Bannu Woolen Mills Limited (PSX: BNWM) was incorporated in Pakistan as a public limited company in 1960. It was established by PIDC, however later purchased by Bibojee group of companies. The principal activity of the company is the manufacturing and sale of woolen yarn, cloth and blankets.

Pattern of Shareholding

As of June 30, 2025, BNWM has a total of 9.506 million shares outstanding which are held by 1442 shareholders. Local general public has the highest stake of 52.06 percent in the company followed by associated companies, undertaking and related parties holding 34.75 percent shares.

The company’s leadership which includes its directors, CEO, their spouse and minor children account for 5.79 percent shareholding while NIT and ICP hold 4.55 percent shares. Around 2.20 percent of BNWM’s shares are held by joint stock companies. The remaining ownership is distributed among other categories of shareholders.

Historical Performance (2019-25)

After witnessing a year-on-year plunge in 2019 and 2020, BNWM’s topline rode an upward trajectory until 2023. However, the topline growth momentum lowered each year and translated into a decline in 2024. In 2025, BNWM’s topline registered a marginal growth. In 2019 and 2020, where BNWM’s net sales slid, its bottomline also registered net losses.

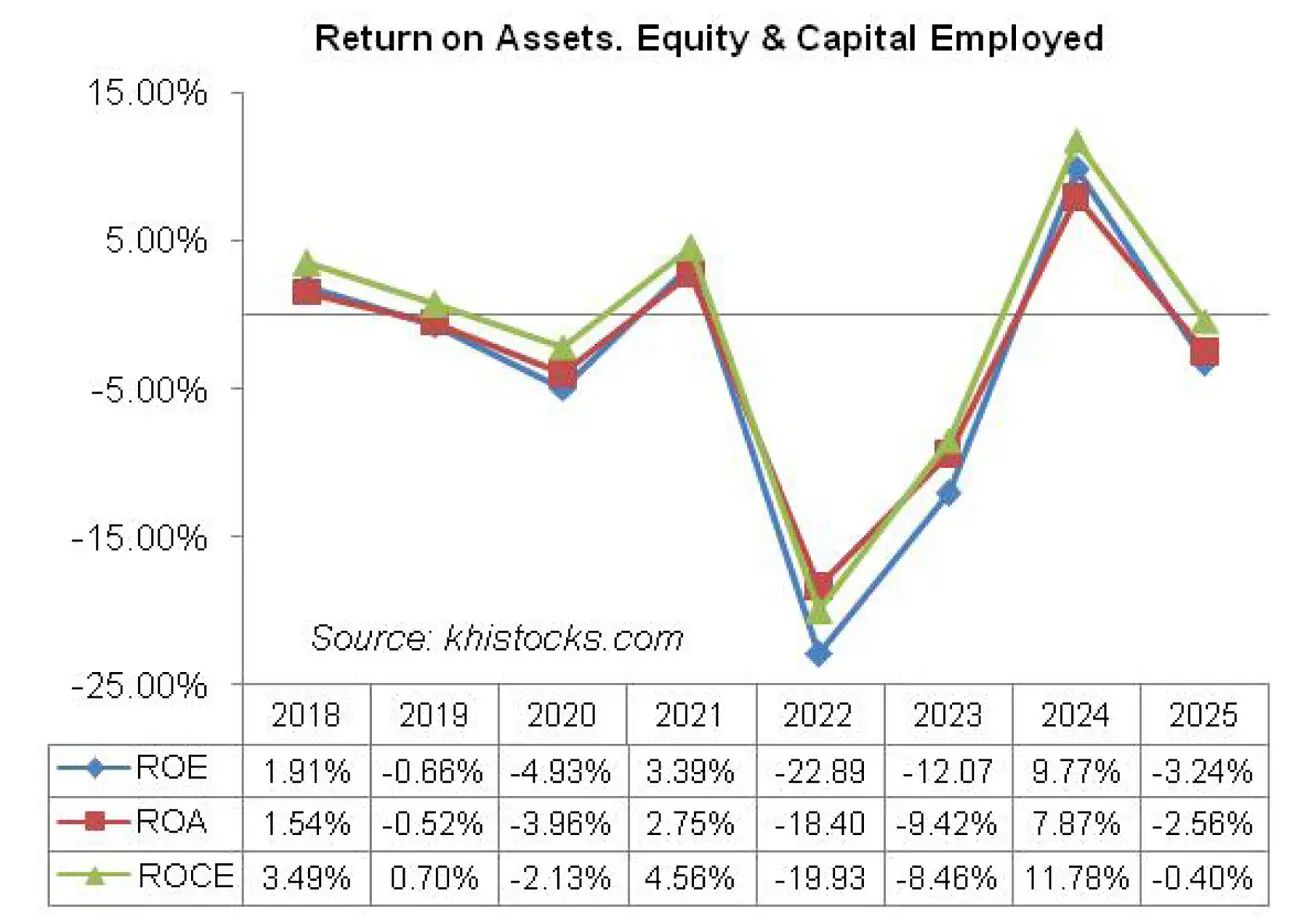

The company’s bottomline was recorded in the profit territory in 2021 but the bliss didn’t last for long as the company again posted net losses in 2022 and 2023 despite an uptick in net sales. In 2024, the company posted net profit which was followed by net loss in 2025. BNWM’s margins fluctuated over the period under consideration (see the graph of profitability ratios).

