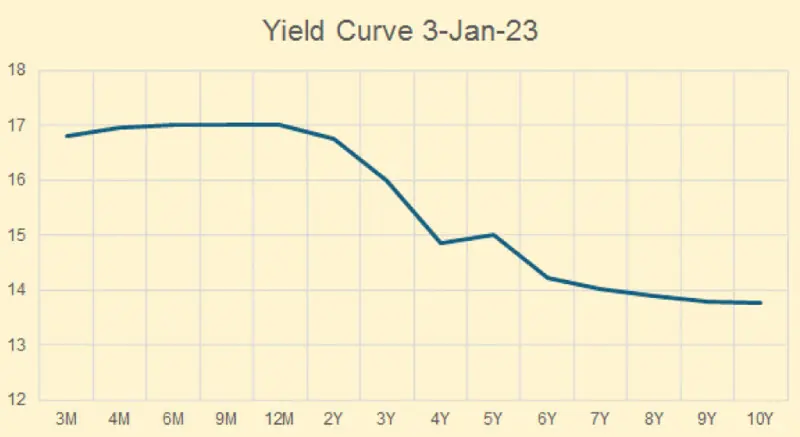

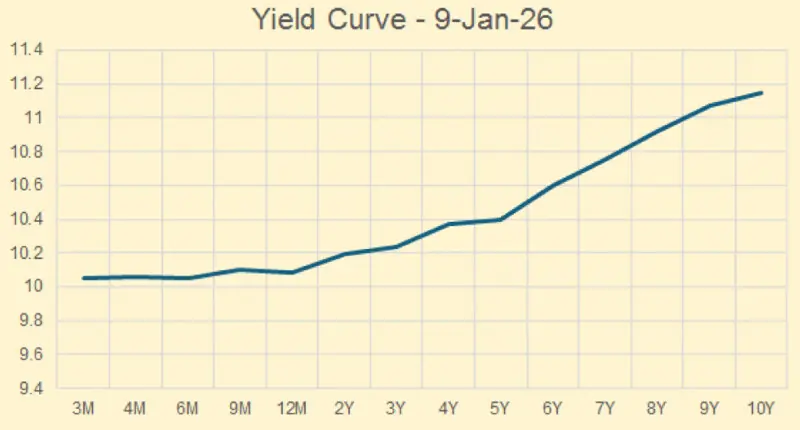

With economic recovery and declining interest rates, the yield curve is becoming smoother and upward sloping — from completely inverted in 2023 to flattened in 2024–25, and now turning upward sloping, as it ideally should be.

Moreover, secondary market yields are falling, as the market is expecting a 50–100 bps decline in the key policy rate.

The buzz is that rates could move into single digits in FY26, and given subdued inflation and calm in the currency market, the chances of having single-digit rates in this fiscal year are becoming high. The current policy rate stands at 10.5 percent.

Three-month to one-year T-bills are now ranging between 10.05 and 10.08 percent in the secondary market, as a 50 bps cut is largely priced in.

In the last auction (conducted on 7 January 2026), the 3M to 1Y cut-off rates ranged between 10.15 and 10.16 percent, and the highest participation (Rs1,375 billion out of Rs2,555 billion) was in the 12M tenor.

The highest acceptance was also in the 12M paper (Rs761 billion out of Rs979 billion). Rates were down by 0.32–0.34 percent compared to the previous auction.

Since then, rates have come down further to 10.05–10.08 percent. The market demanded 12M paper, reflecting expectations of rates falling further in the coming months. The government also accepted higher amounts in the 12M tenor, effectively locking in higher returns for banks at a time when interest rates are declining.

Another notable observation is the steep fall in the spread of PIB floaters over the past year. PIB floaters are linked to market rates, with bids reflecting the premium over the linked rate (i.e., weighted average spreads). The spread ranged between 1.28 percent and 1.45 percent during October 2024 to March 2025 on 10-year floaters, during which the government issued a massive Rs5.9 trillion in 10-year paper at very high spreads.

In the latest auction, the spread has reduced to 0.47 percent. This is a significant relief for the government. However, it also indicates that some banks made substantial profits on the higher spreads earlier, as the government was pushed by the IMF to undertake higher long-term issuance.

Banks that locked in these higher spreads will continue to enjoy the premium for the next 10 years. This is one of the reasons some banks have posted extraordinary profits and why their stock prices are breaking records. Anyhow, that is a side note.

The main story remains falling T-bill rates, rising expectations of the policy rate moving into single digits, and shrinking spreads on PIB floaters. Together, these trends are likely to ease the government’s debt servicing burden and may create some fiscal space to marginally lower tax rates next year.

Comments

Comments are closed for this article.