Fecto Cement Limited (PSX: FECTC) was incorporated in Pakistan as a public limited company in 1981. The company is engaged in the manufacturing and sale of Portland cement.

Pattern of Shareholding

As of June 30, 2025, FECTC has a total of 50.16 million shares outstanding which are held by 2742 shareholders. The company’s directors have the majority stake of 75.13 percent in the company followed by local individuals holding 12.52 percent shares.

Banks, DFIs, NBFIs and Insurance Companies collectively hold 7.50 percent of FECTC’s shares while NIT & ICP hold 2.25 percent shares.Joint stock companies account for 1.77 percent shares of FECTC. The remaining shares are held by other categories of shareholders.

HistoricalPerformance (2019-25)

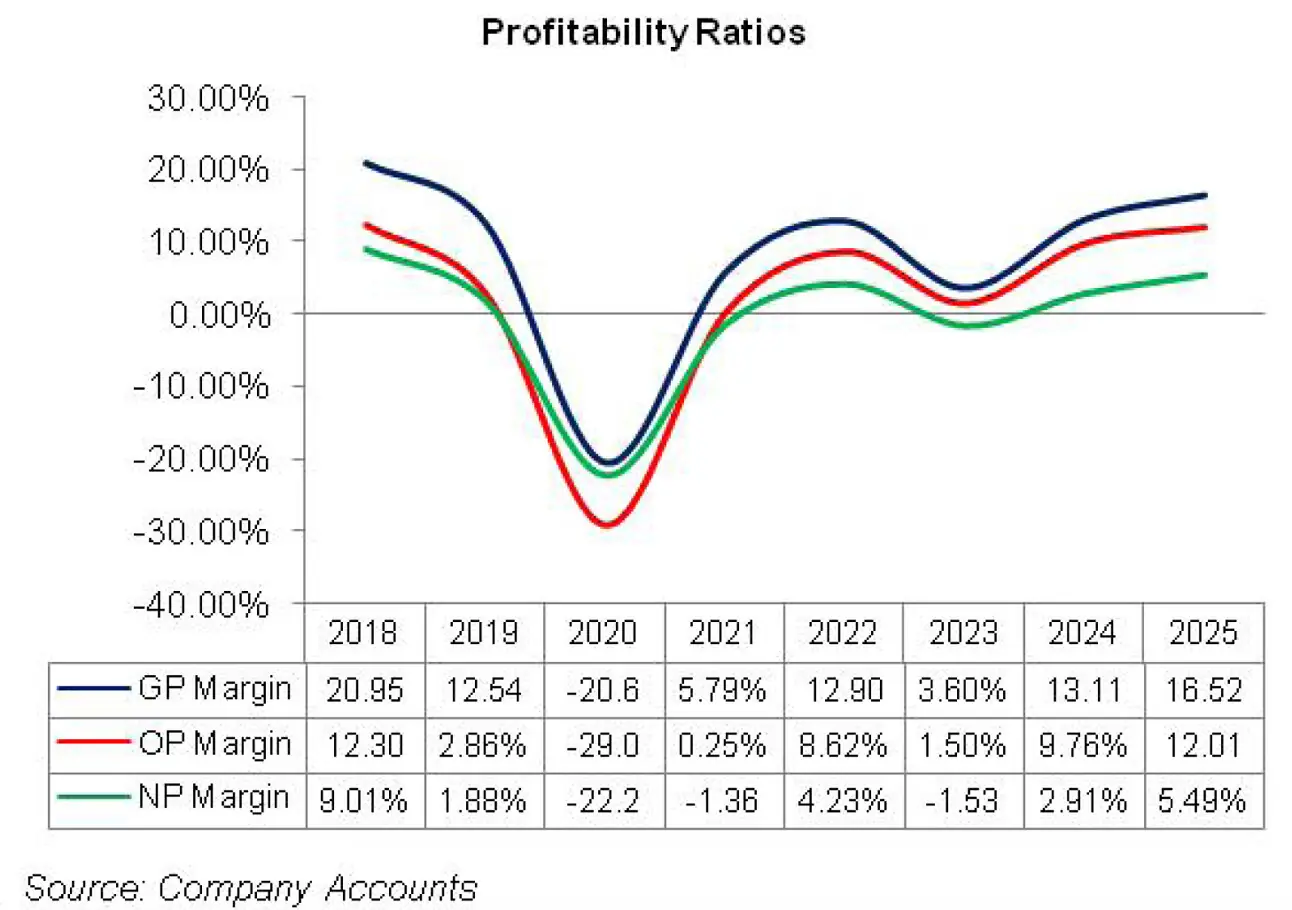

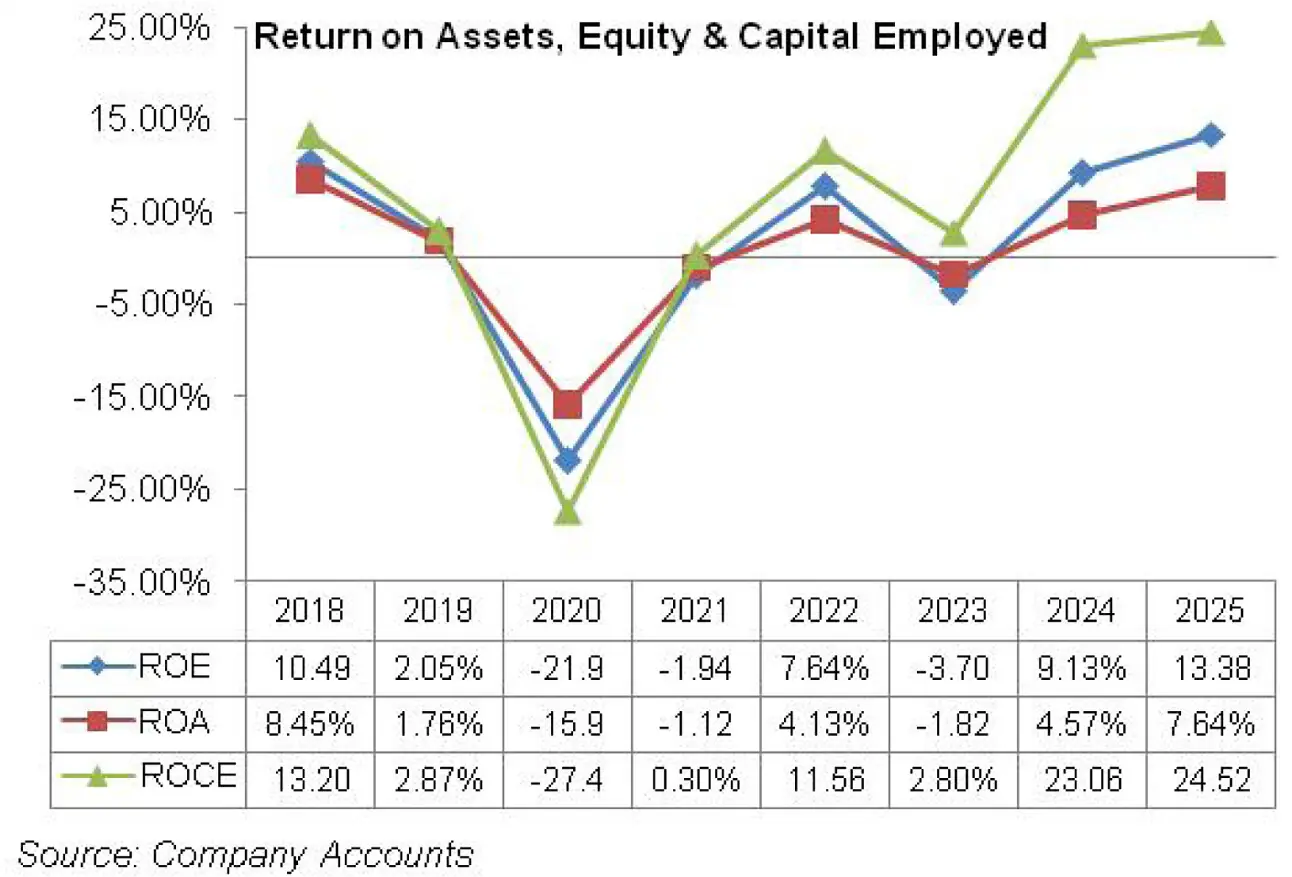

Afterposting year-on-year decline in 2019 and 2020, FECTC’s topline took an upward flight thereafter. Conversely, its bottomline continued to plunge until 2020 when FECTC posted net loss. The company couldn’t recover from net loss in 2021, however, the magnitude of net loss lessened.

In 2022, FECTC registered net profit only to fall back in the loss pit in 2023. In 2024, FECTC posted net profit which further grew in 2025. The company’s margins, which dwindled until 2020, posted recovery in 2021 and 2022.

