Cherat Cement Company Limited (PSX: CHCC) was incorporated in Pakistan as a public limited company in 1981. The company is engaged in the manufacturing, marketing and sale of cement.

Pattern of Shareholding

As of June 30, 2025, CHCC has a total of 194.295 million shares outstanding which are held by 5424 shareholders. Local general public has a majority stake of 28.76 percent in the company followed by associated companies, undertakings and related parties holding 27.14 percentshares.

Modarabas & Mutual funds account for 11.13 percent of the outstanding shares of CHCC while Banks, DFIs and NBFIs hold 7.13 percent shares. Around 5.79 percent of CHCC’s shares are held by Insurance companies and 3.60 percent by Directors, CEO, and their spouse and minor children.

Foreign companies hold 1.60 percent shares of the company while foreign general public accounts for 1.01 percent shares. The remaining shares are owned by other categories of shareholders.

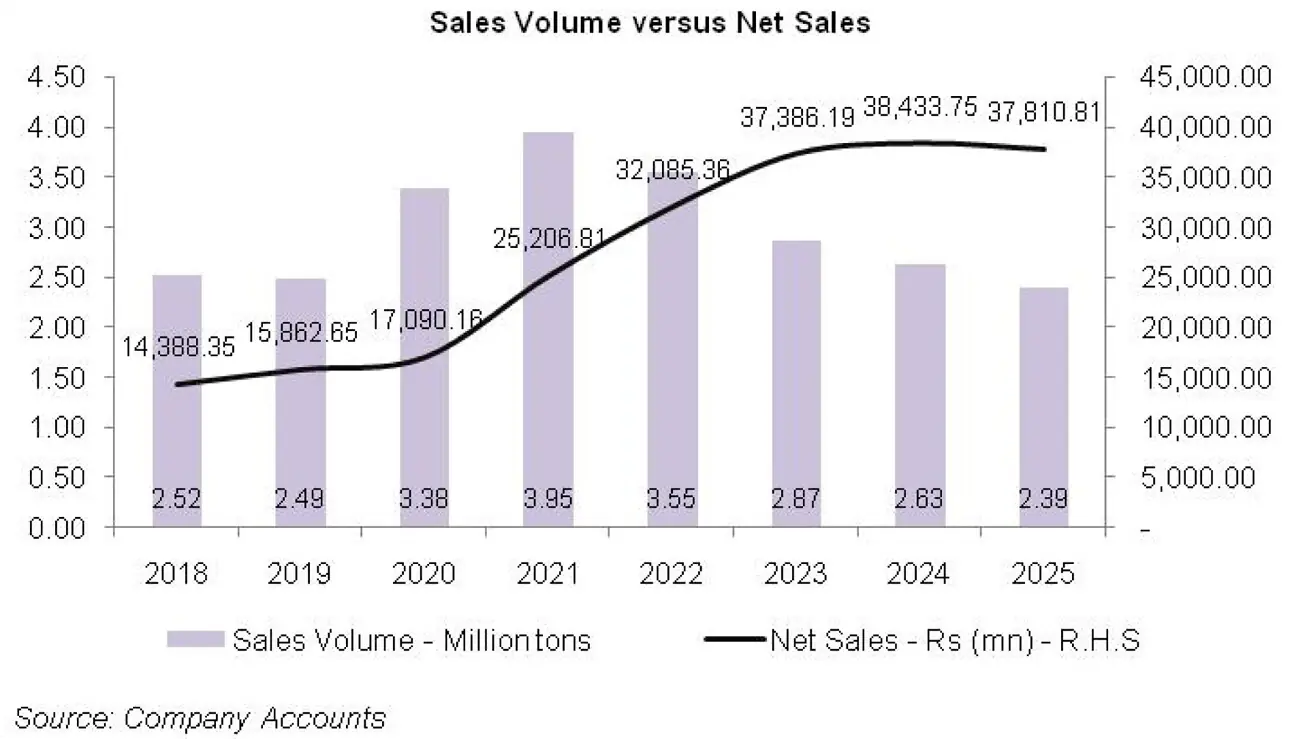

Historical Performance (2019-25)

Except for a year-on-year decline in 2025, CHCC’s topline posted year-on-year growth over the period under consideration. However, its bottomline descended in 2019 and 2020 with net loss recorded in the latter year.

