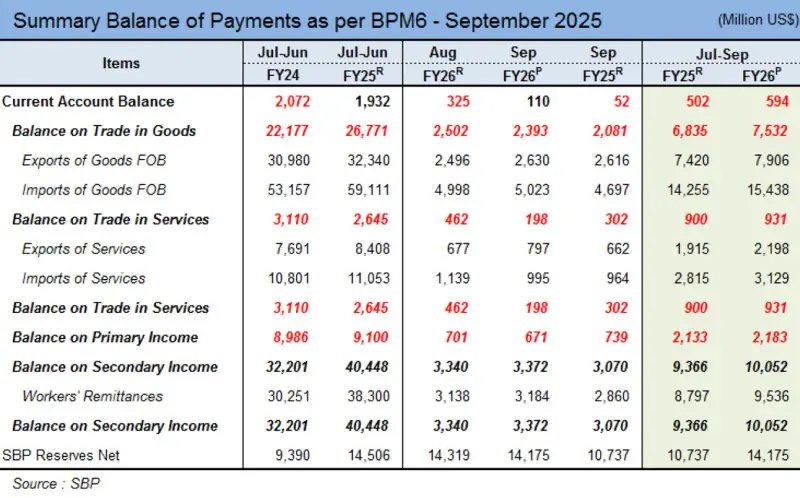

The current account surprisingly posted a surplus of $110 million in September 2025 even though the market was expecting a significant deficit based on the PBS trade data (shipment basis).

However, the trade deficit published by SBP (on payment basis) is almost a billion dollars less than what it was at PBS. There might not be any foul play, as payments and shipments have a lag and sometime the gap is higher than usual. However, when the gap is higher, in coming months, it converges – that is implying that we have to expect higher deficit in the 2QFY26.

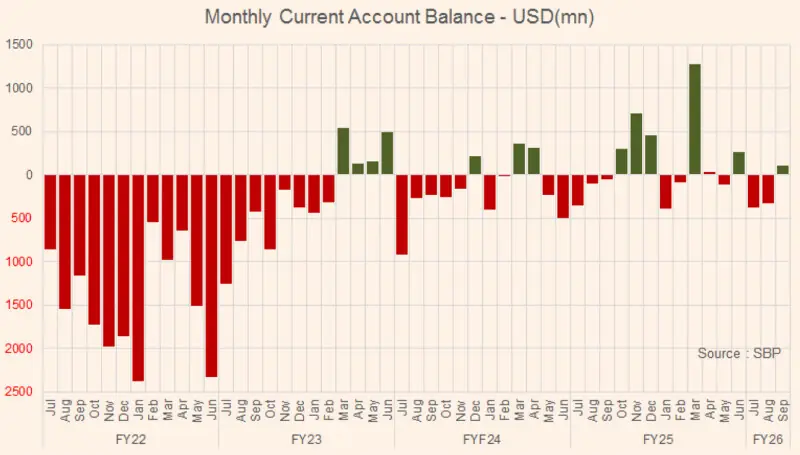

The current account deficit stood at $594 million in 1QFY26 as compared to a deficit of $502 million in the same period last year. Last year, the subsequent quarters had surpluses to result in full year surplus. That might not be the case this year, as imports (PBS) are picking up while remittances growth is low amid exports (PBS) are stagnating. It is a matter of time, the higher deficit to start reflecting in current account data too.

Goods imports stood at $5.0 billion in September (SBP data) while on shipment basis the toll stood at $5.9 billion. Based on PBS detailed data imports notably moved up in food group (33% YoY), machinery group (19% YoY) and transport group (146% YoY). Mobile phones’ imports almost doubled and so is the case for CKD cars. One of the sharpest increases (to $105 mn from $5 mn) in CKD buses, trucks and heavy vehicles.

The story is different in case of SBP – where bus and car imports numbers are significantly lower suggesting that the payments will get recorded in coming months. Car assemblers might have a delay in payment schedule. In CBUs buses case, Punjab government has imported a plethora ofbuses, and the payment must be made with some lag. Similar gaps are visible in food imports – especially palm oil. This implies that the import bill (payment basis) ought to grow and is likely to bring the current account into deficit.

Another alarming number is growing food trade deficit – based on PBS data (shipment basis), it stood at $1.1 billion in 1QFY26 as compared to mere $45 million in the same period last year. The number is going to get worse, as wheat is expected to be imported in months to come. What has happened is that rice exports bonanza has ended. Lats year or so, the rice exports were up, as India banned its exports for domestic political reasons, and now that has normalized, and so did our rice exports – fell by 42 percent in 1QFY26 to $713 million.

It is hard to find any goods export area where there is noticeable growth. Textile exports in 1QFY26 are marginally up by 6 percent while other manufacturing and food exports fell by 3 percent and 31 percent respectively. That is resulting in overall decline in exports to 4 percent in 1QFY26 to $7.6 billion.

However, SBP data show a slightly different picture – in 1QFY26, exports are up by 7 percent to $7.9 billion. It is likely that SBP numbers are less going forward. And in case of imports, SBP numbers are going to be higher. The overall trade deficit is to be worsened.

The only silver lining within trade data is falling oil prices. Already oil prices are lower this year – averaged at $69/ barrel in 1QFY26 as compared to $80/barrel in 1QFY25. That is why petroleum imports (PBS data) are down by 7 percent YoY where as both crude and petroleum products volumes are up by 10 percent and 15 percent, respectively. Oil prices are down further in October and likely to remain below $60 in the remaining year. That is to give room to let the non-oil imports grow without creating panic.

Another good news is of growing ICT exports –it is at all time monthly high of $366 million in September – up 25 percent YoY and its share in total goods and services exports have reached 10.7 percent. in 1QFY26, ICT exports are up by 21 percent to $1.1 billion.

The home remittances continue to grow on a high base – up by 8 percent to $9.5 billion. It would be challenging to keep the same pace in exports for the rest of the year, as the numbers significantly move up in the second half of the last year.

Thus, growing exports is the key to finance growing imports, as lower oil imports and slightly higher remittances might not be enough to pace up with non-oil imports – and to let the GDP to grow, the imports should move up further. And that is to increase the current account deficit. And to let that happen without triggering balance of payment crisis, financial and capital accounts need to grow.

There are no signs of any improvement in financial and capital accounts. FDI is down by 45 percent in 1QFY26 to $484 million versus $879 million same period last year. The decline is primarily due to higher repatriation resulting in lower retained earnings. Meanwhile, portfolio investment new outflow is $630 million versus net inflow of $143 million. These were dragging financial accounts into negative, but the general government services come to rescue which are up by $359 million versus outflow of $573 million last year. Overall financial account inflows stood at $527 million – down by 43 percent YoY.

Going forward, in order to build reserves (down by $274 mn in 1QFY26), financial accounts – especially government services have to be significantly positive. The government is eying improved geopolitical situation and leverage improved relation with the Middle East to reap fruits. If that happens, the balance of payment would remain comfortable. Otherwise, there is a crisis in the making.

Comments

Comments are closed for this article.