In 2023, FECTC’s margins drastically plunged followed by a considerable improvement in 2024 and 2025(see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, FECTC’s topline plummeted by a marginal 3.31 percent year-on-year to clock in at Rs.4540.50 million. This was the consequence of curtailed cement dispatches during the year which clocked in 682,612 tons, down 13.76 percent year-on-year.

In 2019, the company made over 90 percent of its sales in the local market with export sales constituting only 9.7 percent of the overall sales mix.

During the year, local and export sales volume of the company fell by 14.41 percent and 7.21 percent, respectively. This was the result of lower demand on account of sluggish economic activity.

Cost of sales inched up by 7 percent year-on-yearin 2019 which was due to steep rise in coal prices in the international market which was further exacerbated by Pak Rupee depreciation.

Moreover, high power cost, stevedoring and transportation cost of coal and higher prices of cement bags also drove up the overall cost of production. This culminated into 42.15 percent year-on-year drop in gross profit in 2019 with GP margin falling from 20.95 percent in 2018 to 12.54 percent in 2019.

Despite inflationary pressure, FECTC was able to cut down its administrative expense by 1.73 percent year-on-year in 2019. This was achieved as the company incurred initial expenditure on new manufacturing plant in the previous year which was significantly reduced in 2019.

Distribution expense also posted a marginal 3.83 percent uptick in 2019 primarily due to higher sales commission and depreciation charges incurred during the year. Other income fell by a massive 58.28 percent year-on-year in 2019 due to high-base effect as FECTC recognized gain on the sale of its operating fixed assets in 2018 which it didn’t recognize in 2019.

Operating profit shrank by 77.49 percent year-on-year in 2019 with OP margin sliding from 12.30 percent in 2018 to 2.86 percent in 2019.

FECTC had a very skimpy debt-to-equity ratio of around 1 percent as of June 2019, hence its finance cost accounted for a mere 0.11 percent of its topline.

FECTC’s finance cost grew by 64.64 percent year-on-year in 2019 due to higher discount rate. Its bottomline witnessed a drastic 79.86 percent year-on-year slippage in 2019 to clock in at Rs.88.975 million with EPS of Rs.1.77 versus EPS of Rs.8.81 recorded in 2018. NP margin also plummeted from 9.01 percent in 2018 to 1.88 percent in 2019.

In 2020, FECTC’s topline further diminished by 26.93 percent year-on-year to clock in at Rs.3463.90 million. This was because cement dispatches eroded by 6.03 percent year-on-year to clock in at 641,450 tons due to lackluster construction activities and the imposition of lockdown in the latter half of the year on account of COVID-19.

Geographical breakup of sales reveals that local dispatches shrank by 7.5 percent in 2020 to clock in at 571,106 tons. Conversely, export dispatches registered 6.11 percent escalation in 2020 to stand at 70,344 tons – representing 10.96 percent of the total sales mix.

Cost of sales ticked up by 0.80 percent year-on-year in 2020 due to Pak Rupee depreciation, high power charges, withdrawal of subsidy on industrial consumers, high transportation cost, and stevedoring charges.

All these factors reversed the positive impact of a retreat of coal prices from their peak due to global slowdown. FECTC registered gross loss of Rs.715.44 million in 2020.

Due to abridged operations on account of the reasons explained above, the company was able to trim down its administrative and distribution expense by 16.72 percent and 53.64 percent respectively in 2020.

Operating loss was recorded at Rs.1005.67 million in 2020. To add to ado, there was a sweeping 431.39 percent year-on-year spike in finance cost in 2020. This was because of a significant escalation in the company’s short-term borrowings which primarily included running finance and export re-finance.

Furthermore, the company also availed SBP Re-finance scheme for the payment of salaries and wages in 2020. This took FECTC’s debt-to-equity ratio to 4 percent in 2020. The company posted net loss of Rs.770.071 million in 2020 with loss per share of Rs.15.35.

Since 2021, FECTC’s net sales began the journey of growth. In 2021, its net sales rebounded by 43.23 percent year-on-year to clock in at Rs.4961.38 million. This was on account of 13.97 percent enhancement in its dispatches which stood at 731.069 tons.

Moreover, prices which remained depressed in 2020 also recoiled during 2021 on the back of resumption of construction activities as the government initiated various stimulus packages. FECTC’s local sales volume grew by 18.43 percent year-on-year in 2021 to clock in at 676,337 tons.