The bottomline rebounded for the next two years followed by a decline in 2023. In 2024 and 2025, CHCC’s net profit reasonably grew to attain its optimum level. The company’s margins followed a similar pattern as its bottomline and reached peak level in 2025. The detailed performance review of the period under consideration is given below.

In 2019, CHCC’s net sales grew by 10.25 percent year-on-year to clock in at Rs.15,862.65 million. While the company’s sales volume stood at almost the same level as last year (see the graph of sales volume), topline growth was the result of upward price revision to pass on the impact of cost hike to its customers.

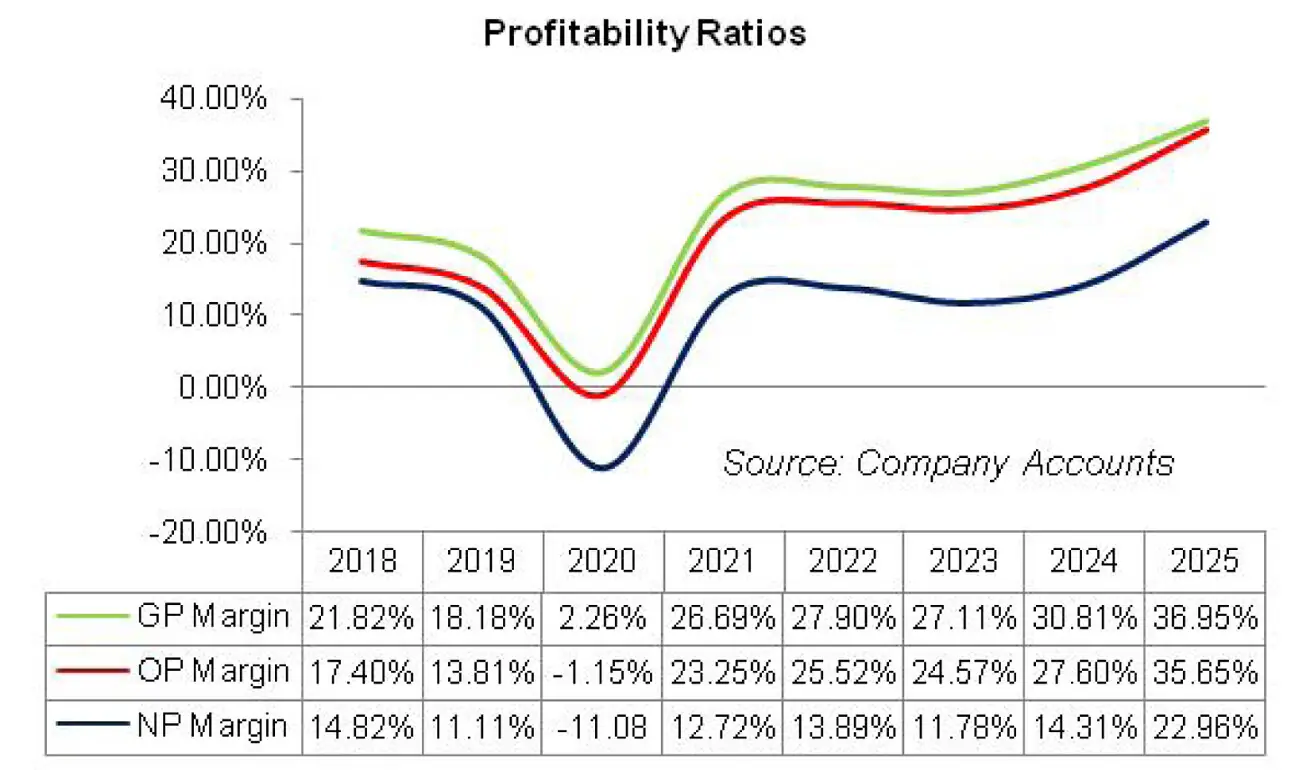

Cost of sales hiked by 15.38 percent year-on-year in 2019 mainly due to heightened fuel prices and Pak Rupee depreciation. This resulted in 8.16 percent slide in CHCC’s gross profit in 2019 with its GP margin moving down from 21.82 percent in 2018 to 18.18 percent in 2019. Distribution expense surged by 17.56 percent in 2019 due to increased salaries and advertisement expenses incurred during the year.

Administrative expense escalated by 19.84 percent in 2019 due to inflationary pressure and also the company expanded its workforce from 885 employees in 2018 to 1012 employees in 2019 which led to higher payroll expense.

Elevated exchange loss was offset by lower profit related provisioning, resulting in 18.37 percent contraction in other expense in 2019. Other income strengthened by 31.71 percent in 2019 due to higher scrap sales. CHCC recorded 12.53 percent reduction in its operating profit in 2019 with OP margin sliding down to 13.81 percent from OP margin of 17.40 percent recorded in 2018.

