Pak Leather Crafts Limited (PSX: PAKL) is incorporated in Pakistan as a public limited company. It was established in 1971. The company is engaged in leather tanning, manufacturing of leather garments as well as export of leather and leather garments.

Pattern of Shareholding

As of June 30, 2025, PAKL has a total of 3.4 million shares outstanding which are held by 599 shareholders. Sponsors’ associates & friends have the majority stake of 43.08 percent in the company followed by directors, their spouse and minor children holding 36.18 percent shares of PAKL. Other individuals account for 18.14 percent shares of the company while financial institutions and joint stock companies collectively hold 2.55 percent shares. The remaining 0.05 percent shares are held by Investment Corporation of Pakistan.

Historical Performance (2019-25)

PAKL’s topline grew considerably in 2019 and 2020 followed by a slump in 2021. It then recovered in the subsequent year followed by a descent thereafter. The company posted net loss in 2021, 2022 and 2023. In all the years under consideration, PAKL posted negative equity because of hefty accumulated losses. This was due to the fact that the company has consistently been registering net losses since 2014. PAKL’s liabilities are quite higher than its total assets.

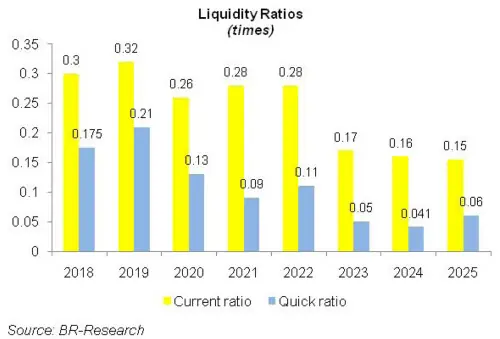

Exorbitant level of current liabilities also translates into negative working capital in all the years under consideration. PAKL’s margins registered a strong rebound in 2019. In 2020, gross margin slid; however, operating and net margins posted a staggering rise. 2021 witnessed a freefall of margins with operating and net margins striking the negative zone. In the subsequent two years, gross margin improved while operating and net margins continued to stay in the negative territory. In 2024 and 2025, PAKL’s margins posted phenomenal growth the detailed performance review of the period under consideration is given below.

In 2019, PAKL’s net sales grew by 48.16 percent year-on-year to clock in at Rs.76.58 million. Despite depressed macroeconomic backdrop characterized by high inflation, Pak Rupee depreciation, monetary tightening as well as regulatory measures, the company was able to push its bottomline into net profit after five uninterrupted years of net losses. While export sales slightly shrank in 2018, the topline growth was mainly the consequence of local income derived from leather processing. Cost of sales grew by 23.81 percent year-on-year in 2019 as the company achieved economies of scale because of higher volumes.

Gross profit magnified by 695 percent year-on-year in 2019 with GP margin jumping up from 3.63 percent in 2018 to 19.46 percent in 2019. Operating expense grew by 25.81 percent year-on-year in 2019 on account of higher payroll expense as the number of employees grew from 21 in 2018 to 40 in 2019. Fee and subscription charges and balances written off also escalated in 2019. PAKL registered operating profit of Rs.5.86 million in 2019 versus operating loss of Rs.4.13 million recorded in 2018. OP margin was recorded at 7.65 percent in 2019. The company had a total debt of around Rs.250 million as of June 30, 2019 out of which Rs.12.99 million was long-term and interest free, acquired from directors’ associates. The remaining short-term loan had mark-up over due for which the banks had filed suit for recovery.

PAKL only paid bank commissions which grew by 24.72 percent in 2019. PAKL posted net profit of Rs.4.146 million in 2019 as against the net loss of Rs.5.29 million recorded in 2018. EPS clocked in at Rs.1.22 in 2019 versus loss per share of Rs.1.56 posted in 2018. NP margin stood at 5.41 percent in 2019.