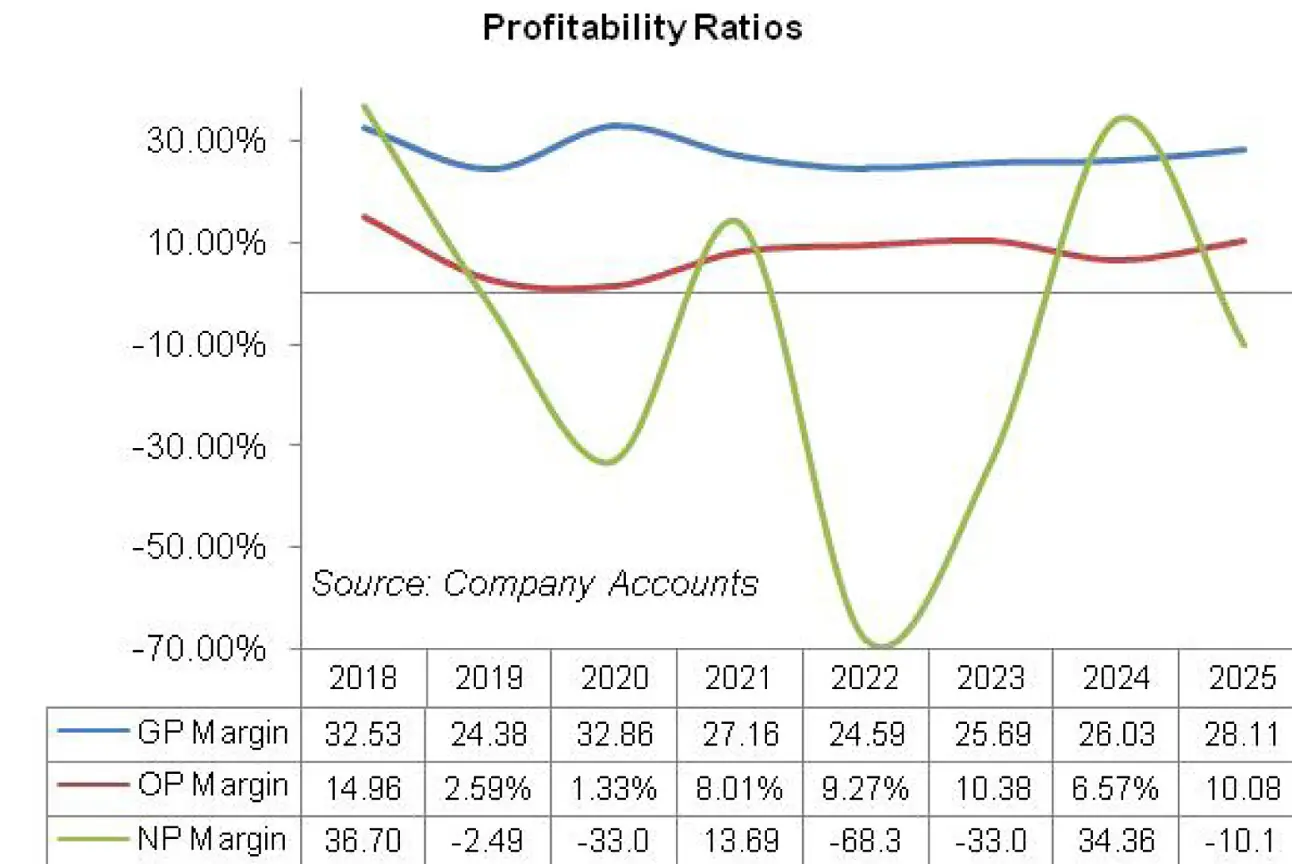

While gross and operating margins have stayed in the positive zone over the period, net margin has portrayed immense ebb and flow on account of the company’s investment in its associated companies. The detailed performance review of the period under consideration is given below.

In 2019, BNWM’s topline slipped by 18.33 percent year-on-year to clock in at Rs.684.91 million. This was on the back of reduced duration and severity of winter season in Pakistan which greatly affected the sales volume of the company. Deteriorating macroeconomic indicators including high inflation, weaker Pak Rupee and hike in electricity tariff added to ado.

In accordance with the reduced demand and to cut down the losses from accumulation of inventory, the company temporarily suspended two shifts of production operations and continued with only one shift. In 2019, BNWM produced 779,642 kgs of yarn and 1.09 million meters cloth which was down 62 percent and 29 percent year-on-year respectively.

Cost of sales didn’t shrink with the similar momentum as net sales because fixed cost wasn’t absorbed efficiently. This culminated into 38.80 percent dip in gross profit in 2019 with GP margin diving down to 24.38 percent in 2019 from 32.53 percent in 2018.

Operating expense dwindled by 2.13 percent year-on-year in 2019. While payroll expense drastically grew in 2019, it was offset by lower sales commission, rent, advertisement and promotion as well as repair & maintenance cost incurred during the year. Higher exchange loss and greater provisioning for ECL on trade debts pushed other expense up by 15.78 percent in 2019.

