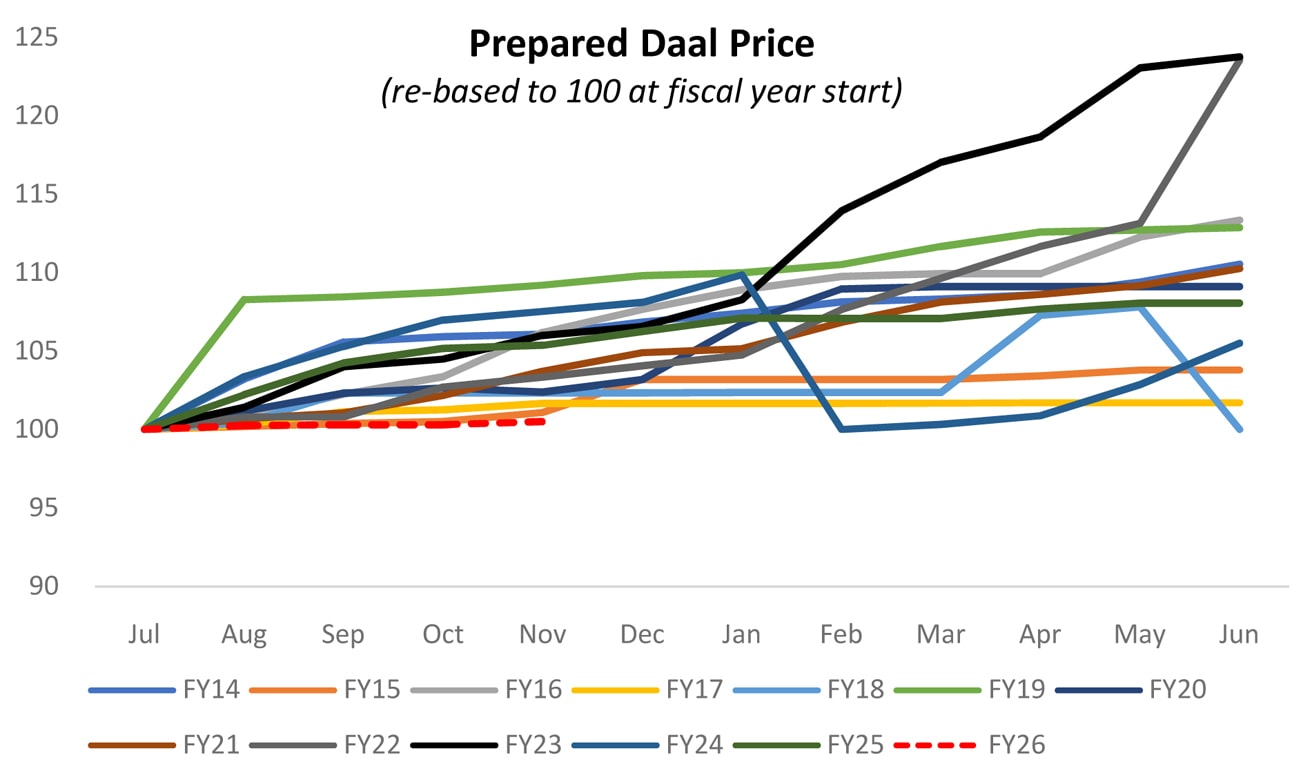

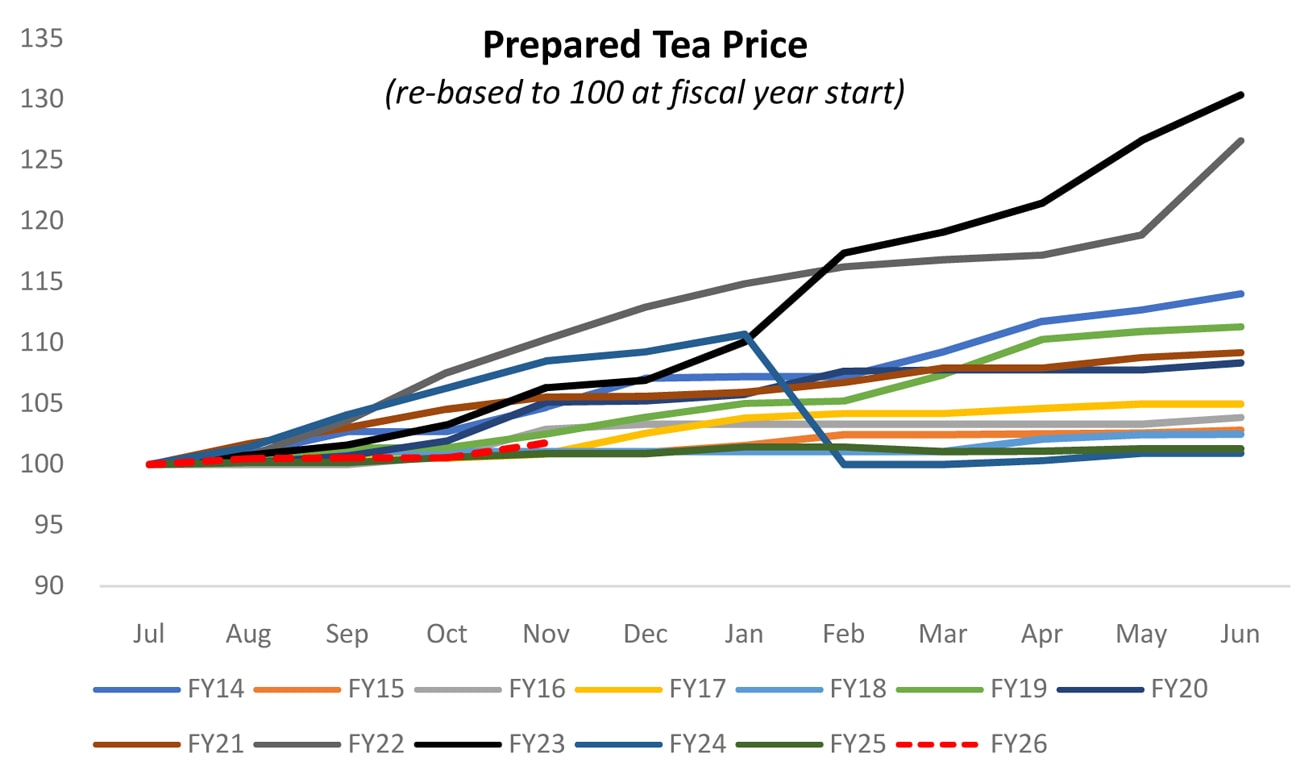

The latest round of price and wage trackers reinforces a familiar imbalance in the early months of FY26. Not all essentials are behaving the same way. Prepared daal and tea two items that normally show steady, almost mechanical monthly increases are rising at one of the slowest paces in more than a decade.

Left on their own these trends would suggest that the post inflation cool down is finally filtering into the kitchen economy.