However, export dispatches took 22.19 percent slide to stand at 54,732 tons in 2021. Cost of sales surged by 11.83 percent year-on-year in 2021, however, upward revision in pricing resulted in a GP margin of 5.80 percent and gross profit of Rs.287.5 million as against gross loss recorded in the previous year.

Administrative and distribution expenses eroded by 5.47 percent and 6.5 percent respectively,resulting in an operating profit of Rs.12.43 million and OP margin of 0.25 percent in 2021.

Despite monetary easing, FECTC’s finance cost surged by 165.34 percent year-on-year in 2021 as the company availed SBP Refinance scheme for renewable energy and also obtained additional running finance. Escalation in company’s outstanding loans is also evident in a steep hike in its debt-to-equity ratio which clocked in at 18 percent in 2021.

FECTC posted net loss of Rs.67.287 million in 2021, down 91.26 percent year-on-year. Loss per share was recorded at Rs.1.34 in 2021.

FECTC’s topline continued to grow in 2022, however, unlike 2021; the topline growth didn’t come to the heels on improved sales volumeit was the result of upward price revision.

In 2022, FECTC’s topline mounted by 36.55 percent year-on-year to clock in at Rs. 6774.57 million. This was despite the fact that its sales volume tumbled by 2.52 percent to clock in at 712,644 tons. While local sales volume posted a marginal 1.44 percent rise to stand at 686,077 tons, export sales volume declined by a massive 51.5 percent due to disturbance at Afghan border and lesser demand from Afghanistan market.

Higher cement prices are evident by the fact that the company attained 203.87 percent rise in its gross profit in 2022 with GP margin climbing up to 12.90 percent. Administrative expense spiked by 15.40 percent year-on-year in 2022 due to higher payroll expense.

Conversely, as sales volume fell, distribution expense slumped by 7.55 percent year-on-year. Scrap sales made during the year coupled with amortization of deferred government grant drove up other income by 88 percent in 2022. As a consequence, operation profit magnified by 4597.56 percent in 2022 with OP margin flying up to 8.62 percent.

Finance cost soared by 104.75 percent in 2022 due to higher discount rate coupled with increased long-term borrowings as the company availed temporary economic refinance facility (TERF) during the year along with refinance scheme for the payment of wages and renewable energy financing scheme.

Increased borrowing had its impact on debt-to-equity ratio which sky-rocketed to 26 percent in 2022. Elevated finance cost coupled with increased taxation greatly diluted the bottomline growth. However, FECTC was able to record net profit of Rs.286.703 million in 2022 with EPS of Rs.5.72. NP margin stood at 4.23 percent in 2022.

The topline continued to grow in 2023 to the tune of 28.16 percent to clock in at Rs.8682.18 million.

