It is that time of the year again. Cane crushing season is upon us, as marketing of new season’s refined sugar begins right about now. And rather than usual anxieties about shortage and speculation, it must open with recognition that the cycle has peaked and that the next phase must be one of correction.

The data already says so. The international market confirms it. And domestic financing leaves little space for anything else.

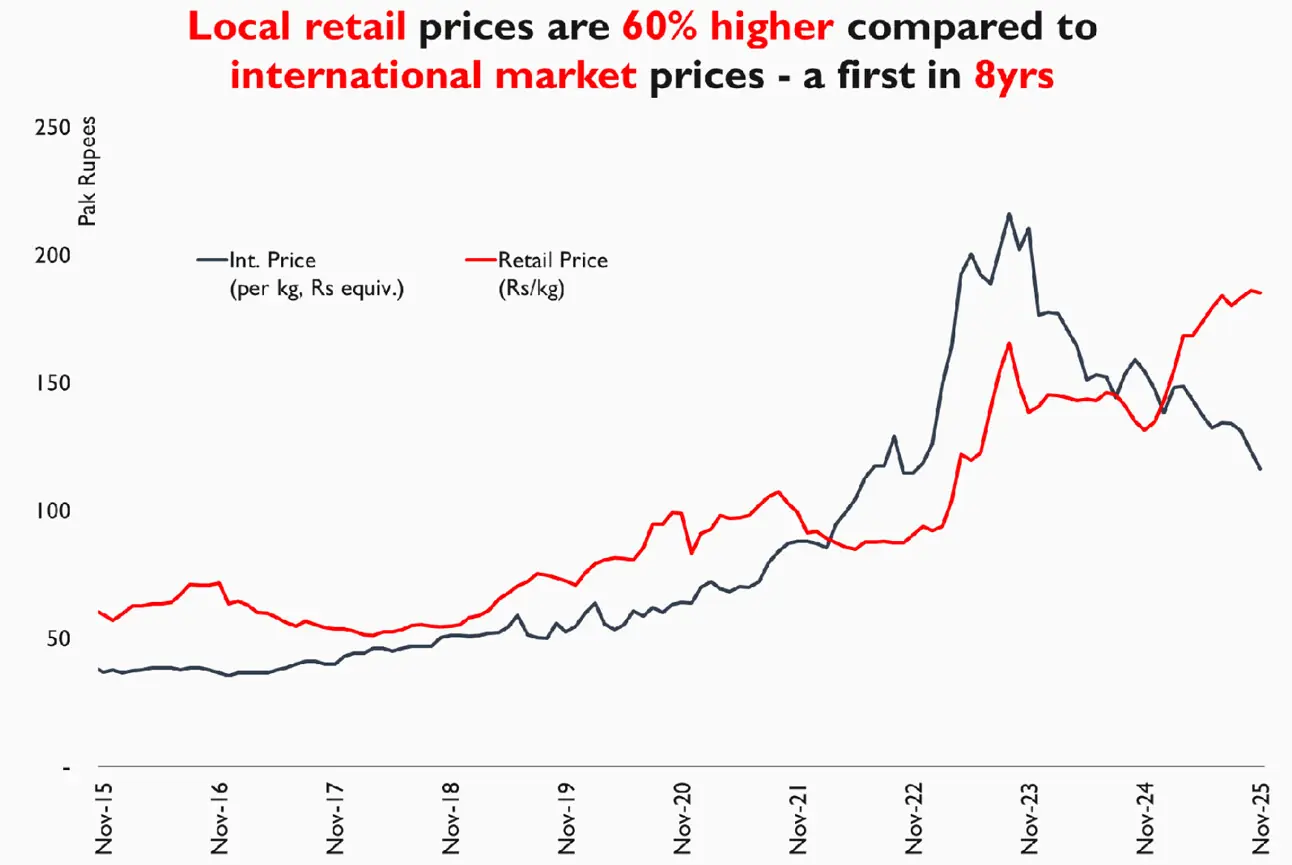

World prices have fallen to a five-year low. From a peak of near$750MT exactly two years ago, they are now flirting to fall below $400MT, a level last witnessed during pandemic lockdowns.This is not a small adjustment; instead, a reset. In any functioning commodity market that kind of decline would prompt domestic alignment, irrespective of tariffs and barriers to free trade.