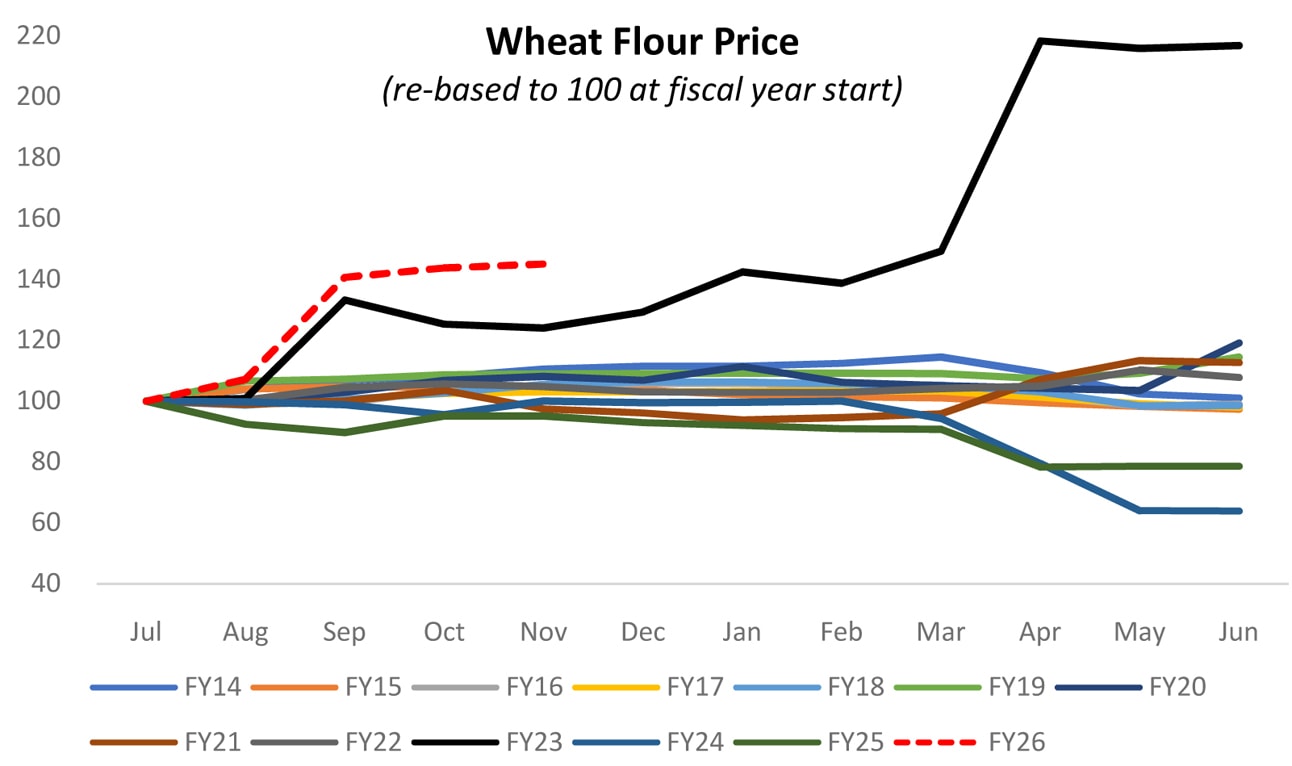

But comfort is misleading because the heaviest consumption item for low-incomehouseholds, wheat flour has surged to its highest level for any five-month period across the entire dataset. For the poorest quintiles where wheat flour constitutes a disproportionately large share of food expenditure, the early year trajectory already resembles the stress episodes of FY23.