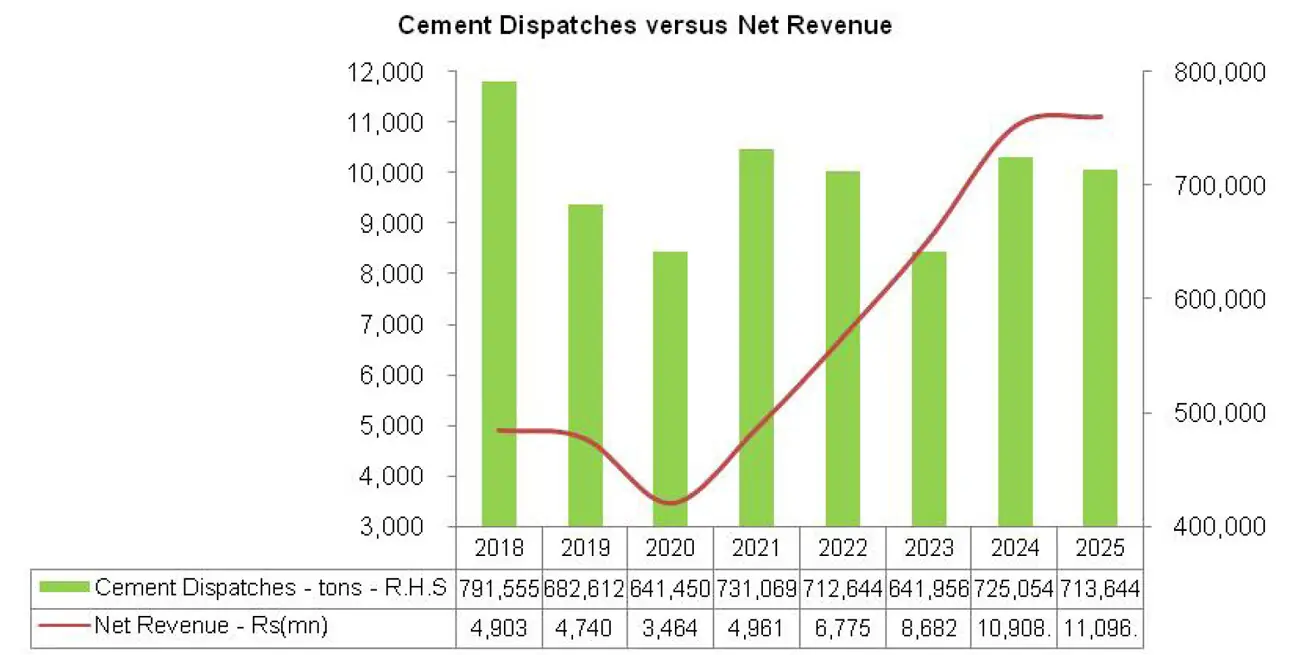

Just like the previous year, the topline growth was the consequence of upward revision in the prices of cement despite the fact that dispatches took 9.92 percent slide to clock in at 641,956 tons in 2023. This came on the back of a decline of 9.65 percent and 16.69 percent respectively in the local and export sales volume of the company (see the graph of cement dispatches and net revenue).

Economic and political uncertainty in the country as well as devastating floods took its toll on the local demand while low demand from Afghanistan and border nuisances kept export sales in check.

Cost of sales hiked by a staggering 41.84 percent in 2023 on the back of sky-rocketed prices of coal, diesel and electricity coupled with Pak Rupee depreciation. Amid depressed demand, the company couldn’t pass on the impact of cost hike completely to its consumers, which resulted in 64.24 percent erosion of gross profit in 2023 with GP margin dwindling to 3.60 percent.

Administrative expense soared by 17.37 percent year-on-year in 2023 due to higher payroll expense and depreciation. Increased salaries and wages drove up the distribution expense by 13.73 percent year-on-year in 2023. The company sold off its operating assets at a gain in 2023 which resulted in 187.81 percent rise in its other income in 2023.

Yet, it was unable to provide any impetus to its operating profit which contracted by 77.70percent year-on-year in 2023 with OP margin marching down to 1.50 percent. Finance cost mounted by 95.32 percent year-on-year in 2023 due to enormous borrowings particularly running finance. FECTC recorded net loss of Rs.133.245 million in 2023 with loss per share of Rs.2.66.

In 2024, FECTC recorded 25.64 percent growth year-on-year in its topline which clocked in at Rs.10,908.12 million. This came on the back of 12.94 percent rise in the company’s sales volume which stood at 725,054 tons in 2024.

Volumetric growth was driven by local sales which grew by 15 percent in 2024 to clock in at 712,769 tons. Conversely, export sales volume dipped by 44.43 percent to clock in at 12,284 tons. This was due to unattractive prices in the international market.

The company significantly increased the prices to account for inflationary pressure and high energy cost. This resulted in 357.58 percent improvement in gross profit in 2024 with GP margin climbing up to 13.11 percent. Administrative expense surged by 11.81 percent in 2024 due to higher payroll expense on account of inflationary pressure.

The company squeezed its workforce from 336 employees in 2023 to 330 employees in 2024. Distribution expense escalated by 15.74 percent in 2024 due to higher salaries & benefits of the distribution staff as well as elevated marking fee. Other income dipped by 48.96 percent in 2024 due to high-base effect as the company recorded gain on sale of investment property in the previous year.

Other expense plummeted by 44.44 percent in 2024 due to high-base effect as the company recorded loss on sale of obsolete bags in 2023. On the positive front, the company recorded share of profit worth Rs.18.90 million on its associate, FECTC’s operating profit improved by 749.84 percent in 2024 with OP margin rising tremendously to 10.15 percent.

Finance cost tapered off by 8.91 percent in 2024 as the company paid off a huge portion of its outstanding liabilities during the year. FECTC recorded net profit of Rs.359.967 million in 2024. This is translated into EPS of Rs.7.18 and NP margin of 3.30 percent.

In 2025, FECTC’s net sales ticked up by 1.73 percent to clock in at Rs.11,096.92 million. This came on the back of upward revision in cement prices during the year. Dispatches fell by 1.60 percent year-on-year to clock in at 713,644 tons in 2025.