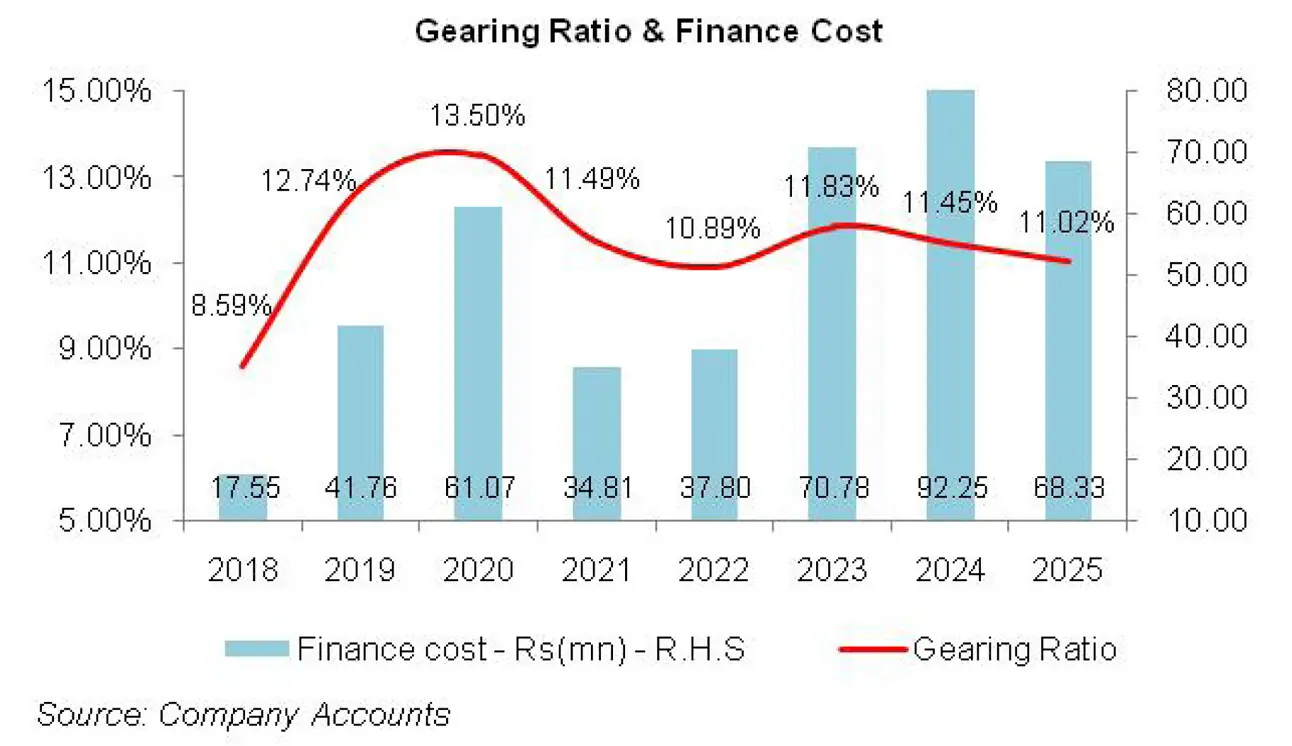

As a consequence, operating profit declined by 85.87 percent in 2019 with OP margin marching down from 14.96 percent in 2018 to 2.60 percent in 2019. Finance cost escalated by 137.92 percent in 2019 on account of greater short-term borrowings and higher discount rate.