PAKL’s topline boasted a tremendous 182.88 percent year-on-year rise to clock in at Rs.216.63 million in 2020. This was because of a splendid 5 times growth in export sales. PAKL achieved huge orders from Hong Kong, Cambodia, China, Indonesia and South Korea which gave a significant boost to its export sales in 2020. Conversely, local sales slid by 64 percent in 2020. Substantial rise in material cost on account of COVID-19 pushed the cost of sales up by 217 percent in 2020. Gross profit grew by 41.52 percent in 2020, however, GP margin drastically fell to 9.74 percent. Operating expense surged by a massive 724.66 percent in 2020 which was the consequence of higher provisioning booked for doubtful debts as well as elevated freight charges on account of COVID-19. Number of employees also rose to 48 in 2020 which pushed up the payroll expense during 2020. Other income grew by 13273.64 percent in 2020 as the company received waiver of Rs.79.89 million and Rs.34.83 million on loan liability and mark-up on loan respectively. This drove the operating profit up by 830.30 percent in 2020 with OP margin registering an overwhelming rise to clock in at 25.17 percent. Bank charges grew by 330.22 percent in 2020. Net profit surged by 1076.62 percent in 2020 to clock in at Rs.48.79 million with EPS of Rs.14.35 and NP margin of 22.52 percent.

The splendid topline growth recorded 2020 was followed by 49.98 percent decline in net sales which clocked in at Rs.108.36 million in 2021. While local sales showed some improvement during the year, the drastic fall of around 61 percent in export sales squeezed the topline in 2021. Thinner export sales were the result of lockdown imposed in various export destinations of PAKL. Cost of sales plunged by 46.51 percent year-on-year in 2021. Gross profit slipped by 82.11 percent year-on-year in 2021 with GP margin marching down to 3.48 percent. Operating expense also nosedived by 79.55 percent year-on-year in 2021 as the company didn’t book any provisioning against doubtful debts and also because of lower freight charges because of lower export sales. Other income slumped by 94.35 percent year-on-year in 2021 due to high-base effect as the company got waivers on loan and mark-up in 2020. PAKL recorded operating loss of Rs.6.43 million in 2021. Bank charges tumbled by 55.89 percent year-on-year in 2021. As a consequence, PAKL posted net loss of Rs.8.70 million in 2021 with loss per share of Rs.2.56.

PAKL’s topline registered 22.68 percent year-on-year improvement to clock in at Rs.132.94 million in 2022. This was due to rise in both export and local sales during the year. Pak Rupee depreciation proved to be a blessing in disguise for the company and drove its gross profit up by 255.25 percent in 2022. GP margin also rose to 10.10 percent in 2022. Operating expense stood at almost the same level as of previous year as the company reduced its workforce to 40 employees and also because of lower freight charges. Other income nosedived by 58.80 percent year-on-year in 2022 due to lower balances written back during the year. PAKL’s operating loss slipped by 89.54 percent to clock in at Rs.0.67 million in 2022. Bank charges also narrowed down by 57.16 percent year-on-year in 2022, translating into 66.68 percent lower net loss to the tune of Rs.2.90 million incurred during the year. Loss per share was recorded at Rs.0.85 in 2022.

In 2023, PAKL’s topline sustained 31.78 percent erosion to clock in at Rs.90.69 million. This was the result of a plunge in both local and export sales during the year. The company couldn’t maintain its growth momentum due to exorbitant increase in the prices of materials which dejected the customers both locally and globally. Wet blue and chemical prices hiked by 25 percent and 50 percent respectively. Electricity prices also spiked during the year. Moreover, only 50 percent of the company’s gas requirement was met by the gas pipeline. The thin liquidity of the company and its inability to meet its financial obligations didn’t allow it to obtain more loans from external parties. Hence, it couldn’t afford to switch to LPG and purchase costlier raw materials to continue its operations. Due to lower sales volume, cost of sales also slid by 32.16 percent in 2023. Gross profit shrank by 28.40 percent year-on-year in 2023, however, GP margin slightly improved to clock in at 10.58 percent. Operating expense surged by 13.89 percent year-on-year in 2023 which was the consequence of higher freight charges on account of escalated prices of POL products. Legal & professional charges also spiked during the year. Operating loss magnified by 1294.79 percent in 2023 to clock in at Rs.9.37 million. Bank charges grew by 28.20 percent year-on-year in 2023 resulting in 286.45 percent higher net loss to the tune of Rs. 11.21 million incurred during the year. Loss per share was recorded at Rs.3.30 – the highest among all the years under consideration.