The decline in dispatches came on the back of 3.09 percent slash in local dispatches which clocked in at 690,987 tons in 2025. This was due to weakened private housing sector, limited credit availability, high construction cost, slow disbursement of PSDP and sluggish recovery in real estate and infrastructure related sectors.

Conversely, export dispatches posted a staggering year-on-year growth of 88.18 percent to clock in at 22,657 tons in 2025.

Export sales stood at 3.174 percent of the company’s total dispatches in 2025 versus their share of 1.66 percent in the previous year.

Cost of sales ticked down by 2.27 percent in 2025 due to cost optimization strategies adopted by the company which included improved coal utilization per ton of final product. This enabled the company to record 28.24 percent stronger gross profit in 2025 with GP margin climbing up to 16.52 percent.

Administrative expense heightened by 24.85 percent in 2025 due to higher payroll expense on account of inflationary pressure as well workforce expansion from 330 employees in 2024 to 337 employees in 2025.

Distribution expense surged by 30.46 percent in 2025 due to higher salaries of sales force and transportation expense incurred during the year. Liabilities no longer payable written off during the year resulted in 23.63 percent improvement in other income in 2025. Other expense surged by 232.64 percent in 2025 due to stocks and in-adjustable input tax written off during the year.

FECTC was able to record net other income of Rs.132.45 million in 2025, up 18.12 percent year-on-year. However, it was partially offset by share of loss of associate worth Rs.60.96 million recorded in 2025.

Finance cost tapered off by 37.65 percent in 2025 due to monetary easing and a considerable decline in outstanding borrowings at the end of the year. Net profit multiplied by 69.10 percent to clock in at Rs.608.692 million in 2025. This translated into EPS of Rs.12.14 and NP margin of 5.49 percent in 2025.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, FECTC posted 23.87 percent enhancement in its topline, which clocked in at Rs.3561.314 million. This came on the back of a marvelous recovery of 42.93 percent in the overall dispatches of the company which stood at 243,108 tons in 1QFY26.

Unlike last year, when local demand was muted, during the period under consideration, local dispatches mounted by 48.21 percent to clock in at 240,118 tons. This was due to broad based development in macroeconomic conditions. Conversely, export sales dipped by 63.02 percent to clock in at 2990 tons in 1QFY26.as majority of the export demand was met by the companies in the south zone.

Due to higher demand, the company recorded capacity utilization of 98.19 percent in 1QFY26 versus capacity utilization of 66.24 percent recorded in 1QFY25. Cost of sales surged by 31 percent in 1QFY26, which was in line with higher production volumes. The company continued to squeeze its cost per ton, which was recorded at Rs.11,927 per ton, down 8.30 percent year-on-year.

Despite cost optimization, gross profit tumbled by 0.14 percent in 1QFY26 with GP margin clocking in at 18.58 percent versus GP margin of 23 percent recorded in 1QFY25. This was due to negative prices variance as retention prices dropped by Rs.2254 per ton to Rs.14,649 in 1QFY26.

Higher operational activity resulted in 14.98 percent escalation in administrative expense in 1QFY26. Distribution expense dipped by 5.73 percent in 1QFY26 due to lower export sales and stable fuel prices. Operating profit ticked up by 3.40 percent in 1QFY26 with OP margin clocking in at 14.78 percent versus OP margin of 17.71 percent recorded in 1QFY25.

Better working capital management coupled with monetary easing allowed FECTC to shave off its finance cost by 51.41 percent in 1QFY26. Increase in levies and taxes compressed the net profit of the company in 1QFY26 which clocked in at Rs.207.78 million, down 9 percent year-on-year. This translated into EPS of Rs.4.14 in 1QFY26 versus EPS of Rs.4.55 recorded in 1QFY25. NP margin also dropped from 7.94 percent in 1QFY25 to 5.83 percent in 1QFY26.

Future Outlook

Lowering inflation, subsided discount rate and declining fuel prices in the international market will augur well for the cement companies in the long-term. Improving investor confidence and availability of low-cost financingwill boost private sector investments. The government is also expected to make disbursements under some core PSDP projects during the year.

Infrastructure development in the flood affected areas will also boost cement demand. However, geopolitical tensions, indigenous political instability, high excise duties, and property taxes can have an adverse impact on the demand.

Comments

Comments are closed for this article.