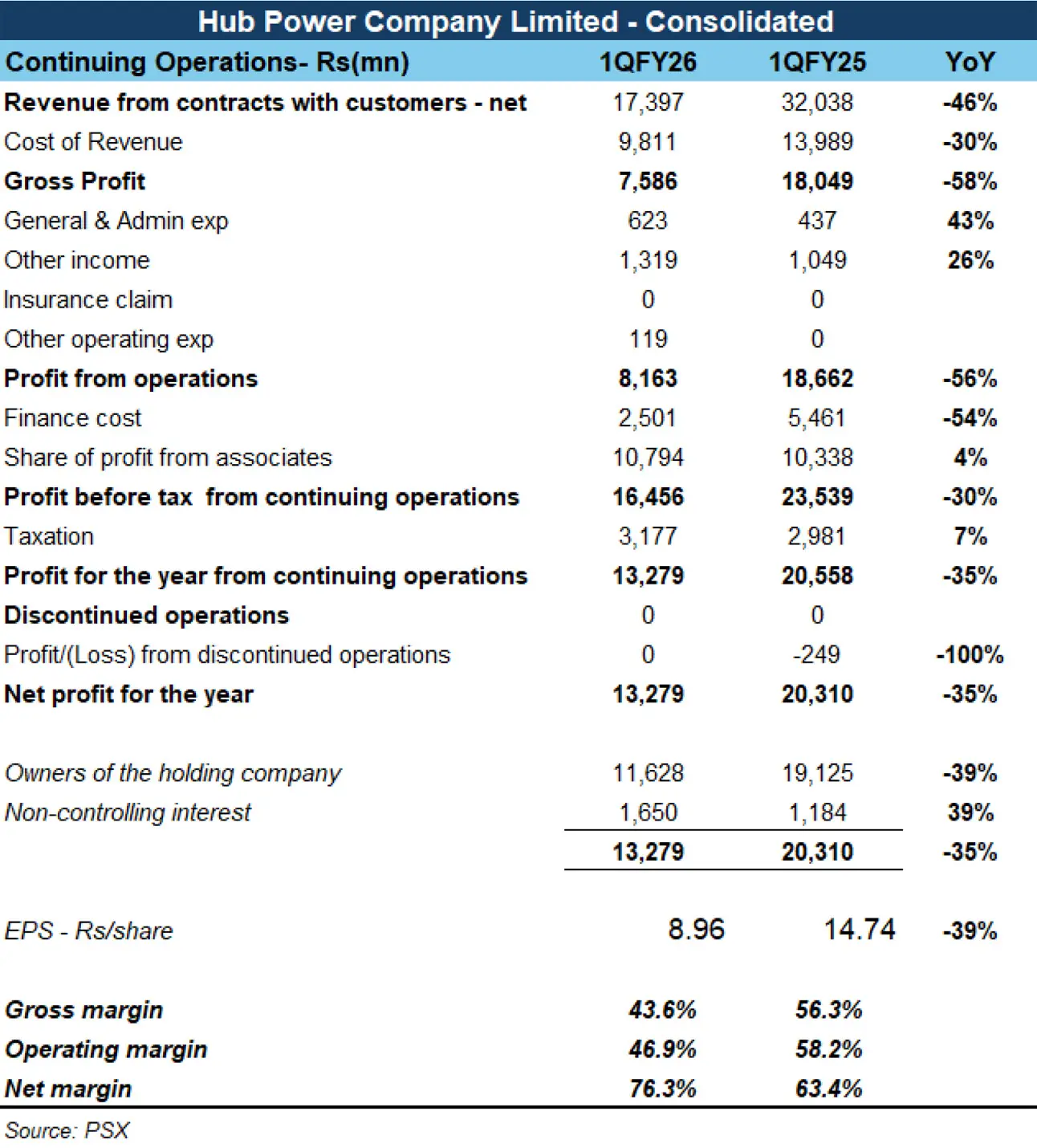

Hub Power Company Limited (PSX: HUBC) posted consolidated earnings of Rs11.6 billion in 1QFY26, marking a 39 percent year-on-year decline. The contraction was driven by the absence of base plant contribution and the revised tariff structure for Narowal Energy Limited (NEL).

Despite lower profitability, the company announced a cash dividend of Rs5 per share, reflecting strong liquidity underpinned by continued dividend inflows from associates.

Net revenue fell 46 percent year-on-year, as lower plant utilization and the exclusion of the base plant curtailed topline growth.

The gross profit margin compressed following the PPA revision for Narowal and loss of base plant earnings.

Even so, profitability remained supported by high-margin income from associates and joint ventures, which collectively contributed Rs10.8 billion, up 4 percent year-on-year, led by China Power Hub Generation Company (CPHGC) and early earnings from BYD’s local operations. Other income also grew 26 percent, driven by higher dividend receipts and improved recoveries.

On the cost side, administrative expenses surged by over 270 percent year-on-year, reflecting project costs related to BYD and the Thar energy ventures. In contrast, finance costs declined 54 percent, owing to lower interest rates and repayment of project-related debt.

Earnings composition continues to shift toward CPEC-linked independent power projects (IPPs) — namely CPHGC, Thar Energy Limited (TEL), and Thal Nova Power (TNPTL) — with both Thar projects nearing their Project Completion Date (PCD). These are expected to unlock new dividend streams during FY26, anchoring future cash flows.

Strategically, HUBC is transitioning from a pure power producer to a diversified energy and industrial platform.

The company has expanded its footprint in Thar coal mining (SECMC), oil and gas exploration (Prime International), and mineral development (Ark Metals). It is also investing in electric mobility and green infrastructure, with the BYD Gharo CKD plant expected to commence operations in 2H2026, and an EV charging network planned along the Karachi–Peshawar corridor.

At the same time, HUBC is evaluating the commercial redevelopment of its 1,100-acre Hub site, including a potential aluminium smelter leveraging local bauxite reserves and surplus energy, or a Single Point Mooring (SPM) facility in partnership with PSO for oil imports via existing pipeline infrastructure.

HUBC’s 1QFY26 results highlight a company in transition — short-term earnings softened by structural changes, but medium-term prospects underpinned by strong associate income, Thar project dividends, and diversification into high-growth sectors such as EVs, mining, and green energy.

Comments

Comments are closed for this article.