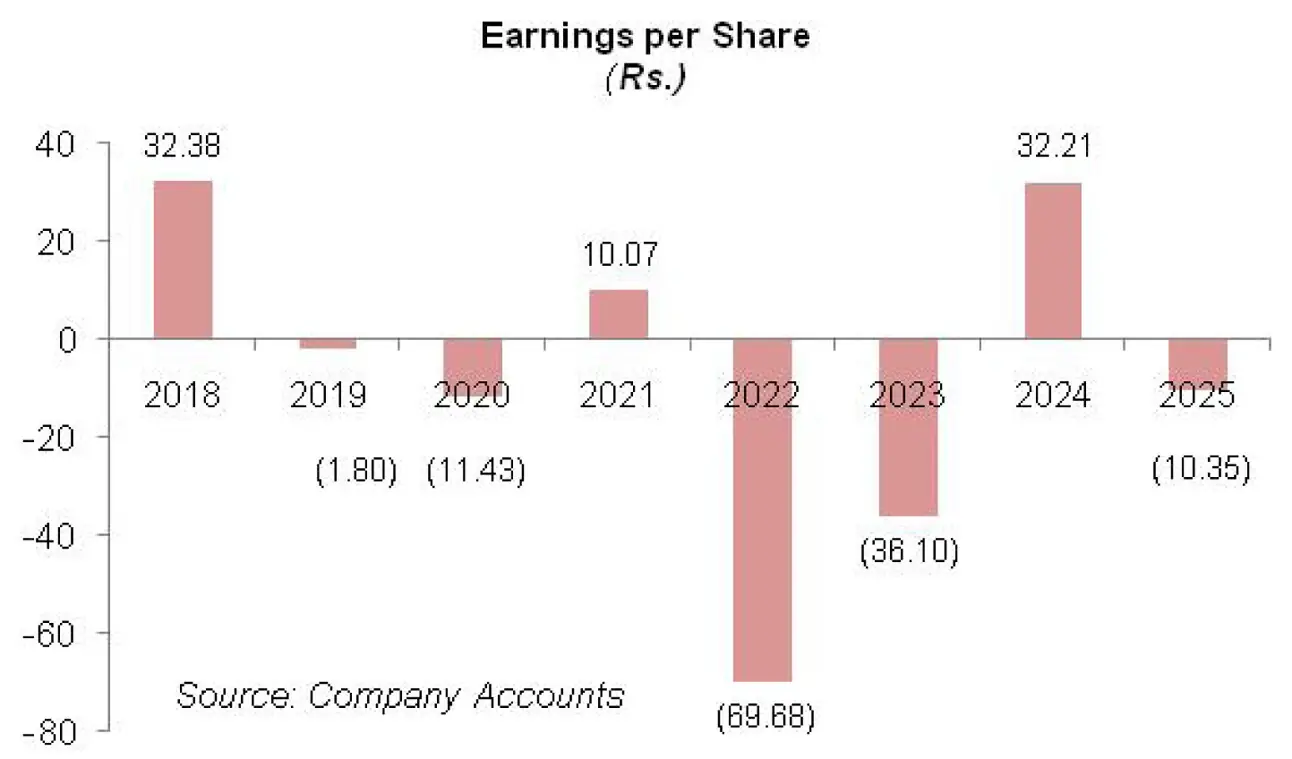

In 2018, BNWM had booked reversals worth Rs.365.33 million on its investment in an associated company which greatly buttressed its bottomline during the past year. However, the absence of such one-off gain in 2019 resulted in net loss of Rs.17.08 million in 2019 versus net profit of Rs.307.78 million posted in 2018. BNWM registered loss per share of Rs.1.80 in 2019 as against EPS of Rs.32.38 recorded in 2018.

In 2020, BNWM’s topline registered year-on-year decline of 52 percent to clock in at Rs.328.71 million. While the company’s sales were already grappling against adverse macroeconomic conditions and unfavorable weather for the past few years, the outbreak of COVID-19 further worsened the situation.

The company resumed its second production line in 2020 which was temporarily suspended last year, yet the production volume massively fell to 474,274 kgs of yarn, down 39 percent year-on-year and 494,507 meters cloth, down 55 percent year-on-year.

The curtailed production was the consequence of demand contraction and lockdown. Cost of sales slumped by 57.39 percent year-on-year in 2020. This greatly improved its GP margin to 32.86 in 2020 percent despite 35 percent slippage in gross profit.

Operating expense nosedived by 20 percent year-on-year in 2020 due to considerably lower sales commission, advertisement & promotion as well as payroll expense. BNWM reduced its number of employees from 467 in 2019 to 396 in 2020.

Significantly lower provisioning and no exchange loss resulted in 98.67 percent reduction in other expense in 2020. Other income multiplied by 537.94 percent in 2020 on account of mark-up recognized on dealers’ balances, exchange gain as well as gain on sale of vehicles.

Operating profit dwindled by 75.32 percent in 2020 with OP margin ticking down to 1.33 percent. Finance cost surged by 46.23 percent year-on-year in 2020 due to higher discount rate for most part of the year coupled with higher working capital related borrowings. This coupled with share of loss worth Rs.48.28 million and impairment loss worth Rs.17.46 on investment in associated companies radically tarnished the bottomline and culminated into net loss of Rs.108.65 million in 2020, up 536 percent year-on-year. This translated into loss per share of Rs.11.43 in 2020.

In 2021, BNWM’s net sales posted a rigorous rebound of 112.69 percent year-on-year to clock in at Rs.699.14 million. With the ease of lockdown restrictions, the company’s sales began to pick up and the company had to resume the third production line which was suspended in 2019. To fulfill the demand, the company produced 888,832 kgs of yarn and 1.28 million meters of cloth, up 87.4 percent and 159 percent respectively.

