Historically, the country has been dogged by two intractable problems: civil-military imbalance and unfair distribution of resources between the federation and provinces. The former has bedevilled democracy, the latter federalism. Yet, no lessons have been learnt from this odyssey of failures. With the induction of the new government, a vociferous campaign has ensued in official circles and the media to review the seventh National Finance Commission (NFC) award — It’s not the NFC Award, Shahab Usto, Dawn, April 6, 2024

The National Finance Commission (NFC) Award has always been central to Pakistan’s federal structure, reflecting the delicate balance of responsibilities, rights, and resources among the federation and its constituent units as envisaged under Article 160 of the Constitution of Islamic Republic of Pakistan [“the Constitution”]. It is unfortunate that in 2025 we kept on following Seventh NFC Award notified on May 10, 2010! Hopefully, 2026 will bring a new NFC award.

All earlier articles contributed by these scribes covering various facets of NFC consistently emphasized that distribution must be fair, evidence-based, and aligned strictly with constitutional principles to sustain the federation.

As Pakistan now enters the critical phase of parleys under the 11th NFC—formally notified on August 22, 2025 by the President of Pakistan after the expiry of 10th NFC on July 21, 2024—this is an opportune moment to revisit earlier arguments and update them in light of new fiscal realities.

What is new in the 11th NFC?

The notification and inaugural meeting of 11th NFC marks an important milestone after the dissolution of the 10th, 9th and 8th NFCs without proposing any award.

The inaugural meeting of 11th NFC on December 4, 2025—headed by the Federal Finance Minister Muhammad Aurangzeb—established multiple thematic working groups mandated to examine broader needs than population alone.

For the first time, there was a structured conversation on:

(i) integrating the economic needs of the merged tribal districts into the national fiscal framework;

(ii) addressing long-standing grievances of underfunded provinces; and

(iii) reconsidering the outdated formula that overwhelmingly emphasizes population rather than needs, deprivation, backwardness, or fiscal effort.

The last one, indeed, represents a promising shift from earlier NFC cycles where the debate remained restricted to one or two variables and overemphasis on population.

On December 15, 2025, according to a Press report, the Federal Government notified eight committees that “will shape the 11th NFC award”. The report further revealed: “A working group, headed by Punjab’s finance minister, was also constituted to make recommendations on sharing financial expenses incurred by the federation in areas under provincial jurisdiction”.

The group’s formation, as per report, followed a legal opinion from the Attorney General for Pakistan, in the wake of an objection from Sindh “arguing that expenditure-sharing falls outside the NFC’s mandate”. The report quoting some sources informed, “Sindh may seek its own legal opinion as the federal government continues spending in areas under provincial control”.

It is further reported that according to Dr. Asad Sayeed, Sindh’s technical member on the NFC, “the federal government retains ministries linked to devolved subjects and spent Rs. 328 billion on them, as highlighted in a 2023 World Bank report”.

Most crucial question remains untouched

The most crucial point, however, remains untouched/undebated. It is why the provinces remain heavily dependent on the NFC transfers in the wake of Constitution (Eighteenth Amendment) Act, 2010, [18th Amendment], became effective on April 19, 2010, only 20 days before 7th NFC Award.

No committee is formed/notified under 11th NFC to examine this vital question and impact of 18th Amendment causing a paradigm shift in Pakistan’s fiscal and administrative architecture.

With principal objective of granting greater autonomy to provinces by devolving critical functions, the 18th Amendment substantially transformed federal-provincial relationship, with re-sharing of taxation powers conforming to fiscal federalism and decentralized governance model.

However, even after a lapse of more than 15 years, the provinces have failed to introduce progressive taxes, transferred from the centre to them through the 18th Amendment.

The provinces have also miserably failed to implement Article 140A(1) of the Constitution to “devolve political, administrative and financial responsibility and authority to the elected representatives of the local governments”.

One of the many maladies in Pakistan’s tax system is cumbersome withholding tax system contained in the Income Tax Ordinance, 2001, Sales Tax Act, 1990 and all provincial laws relating to sales tax on services.

This kind of irrational system of withholding of tax at source is operationally inefficient, anti-business, complex, time-consuming and costly. The withholding tax regime must be abolished, except for payroll, dividends, interest income from banks, and taxable payments to non-residents.

