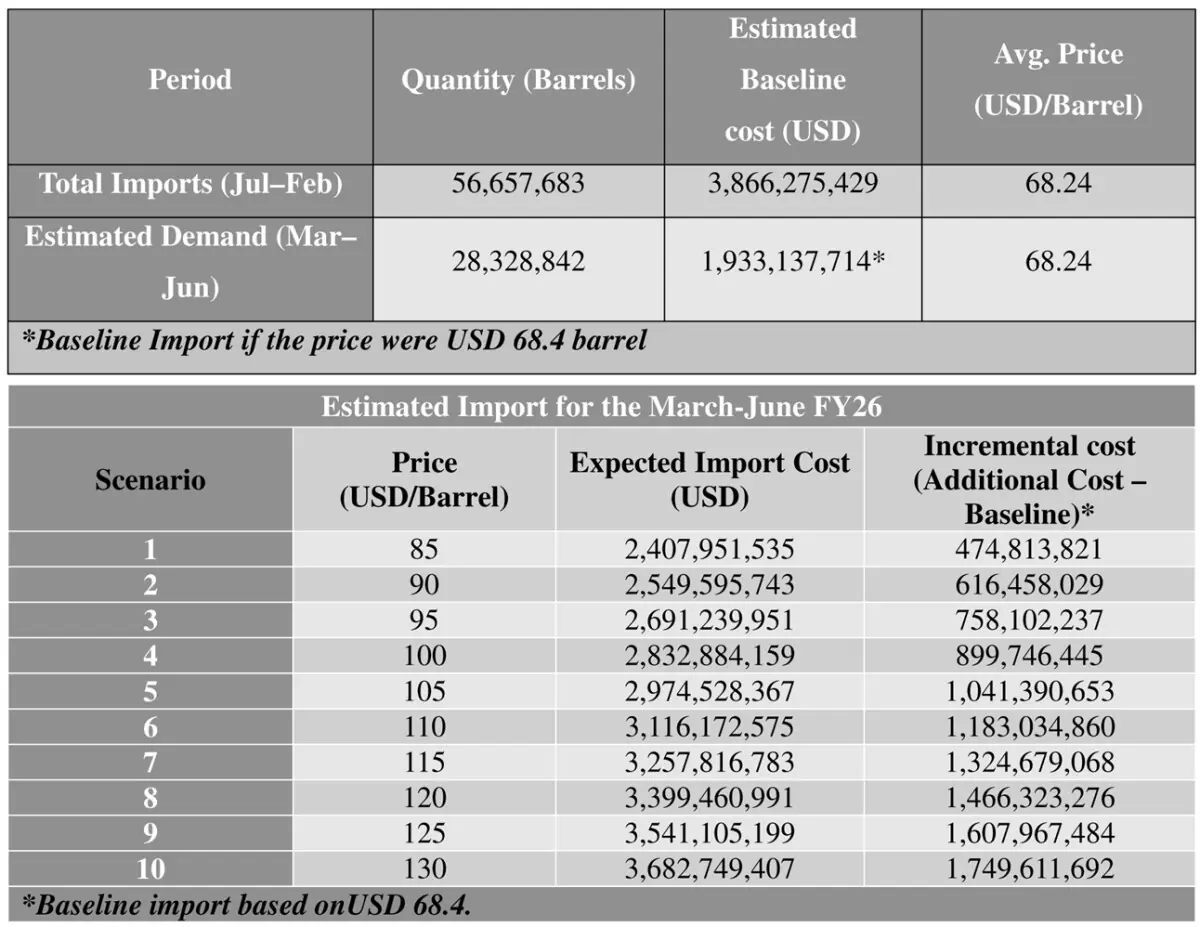

Additionally, Pakistan’s crude oil import bill demonstrates high sensitivity to fluctuations in global oil prices. Based on the projected demand of 28.3 million barrels for March through June, even moderate increases in prices can substantially elevate the import bill.