In 2024, PAKL recorded year-on-year topline slide of 1.43 percent. Net sales clocked in at Rs.89.40 million. This was on account of a decline in export sales due to global recession. Thinner export sales were partially substituted by an uptick in local revenue from leather processing. Cost of sales plummeted by 5.74 percent in 2024 due to lesser raw materials consumed owing to lower export volumes. This resulted in 34.95 percent progress in the company’s gross profit in 2024. GP margin also jumped up to 14.50 percent in 2024. Operating expense tumbled by 24.53 percent in 2024 predominantly because of lower freight & forwarding charges as well as travelling & conveyance charges incurred during the year. What gave a significant support to the company’s bottomline was a staggering 11457 percent growth in other income. This was on account of waiver of loan liability and mark-up on loan on settlement. PAKL recorded operating profit of Rs.11.73 million in 2024 with OP margin of 13.12 percent. This was against the operating loss of Rs.9.37 million recorded in 2023. Bank charges & commission slipped by 5.58 percent in 2024 owing to lesser bank transactions on account of weak export sales volume. After three years of posting net losses, PAKL was able to record net profit of Rs.8.126 million in 2024 with EPS of Rs.2.39 and NP margin of 9.1 percent.

In 2025, PAKL’s topline further deteriorated by 32.78 percent to clock in at Rs.60.09 million. Leather processing income in the home market posted a drastic decline of 77.06 percent to clock in at Rs.8.689 million in 2025. This was due to decline in the demand of leather products in Pakistan due to sustained period of high inflation which took its toll on the purchasing power of consumers. Global recession also wreaked havoc on the export sales of the company which nosedived by 7.60 percent to clock in at Rs.51.78 million in 2025. Cost of sales plunged by 39.65 percent in 2025 in line with streamlined operations due to lower demand. PAKL’s ability to have a greater proportion of export sales in its sales mix resulted in 7.77 percent uptick in its gross profit in 2025. GP margin attained its optimum level of 23.23 percent in 2025. Considerably lower freight charges due to thinner sales volume, no travelling charges and a massive drop in legal & professional charges and fee & subscription charges resulted in 7.84 percent downtick recorded in operating expense in 2025. Other income also dwindled by 29 percent in 2025 due to high-base effect as the company received waiver of loan liability and mark-up in the previous year. Operating profit diminished by 14.43 percent in 2025, however, OP margin jumped up to 16.70 percent. Bank charges & commission ticked up by 8.28 percent in 2025. PAK L didn’t pay any mark-up on its loan due to unwinding of related deferred income during the year. Tax adjustment of Rs.1.400 million for prior years resulted in 94.30 percent decline in tax expense for the year. This resulted in net profit of Rs.9.023 million in 2025. NP margin was recorded at 15 percent in 2025 while EPS stood at Rs.2.65.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, PAKL posted year-on-year decline of 64.81 percent in its topline which clocked in at Rs.6.55 million. The entire revenue recognized in 1QFY26 comprised of export sales and rebate as no local sales were made during the period. The production for export sales was also conducted on toll manufacturing basis instead of self manufacturing. This resulted in huge cost saving for the company because due to low capacity utilization, fixed cost couldn’t be absorbed efficiently resulting in weaker gross profit in 1QFY25. Gross profit thinned down by 21.47 percent in 1QFY26, however, GP margin greatly improved from 12.14 percent in 1QFY25 to 27 percent in 1QFY26. Operating expense mounted by 21.82 percent in 1QFY26. While selling & distribution expense was low due to petite sales volume, higher operating expense was the consequence of increased payroll expense, power & water charges as well as depreciation expense incurred during the period. PAKL recorded 120.10 percent escalation in its operating loss which clocked in at Rs.2.19 million in 1QFY26. Finance cost dipped by 66.97 percent in 1QFY26. Net loss surged by 56.46 percent to clock in at Rs.2.36 million in 1QFY26. This translated into loss per share of Rs.0.69 in 1QFY26 versus loss per share of Rs.0.44 recorded in 1QFY25.

Future Outlook

As at September 30, 2026, PAKL has negative equity of Rs. 321.715 million. Its current liabilities exceed its current assets by Rs.323.851 million. These conditions cast significant doubts on the ability of the company to continue as a going concern. The company has recently disposed off its plant & machinery and is also planning to rent out its office building to improve its liquidity conditions.

Besides internal concerns, the company is also facing demand destruction owing to shrunken pockets of local customers and the company’s inability to compete in the global market due to high cost of production particularly elevated energy cost in the home market. The company has recently shifted to toll manufacturing to reduce its cost and stay competitive in the export market. In the recent period discussed, the company solely relied on its exports sales, however, in the wake of the ongoing geo-political tensions including the war imposed on the Gaza strip and other Middle Eastern regions, the sustainability of the company’s exports can’t be guaranteed.

Comments

Comments are closed for this article.