In Pakistan, the transmission is always slower than it should be, but it can only be delayed so long. The just-ending season was carried on the back of thin carry-forward stock,insipid bank borrowing, and retail prices soaring on rumor and information asymmetry.

Those supports are now eroding, and the upcoming season must not rely on them. In fact,given the lax financing capacity available to mills, it should actively discourage any attempt to hold stock or squeeze margins.

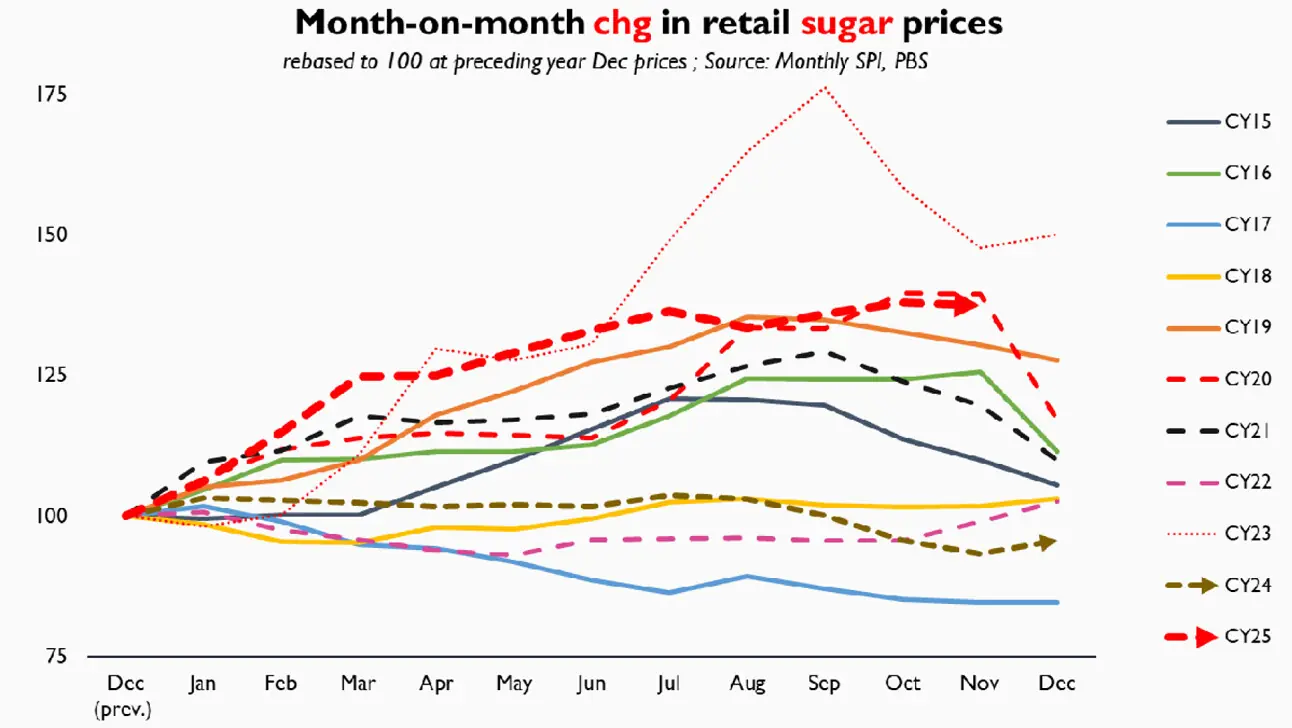

The year that has just closed could hardly be described as a normal sugar cycle. Retail prices did not fall when global prices softened. They held steady through most of the season because inventories were thin and liquidity was tight.