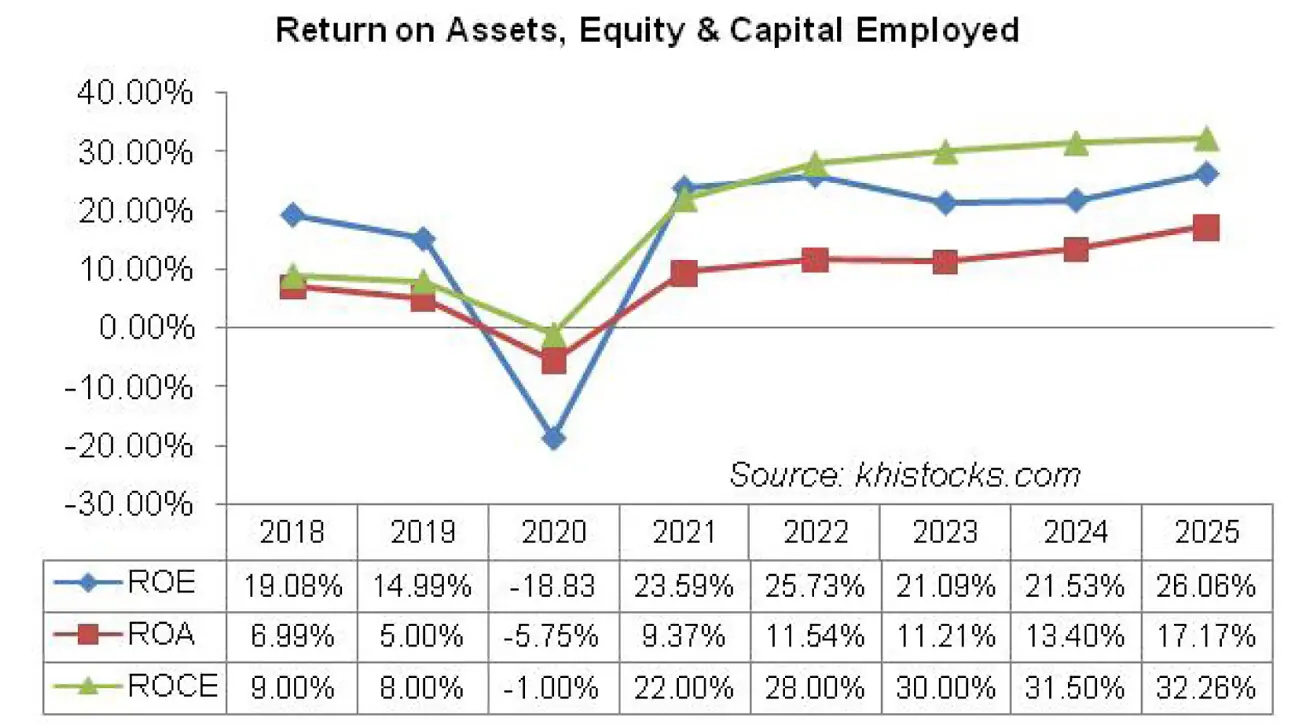

Finance cost soared by 220.42 percent in 2019 due to higher discount rate and increased borrowings associated with the construction of new cement line. Gearing ratio hiked from 59.25 percent in 2018 to 64.24 percent in 2019.

The announcement of Federal budget also led to reversal of tax benefit availed by the company under section 65-B of Income Tax Ordinance. This resulted in 17.32 percent decline in CHCC’s net profit which clocked in at Rs.1762.76 million in 2019 with EPS of Rs.9.07 versus EPS of Rs.12.07 recorded in the previous year. NP margin also fell from 14.82 percent in 2018 to 11.11 percent in 2019.

CHCC recorded 7.74 percent year-on-year uptick in its topline which clocked in at Rs. 17,090.16 million in 2020. Due to the commissioning of new cement line in 2019, the company was able to increase its dispatches by 35.46 percent in 2020, which clocked in at 3.377 million tons. Local sales rose by 36 percent during the year while sales to Afghanistan grew by 32 percent.

Hefty increase in sales volume is not reflected in the company’s topline growth during the year due to price wars. Cost of sales grew by 28.69 percent in 2020 which squeezed the gross profit by 86.59 percent in 2020. GP margin drastically fell to 2.26 percent in 2020.

Distribution expense declined by 8.66 percent in 2020 due to lower salaries of sales force. During the year, the company streamlined its workforce to 972 employees which resulted in 7.54 percent lower administrative expense.

No provisioning for WPPF and no exchange loss incurred during the year resulted in 82.60 percent plunge in other expense in 2020. Other income also plummeted by 33.95 percent in 2020 due to less scrap sales and smaller dividend amount received from related parties. CHCC incurred operating loss of Rs.195.73 million in 2020.