Cost of sales went up by 130.74 percent in 2021 which squeezed the GP margin to 27.16 percent despite 75.80 percent higher gross profit recorded during the year. Operating expense spiked by 23.63 percent year-on-year on account of higher sales commission as well as repair & maintenance expense incurred during the year. Higher profit related provisioning drove other expense up by 1262.13 percent in 2021.

Other income inched down by 32.49 percent in 2021 due to no mark-up income recognized on dealers’ balances, lesser exchange gain and lesser gain on sale of fixed assets in 2021. Operating profit multiplied by 1180.97 percent in 2021 with OP margin jumping up to 8 percent. BNWM was able to cut down its finance cost by 43 percent in 2021 owing to monetary easing and lesser borrowings in 2021.

The company also earned a share of profit worth Rs.78.72 million from its associated company. This translated into net profit of Rs.95.72 million in 2021 with EPS of Rs.10.07 and NP margin of 13.70 percent.

The growth trajectory continued in 2022 with 38.67 percent year-on-year inclination in net sales which clocked in at Rs.969.52 million. The production further rose to 1.17 million kgs of yarn and 1.44 million meters of cloth, up 31.7 percent and 12.6 percent respectively in line with demand recovery.

Cost of sales spiked by 43.57 percent year-on-year in 2022 on account of steep rise in inflation, Pak Rupee depreciation and hike in power tariff. This pushed the GP margin down to 24.60 percent in 2022. Operating expense largely remained unchanged in 2022.

While administrative expense rose on account of hike in payroll expense and utilities expense incurred during the year, massive drop in distribution expense due to discontinuation of commission to dealer from 2022 offset the hike in administrative expense during the year. Higher provisioning for ECL pushed other expense up by 578.15 percent in 2022.

Conversely, other income slid by 25.50 percent in 2022 on account of no exchange gain recognized during the year as well as no sale of trees made during the year. Operating profit improved by 60.39 percent in 2022 with OP margin marching up to 9.30 percent.

Finance cost grew by 8.61 percent year-on-year due to higher discount rate. BNWM also recognized a share of profit from associate company worth Rs.84.57 million in 2022. What turned tables for the company in 2022 was the massive unrealized impairment loss on investment in Janana De Malucho, an associate company of BNWM. This translated into an enormous net loss of Rs.662.40 million in 2022 with loss per share of Rs.69.68.

BNWM’s net sales posted a marginal rise of 7.14 percent in 2023 to clock in at Rs. 1038.73 million. This appears to be the effect of upward revision in prices to combat the mounting cost pressure. The demand shrank in 2023 on account of high inflation which took its toll on the purchasing power of consumers.

Production of yarn clocked in at 1.008 million kgs while production of cloth was recorded at 1.22 million meters of cloth, down 13.8 percent and 15.24 percent respectively in 2023. Cost of sales rose by 5.57 percent in 2023 on account of high inflation, Pak Rupee depreciation, high energy and power charges.

Gross profit ticked up by 11.94 percent in 2023 while GP margin slightly improved to 25.70 percent in 2023. Operating expense expanded by 16.83 percent in 2023 on the back of higher depreciation on right-of-use assets and rental arrears of past years. Other expense slumped by 75.47 percent on the back of lesser provisioning done for ECL.

Higher income on PLS account and increased sale of scrap resulted in 20.13 percent recovery in other income in 2023. Operating profit grew by 20 percent year-on-year with OP margin climbing up to 10.40 percent in 2023.

Impairment loss on investment in associate and share of loss from associate company coupled with elevated finance cost resulted in net loss of Rs.343.16 million in 2023 with loss per share of Rs.36.1 in 2023.

In 2024, BNWM’s net sales deteriorated by 14.20 percent to clock in at Rs.891.27 million. This was on account of squeezed purchasing power of consumers which led to lower demand. The company shut down its plants multiple times during the year due to lesser orders.

Production volume of yarn fell by 18.84 percent to clock in at 817,354 kgs while production volume of cloth fell by 19.59 percent to clock in at 983,791 meters in 2024. Cost of sales shrank by 14.59 percent in 2024, resulting in 13.10 percent thinner gross profit recorded by the company in 2024.