The implementation of agenda of simplification of tax codes and rationalization of tax system can improve tax compliance. Provided this agenda is also accompanied by substantial improvement in public perception regarding the efficiency, technical competence, integrity and ability of the tax authorities to collect taxes fairly and justly, using modern technological tools.

The present weak and fragmented structures of the federal and provincial tax agencies have failed to achieve these objectives.

Therefore, the fundamental challenge is providing a simple tax but efficient system that is manned by a competent, proficient and service-oriented administration, which is presently non-existent.

Tax administrations, both at federal and provincial levels are outdated and outmoded, besides suffering from inefficiencies, lack of trained manpower and requisite infrastructure and facilities.

The absence of requisite level of digitization, professionalism and human skills is their major malady. Tax reforms certainly do not mean mere alteration of tax laws or just making cosmetic changes. There is no effort till today to first restructure the entire tax administration on modern lines.

The failure to tap real tax potential of Rs. 34 trillion is the real dilemma of both the federal and provincial governments and not the mere NFC Award. Poor performance of Federal Board of Revenue (FBR) adversely affects provinces as they are overwhelmingly dependent on the transfers under the NFC Award—commonly called Divisible Pool. Provinces are not ready to collect taxes wherever due e.g. agricultural income tax from rich absentee landowners and rationalized property tax from occupant of palatial houses/bungalows/farm houses etc.

Structural causes of fiscal imbalances

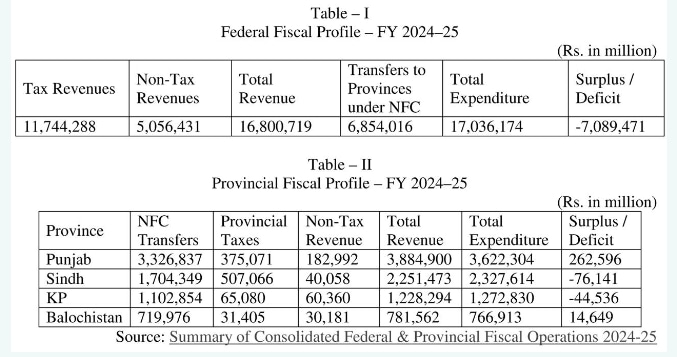

To illustrate the present structural imbalance in Pakistan’s fiscal federalism, below is a summary of federal and provincial revenues and expenditures for fiscal year (FY) 2025:

Look at the figures contained in Table I and Table II. How little provinces collect in taxes at their own and the quantum of fiscal deficit suffered by the federation due to the small size of cake (overall national resource mobilization versus monstrous expenditures)! While the federal government is accumulating unmanageable debts, the provinces, heavily dependent on transfers under NFC Award, are engaged in unproductive spending spree.

What makes the situation more disturbing is the fact that right of provinces to levy sales tax on services is encroached by federal government through levy of presumptive/minimum taxes on services under the Income Tax Ordinance, 2001, sales tax on gas, electricity and telephone services and excise duty on a number of services. In 2025, the provinces also encroached upon the right of Parliament by imposing sales tax on rent!

The federal government after imposing all kinds of oppressive taxes has miserably failed to reduce the burgeoning fiscal deficit. The reason being that FBR has been persistently failing to achieve the assigned targets, what to speak of tapping the actual tax potential that at federal level is not less than Rs. 30 trillion and Rs. 4 trillion at provincial levels.

[To be concluded]

Copyright Business Recorder, 2025

The writer is a lawyer and author, is an Adjunct Faculty at Lahore University of Management Sciences (LUMS), member Advisory Board and Senior Visiting Fellow of Pakistan Institute of Development Economics (PIDE)

The writer, an Advocate Supreme Court, Adjunct Faculty at Lahore University of Management Sciences (LUMS), member Advisory Board and Visiting Senior Fellow of Pakistan Institute of Development Economics (PIDE), holds LLD in tax laws

The writer is a corporate lawyer based in the US with extensive expertise in financial regulations, including Virtual Asset Service Providers (VASPs), corporate governance, and global economic policies. He holds an LLM from Washington University in St. Louis and has completed the Management Development Program at the Wharton School. He has developed regulatory frameworks for North American and South American Financial Institutions and has consulted and trained bureaucrats of different regions. He can be reached at [email protected]

Comments

Comments are closed for this article.