The situation was further aggravated by 121.17 percent spike in finance cost in 2020. This was the result of higher discount rate and hefty long-term loans obtained for the installation of new production line in 2019.

CHCC’s gearing ratio enlarged to 67.12 percent in 2020. The company incurred net loss of Rs.1893.11 million in 2020 with loss per share of Rs.9.74.

CHCC clearly seems out of hot waters in 2021 with its topline staggeringly growing by 47.49 percent to clock in at Rs.25,206.81 million.

Not only did CHCC did immensely well in 2021, but the entire industry’s dispatches also rose by 21 percent on account of launch of several government backed construction projects and enhanced allocation and disbursement of funds for PSDP.

CHCC’s cement dispatches rose by 16.96 percent to clock in at 3.950 million tons. Local sales volume grew by 18 percent and export sales grew by 8 percent in 2021. Higher demand also enabled the company to revise its prices, which resulted in 1640.89 percent bigger gross profit in 2021 with GP margin jumping up to 26.69 percent.

Distribution expense grew by 18.58 percent in 2021 on account of increased sales volume. While the company squeezed its workforce to 966 employees in 2021, inflationary pressure didn’t allow payroll expense to subside. This resulted in 7.16 percent taller administrative expense incurred during the year.

Enormous provisioning worth Rs.228.274 million booked for WPPF resulted in 1221 percent surge in other expense in 2021.

Other income grew by 48.67 percent in 2021 on the back of gain on redemption of short-term investments and increased profit on bank accounts. Scrap sales, although slid in 2021, however, made the biggest chunk of CHCC’s other income.