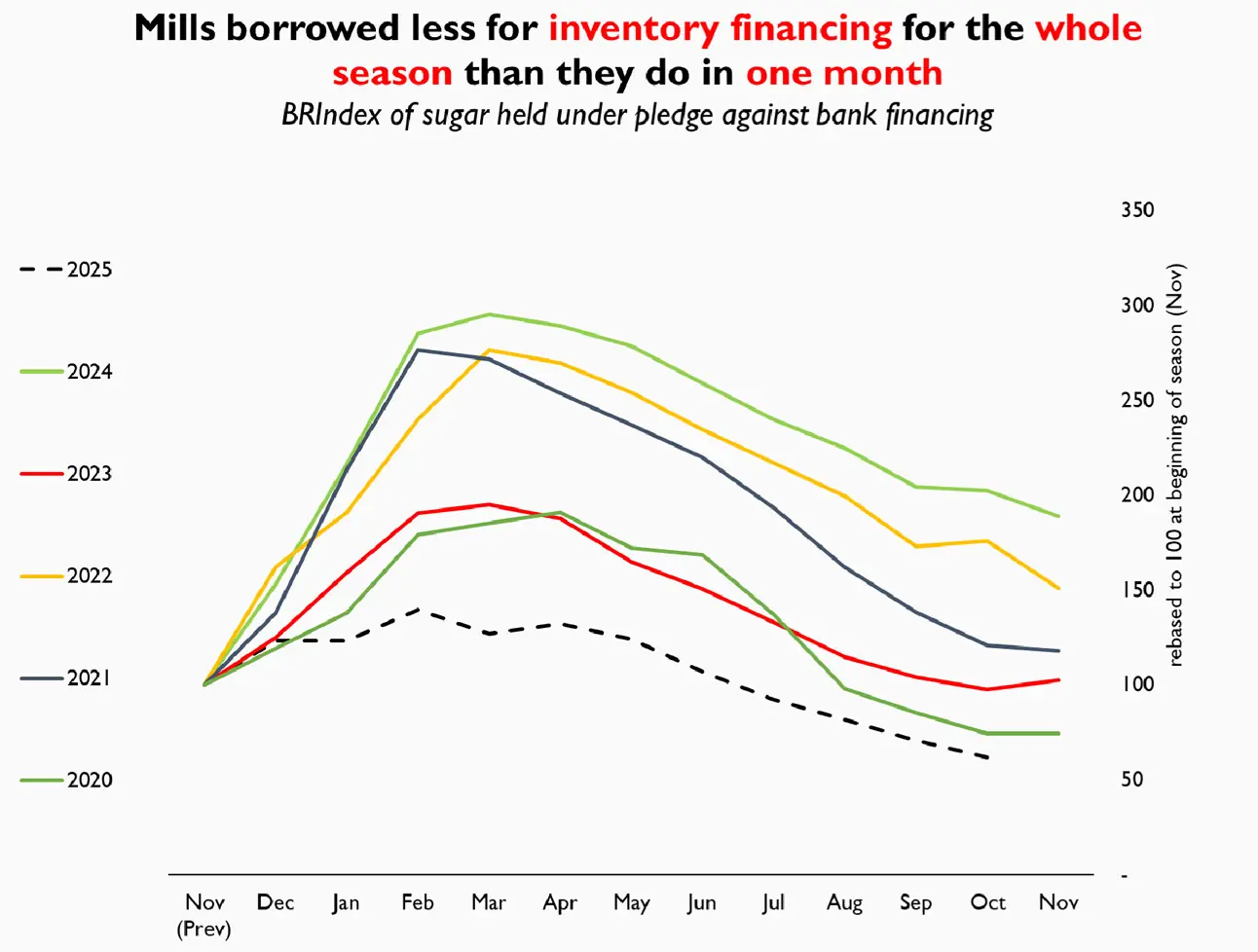

Mills operated with lighter carry-forward stock than usual and bank borrowing remained unusually subdued. According to the BRIndex, total financing for inventory across the year was lower than what mills once drew in a single month.