On the positive front, the company was able to drive up its GP margin to 26 percent in 2024 by revising the prices of its products in accordance with hiking cost. Operating expense multiplied by 11.96 percent in 2024.

While distribution expense dropped by 9.10 percent during the year owing to curtailed sales volume, administrative expense succumbed to inflationary pressure. 18.21 percent higher administrative expense incurred during the year was despite the fact that BNWM streamlined its workforce from 579 employees in 2023 to 447 employees in 2024.

Other expense fell by 93.65 percent in 2024 due to lesser provisioning done for WWF and WPPF. Other expense was wiped off by 25.41 percent improved other income recorded by BNWM in 2024. This was the result of higher profit recognized on PLS accounts due to higher discount rate.

Operating profit tapered off by 45.70 percent in 2024 with OP margin sliding down to 6.57 percent. Finance cost mounted by 30.34 percent in 2024 primarily due to higher discount rate while outstanding liabilities considerably reduced during the year.

During the year, BNWM incurred share of loss of Rs.111.92 million from its investment in associate company, Janana De Malucho. However, its impact was conveniently offset by the reversal booked on impairment loss on investment in associate. This was the result of “Market Value of Net assets approach” adopted by the company to provide more accurate value of its investments.

BNWM booked reversal of Rs.446.51 million of impairment loss in 2024. This resulted in net profit of Rs.306.21 million in 2024 as against net loss of Rs.343.16 million posted by the company in the previous year. EPS stood at Rs.32.21 in 2024 versus loss per share of Rs.36.10 posted last year. NP margin was recorded at 34.36 percent in 2024.

In 2025, BNWM’s topline ticked up by 8.67 percent to clock in at Rs.968.56 million. While macroeconomic indicators such as inflation, discount rate, exchange rate etc posted considerable improvement during the year, however, prolonged period of politico-economic instability had considerably squeezed the purchasing power of consumers which will take time to recuperate.

Owing to lower demand, yarn production dwindled by 33.37 percent to clock in at 612,863 kgs while cloth production deteriorated by 17.53 percent to clock in at 837,053 meters. Cost of sales grew by only 5.62 percent due to operational efficiency coupled with the ease of inflation. This coupled with the company’s continued focus on high-value products resulted in 17.34 percent improvement in the company’s gross profit in 2025 with GP margin attaining its 5-year highest level of 28.11 percent.

Distribution expense surged by 19.94 percent in 2025 due to higher salaries of sales force as well as elevated outward freight. Administrative expense stayed largely intact during the year.

As against last year, BNWM booked provision for WWF, WPPF and impairment of trade debts in 2025. This resulted in 886.42 percent escalation in other expense in 2025. Other income strengthened by 169.80 percent in 2025 on account of gain recognized on the sale of operating fixed assets and reversal of provision recorded on its associated company Waqf-e-Kuli Khan.

Operating profit mounted by 66.75 percent in 2025 with OP margin climbing up to 10 percent. Finance cost descended by 25.93 percent in 2025 due to monetary easing and lesser outstanding liabilities at the end of the year.

Share of loss from associated company, Janana De Malucho surged by 75.50 percent to clock in at Rs.196.42 million. Its impact was partially counterbalanced by the reversal worth Rs.85.71 million booked on impairment loss on investment in associate. This was in accordance with the “Market value of net assets” approach adopted by BNWM as per the requirements of IAS 36. The company recorded net loss of Rs.98.425 million in 2025 with loss per share of Rs.10.35.

Future Outlook

With tighter consumer spending due to contraction in the purchasing power, the demand may witness any slow recovery in the near-term. To cope up with this, BNWM is tweaking its product mix in favor of high-margin products and also focusing on achieving operational efficiency which includes solar energy expansion and working capital control to improve its financial performance.

Despite meticulous efforts to improve its profitability and margins, BNWM investment in its associate company, JDMT, is adversely affecting its financial performance and warrants meticulous review.

Comments

Comments are closed for this article.