The company made a robust operating profit of Rs.5861.40 million in 2021 which was the highest ever operating profit recorded by the company to-date. Finance cost lowered by 39.68 million in 2021 due to monetary easing and a downtick in long-term and short-term financing.

Gearing ratio fell to 55.98 percent in 2021. CHCC registered net profit of Rs.3205.06 million in 2021 with EPS of Rs.16.50 and NP margin of 12.72 percent.

In 2022, CHCC’s topline further strengthened by 27.29 percent to clock in at Rs.32,085.36 million. Overall cement industry dispatches declined by 8 percent in 2022 due to economic and political instability in the home market and geopolitical tensions in Afghanistan.

CHCC sales volume dipped by 10 percent to clock in at 3.552 million tons in 2022. Local and export sales of CHCC dipped by 5 percent and 43 percent respectively during the year. Hence, topline growth was merely the result of upward revision in cement prices to account for inflation and Pak Rupee deprecation.

Russia-Ukraine crisis also led to commodity super-cycle in the international market. Gross profit enhanced by 33 percent in 2022 with GP margin climbing up to 27.90 percent. Distribution expense spiked by 23.29 percent in 2022 due to higher fuel prices. Administrative expense enlarged by 19.89 percent in 2022 due to higher payroll expense as CHCC increased its employee headcount to 1007 in 2022, resulting in elevated payroll expense.

Other expense ticked up by 9.53 percent in 2022 due to provisioning done for WWF. Other expense was completely offset by 272.25 percent higher other income recorded by CHCC in 2022 which was the consequence of exchange gain recorded on escrow account. Operating profit strengthened by 39.69 percent in 2022 with OP margin rising up to 25.52 percent.

Despite monetary tightening, CHCC was able to cut down its finance cost by 10.85 percent in 2022 due to repayment of outstanding loans. This enabled the company to mark down its gearing ratio to 48.59 percent in 2022. Net profit enhanced by 39 percent in 2022 to clock in at Rs.4455.97 million with EPS of Rs.22.93 and NP margin of 13.89 percent.

CHCC’s topline registered 16.52 percent ascent to clock in at Rs. 37,386.19 million in 2023. The country was passing through a rough patch with diminishing FOREX reserves.

In order to resume the IMF program, the government had to take austerity measures in both monetary and fiscal domains. This significantly slowed down the overall economy. Cement industry dispatches recorded a decline of 16 percent in 2023 due to thinner PSDP budget, shaky investor confidence and higher financing rates.

Increase in sales tax and FED on cement also inhibited demand. CHCC’s sales volume plunged by 19.17 percent to clock in at 2.871 million tons in 2023. Local and export sales slid by 16 percent and 13 percent respectively in 2023. Hike in coal, fuel, electricity and other raw material prices coupled with Pak Rupee depreciation resulted in 17.79 percent hike in cost of sales in 2023.

Gross profit in absolute terms grew by 13.25 percent in 2023, however, GP margin inched down to 27.11 percent. Distribution expense swelled by 14.58 percent in 2023 due to inflationary pressure.

Increase in employee headcount to 1022 and inflationary pressure resulted in higher payroll expense which pushed up administrative expense by 24.91 percent in 2023. Other expense spiked by 31.51 percent in 2023 due to higher profit related provisioning. Other income improved by 16.25 percent in 2023 due to higher scrap sales and profit on bank accounts.

CHCC recorded 12.20 percent higher operating profit in 2023, however, OP margin slid to 24.57 percent. Finance cost increased by 40.86 percent in 2023 due to higher discount rate.

Gearing ratio marched down to 36.72 percent in 2023. Super tax levy increased from 4 percent in 2022 to 10 percent in 2023. This resulted in 1.17 percent contraction in CHCC’s net profit which clocked in at Rs.4403.93 million in 2023 with EPS of Rs.22.67 and NP margin of 11.78 percent.