This divergence matters because it punctures the notion that easing headline inflation has translated into broad relief for households.

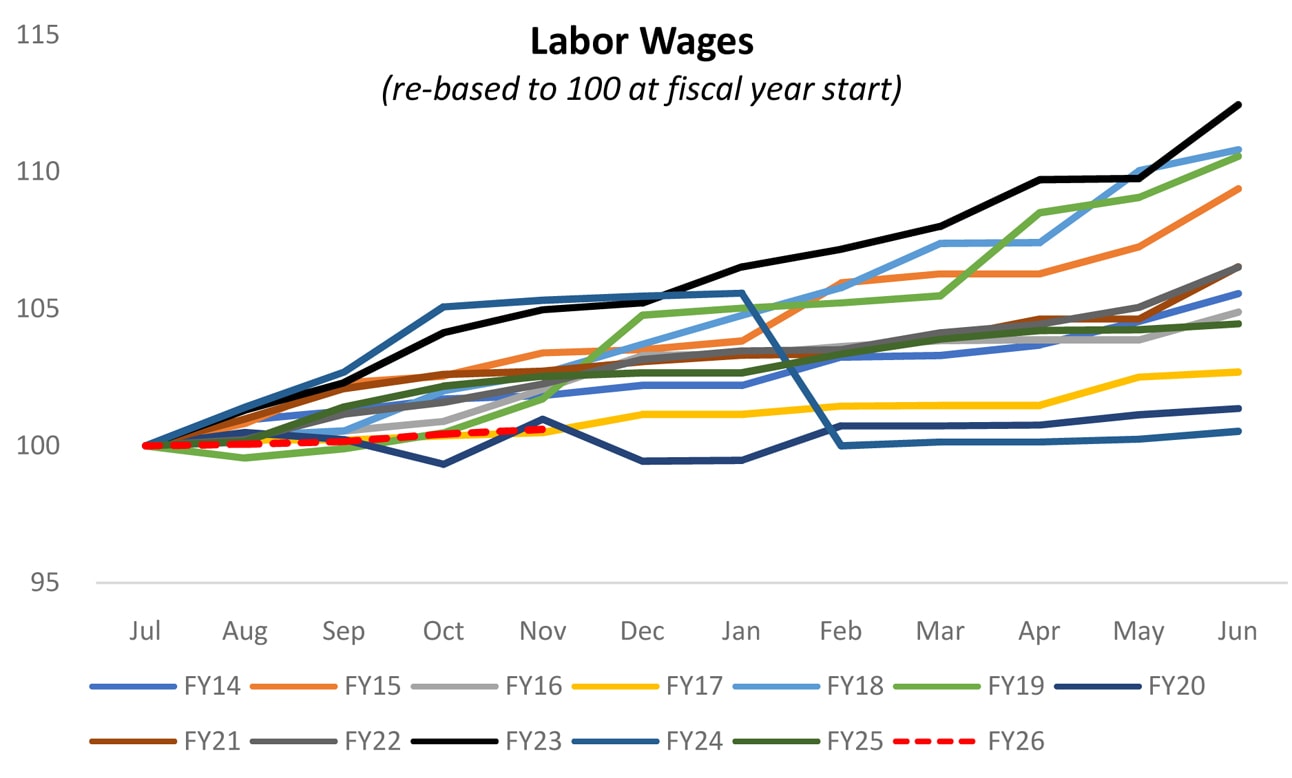

The income side of the picture is even weaker. Construction labor wages which serve as a real time proxy for informal labor demand show the slowest growth since FY17 and the second lowest in a twelve-year span by November. The industrial side does not offer an offset.

Wage growth in LSM has consistently lagged behind even the subdued construction wage cycle despite manufacturers claiming improved stability and better planning conditions. It points toward an economy that may be stabilizing on paper but is yet to translate that stability into stronger earnings for workers.

What stands out is how clearly the long shadow of FY23 still stretches across household balance sheets. That year’s inflation shock weakened real incomes to an extent that a single year of moderation was never going to repair.

The data suggests that recovery has been even slower than expected. Even with inflation at more manageable levels, construction workers are still experiencing negative real incomes. This is not simply a story of wages adjusting with a lag. It is a sign that pockets of the economy remain depressed with limited capacity to generate the wage momentum that usually accompanies stabilization phases.

The combined movement of these indicators underscores the uneven nature of relief. Daal and tea may be behaving, but wheat flour the anchor of food security for low-income households is not. Wage cycles remain anemic across both informal and industrial segments. The headline inflation dragon may have been tamed compared to the fire breathing months of FY23 and FY24 but for millions of households the everyday arithmetic of food and income still does not add up.

Comments

Comments are closed for this article.