The chart below shows the possible scenarios:

If oil prices escalate to between USD 85 and USD 130 per barrel, Pakistan may face an additional external financing requirement of between USD 0.5 billion and USD 1.7 billion within the remaining four months of FY26.

Moreover, Pakistan could face double-digit inflation due to the rise in crude prices, driven by both the direct and indirect effects of higher domestic fuel prices. Historically, shocks of this nature have prompted Pakistan to seek emergency programs with the International Monetary Fund (IMF).

For decades, Pakistan’s economic stabilization strategy has primarily depended on periodic assistance from the IMF, often viewing IMF programmes as the default remedy during Balance of Payments (BOP) crises. Nonetheless, a sustainable and sovereign economic future underscores the need for formulating a credible “Plan B” by the government.

In the Budget for 2022–23, an amendment was introduced to Section 111(4) of the Income Tax Ordinance, whereby foreign exchange remitted into Pakistan up to PKR 5 million per tax year is not classified as unexplained income. This threshold could be substantially increased—potentially up to USD 100,000—to promote domestic investment, while safeguarding against terror financing, money laundering, and other illicit activities. Such a measure could have represented a significant breakthrough for Pakistan. However, following the presentation of the Finance Bill, the government entered into a short-term arrangement with the IMF and was compelled to withdraw the proposed amendment.

On average, Pakistan requires approximately USD 28 billion annually, with USD 16 billion derived from rollover financing. The remaining USD 12 billion comprises bilateral inflows and the current account deficit (CAD). The concept of a ‘game changer,’ representing Pakistan’s well-considered and deliberated ‘Plan B,” was rooted in this context. According to data on remittances from 2020 to 2022, approximately PKR 1.2 trillion (USD 4.2 billion) was remitted by roughly 350,000 to 450,000 individuals, averaging about PKR 3 million per person. This figure significantly exceeds the permissible limit of PKR 5 million.

If the government permits remittances of up to USD 100,000 per individual, it could potentially generate an additional USD 60,000 per person. Assuming approximately 400,000 individuals remit funds, this could culminate in around USD 24 billion. Consequently, the government could realistically mobilize an extra USD 15–20 billion, thereby enabling Pakistan to meet its external financing needs and service foreign currency debt obligations. This would constitute the effective implementation of Plan B, offering Pakistan an avenue to disengage from IMF dependence. Unfortunately, a few individuals disrupted this initiative under the misconception that Pakistan might default.

In the absence of an IMF programme, a critical concern is the stagnation of export growth. An analysis of ten years of data indicates that Pakistan’s exports have exhibited structural stagnation, remaining within a narrow band, thus lacking sustained growth. Although exports peaked in FY22 with an amount of USD 32.5 billion, the average exchange rate was PKR 177/USD. In 2024, exports were recorded at USD 32.4 billion, with an average rate of PKR 274/USD. This suggests that devaluation has not positively impacted export performance. The subdued export response to currency depreciation reflects deeper supply-side limitations and a lack of diversification.

Further analysis reveals that for every USD 100 of exports, Pakistan imports nearly 70 percent of the necessary inputs. Exporters typically retain 10 percent of export value in accounts abroad to cover marketing and related expenses. There are serious concerns regarding these transactions, with some possibly involving themselves in back-to-back (“me-to-me”) buying and selling. Moreover, issues of under-invoicing of exports and over-invoicing of imports persist, and the full extent of these practices remains largely unknown. As a result, net export yields are approximately 15 percent, an alarmingly low figure. Pakistan should consider adopting the Bangladesh model, wherein 20 percent of export value addition is retained in a domestic account, with transactions subject to governmental audit to evaluate performance.

Exporters should be supported on a value-added basis. For instance, if an exporter imports 70 percent of inputs and generates only 30 percent domestic value addition, incentives should be limited to 10–20 percent of that value addition, ensuring that proceeds remain within Pakistan and expenditures are incurred domestically. “Me-to-me” imports and exports should be prohibited, with strict enforcement that beneficial owners are distinct entities and not linked through tax-haven structures.