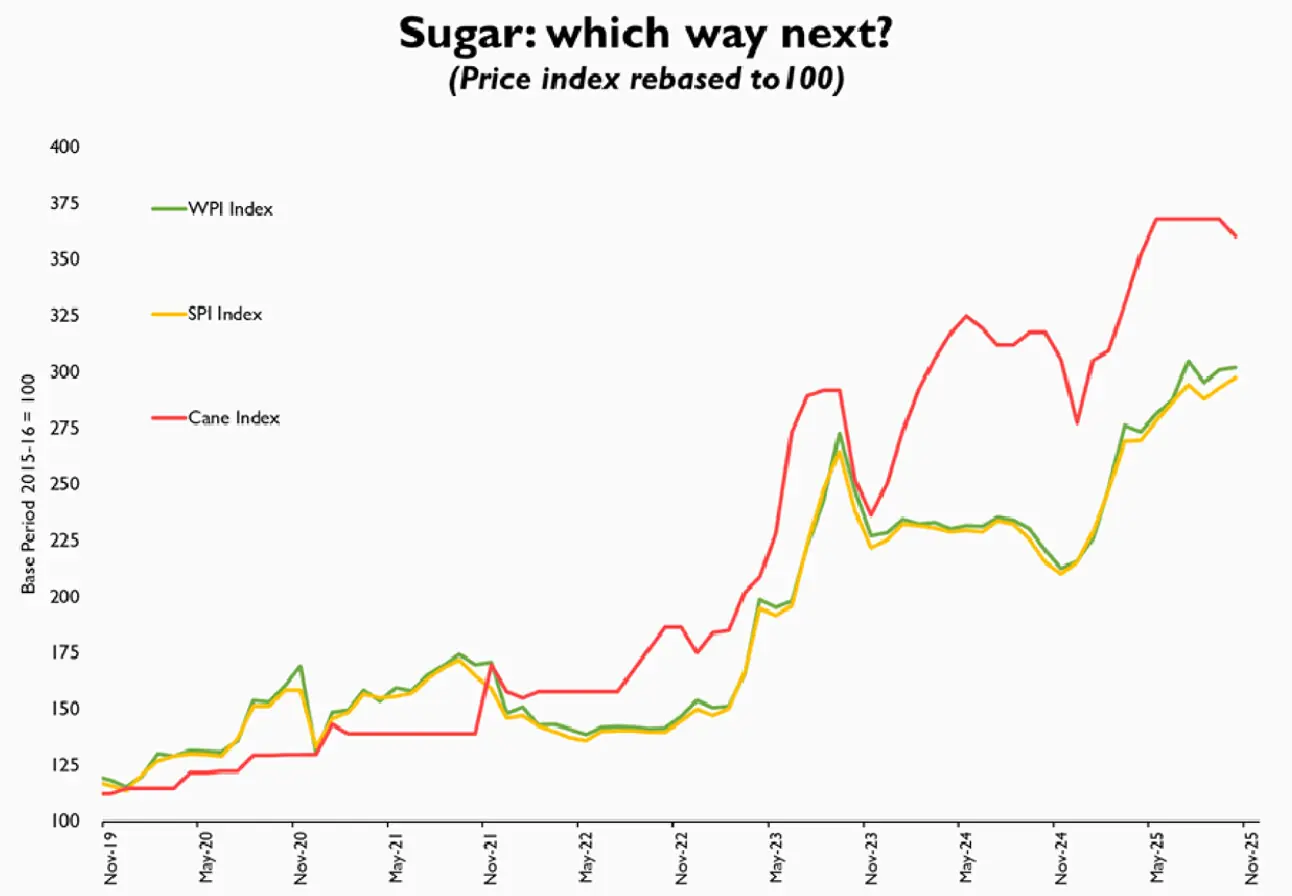

But now the fundamentals have shifted: the cane index has decoupled visibly from SPI and WPI trends. That gap cannot stretch indefinitely. With bank liquidity no longer available at negative real rates unlike yesteryears, the more logical adjustment should come from the consumer price side. That means retail prices must start absorbing the global decline instead of defying it.

The relationship between mill margins and retail stability has narrowed. The policy window to manage this trade-off has also shrunk. With broader fiscal stress and no budgetary space, there is little room to repeat the stopgap measures of the past.

The correction therefore should not be treated as a risk. It should be treated as an opportunity. If the government avoids mid-season interventions once crushing begins, and if export signals are held back until domestic supply is fully counted, the price adjustment can be gradual. It would allow the market to rebalance without panic. It would ease pressure on consumers at a time when food inflation risks have resurfaced. And it would restore credibility to a commodity market that has lived on speculation rather than fundamentals for too long.

If, however, policy tilts toward administrative control or premature export announcements the correction will still come only faster and with greater cost. A thin stock cushion makes it harder to manage sudden shocks. When godowns are full the state can nudge prices. When they are bare it only invites volatility. This must be recognised before we repeat the errors of previous cycles.

The coming year does not require a dramatic intervention. It requires discipline. Sugar will no longer be in a shortage territory. Mills are not in a position to run aggressive games. And the global price curve is pointing in one direction. A controlled descent is not only possible. It is necessary. The market does not need another year of tension and speculation. It needs a clean acceptance that the peak has passed and that the correction must begin before pressure makes the decision for us.

Comments

Comments are closed for this article.