In 2024, CHCC’s topline ticked up by 2.80 percent to clock in at Rs.38,433.75 million. This primarily came on the back of upward revision in cement prices to offset higher input cost – particularly electricity and gas tariffs.

The company’s overall dispatches tumbled by 8.50 percent to clock in at 2.63 million tons in 2024. While local sales slid by 13 percent, exports sales surged by 22 percent due to increased exports to Afghanistan. During 2024, the company’s cost of sales dropped by 2.41 percent, which was achieved through the optimization of coal and power mix.

Lower cost coupled with increased cement prices resulted in 16.81 percent higher gross profit recorded in 2024 with GP margin attaining an unprecedented level of 30.81 percent.

Higher export sales resulted in 25.42 percent greater distribution expense in 2024. Administrative expense mounted by 14.75 percent in 2024 on account of inflationary pressure. This was despite the fact that CHCC streamlined its workforce from 1022 employees in 2023 to 978 employees in 2024.

Increased profit related provisioning pushed up other expense by 28 percent in 2024; however, it was offset by 8.69 percent higher other income. Superior other income recognized during the year was the result of robust dividend income and profit on bank accounts.

Scrap sales drastically fell during the year. CHCC recorded 15.49 percent higher operating profit in 2024 with OP margin of 27.60 percent. Scheduled and early repayments of long-term loans resulted in 27.85 percent slide in finance cost in 2024 despite high discount rate.

Gearing ratio clocked in at 18.05 percent in 2024. Net profit grew by 24.88 percent in 2024 to clock in at Rs.5499.75 million with EPS of Rs.28.31 and NP margin of 14.31 percent.

Recent Performance (2025)

CHCC’s net sales tapered off by 1.62 percent to clock in at Rs.37,810.81 million in 2025. The company’s overall dispatches contracted by 9 percent to clock in at 2.39 million tons in 2025. Local sales volume slid by 10 percent due to macroeconomic flaws while export sales volume slid by 3 percent due to logistics issues.

The decline in CHCC’s topline would have been more profound if the prices had not increased by Rs.1400 per ton locally and Rs.323 per ton internationally.

During the year, the company raised its overall solar capacity to 23 MW by commissioning an additional 9 MW solar capacity. Efficient coal procurement strategies also kept a check on CHCC’s cost of sales in 2025.

Cost optimization coupled with increased retention prices culminated into 18 percent stronger gross profit in 2025 with GP margin attaining its optimum level of 36.95 percent. Distribution expense escalated by 12.32 percent in 2025 due to higher salaries of sales force and increased advertising & promotion budget allocated for the year.

Administrative expense mounted by 19.18 percent in 2025 due to higher payroll expense. This was despite the fact that the company streamlined its workforce from 978 employees in 2024 to 945 employees in 2025. Other expense multiplied by 35.61 percent in 2025 due to increased profit related provisioning.

Other income posted a staggering 221.92 percent growth in 2025 due to gain recognized on the redemption of short-term investments at FVTPL followed by gain on disposal of property, plant & equipment and scrap sales, CHCC posted 27 percent rebound in its operating profit in 2025 with OP margin picking up to 35.65 percent.

Finance cost dwindled by 57.15 percent in 2025 due to monetary easing and early payment of long-term loans. This resulted in a much lower gearing ratio of 15.15 percent recorded in 2025. CHCC’s net profit posted year-on-year recovery of 57.85 percent to clock in at Rs.8681.36 million. This translated into EPS of Rs.44.68 and NP margin of 22.96 percent in 2025.

Future Outlook

PSDP, CPEC and other government related projects are expected to gain momentum and support local sales volumes in the coming year.

Moreover, infrastructure spending in the flood affected regions will also shape local demand. Exports are also expected to stay strong. Softer coal prices, stable Pak Rupee and lower interest rates are also favorable factors for the cement industry. This coupled with the company’s cost control measures will result in strong margins and profitability.

Comments

Comments are closed for this article.