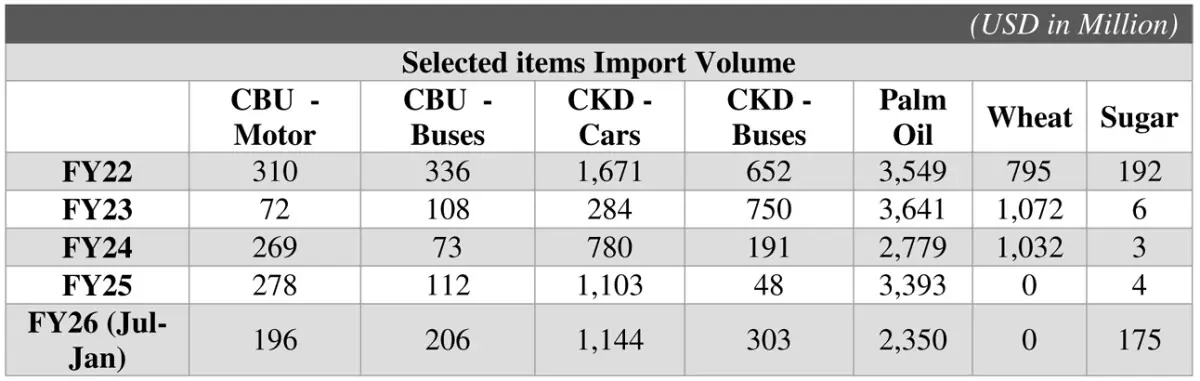

Imports, meanwhile, continue to grow sharply, largely driven by luxury items such as automobiles. Despite declines in global palm oil and fuel prices, Pakistan’s import bill has continued to rise this year (evident from car and luxury import data).

The data for FY26 in the span of seven months is already meeting the pace of FY22, which eventually hit a high cumulative current account deficit (CAD). This approach is unsustainable. Imports must be strictly regulated and limited to essential items only for at least five years in order to curb unnecessary outflows, contain the import bill, and ease pressure on the CAD.

Moreover, the key limitation of IMF-led stabilization programme is its impact on the exchange rate and interest rates. The PKR/USD rate is currently around 280, whereas its fair market value is closer to 253 per USD. Despite the global decline in the value of the US dollar, the rupee has remained artificially weak. As a result, interest rates remain elevated, which in turn worsens the fiscal deficit and inflation. Inflation, which could have been near 0–1 percent, averaged around 5.5 percent during July to February of FY26.

If the exchange rate were aligned closer to its fair value of PKR 253/USD, a PKR 30 rupee appreciation could reduce inflation by approximately 6 percent (based on the relationship that a PKR 10 appreciation lowers CPI inflation by about 2 percent). This would allow a 4-5 percentage point reduction in interest rates, creating fiscal space. A 1 percent reduction in the fiscal deficit could generate approximately PKR 550 billion in domestic debt-servicing relief. Moreover, lower borrowing costs would support industrial growth, particularly in export-oriented sectors.

Furthermore, the freelancing and information technology services sector necessitates precise valuation. Pakistan ranks among the world’s leading freelancing hubs; however, the actual value of foreign contracts executed within the country remains unmeasured. In numerous instances, work valued at USD 100 is subcontracted to Pakistani entities for USD 20, while the remaining USD 80 is retained abroad, resulting in considerable foreign exchange losses. The total value of such offshore retention must be formally appraised and documented.

Even in the absence of IMF support, Pakistan possesses alternative pathways. Through digital banking and the automated exchange of information, the country can accurately assess the real foreign assets of Pakistani nationals, particularly in countries such as the United States, the United Kingdom, the United Arab Emirates, Saudi Arabia, and Turkey, ensuring their proper disclosure to domestic tax authorities.

Therefore, reliance on the IMF can be phased out while concurrently strengthening foreign exchange reserves, enhancing exports, and significantly improving economic transparency and policy credibility. If these measures are implemented effectively, Pakistan can achieve exit from the IMF programmes.

Copyright Business Recorder, 2026

Comments