Good Luck Industries Limited (PSX: GIL) was incorporated in Pakistan as a public limited company in 1967. The company is engaged in the milling of wheat and all kinds of grains. The main products of GIL are maida (all-purpose flour), fine flour, bran and mill flour (chakki atta).

Pattern of Shareholding

As of June 30, 2025, GIL had a total of 300,000 shares outstanding which were held by 79 shareholders. Individuals represent the largest shareholder category of GIL with 59.87 percent shares followed by directors, CEO, their spouse and minor children having a stake of 40.11 percent in GIL.

The remaining 0.02 percent shares are held by NIT and ICP.

Financial Performance (2019-25)

Over the period under consideration, GIL’s topline posted a dip twice i.e. in 2020 and 2025. However, its bottomline took a slide thrice i.e. in 2020, 2023 and 2024. The company’s margins show a cyclical trend.

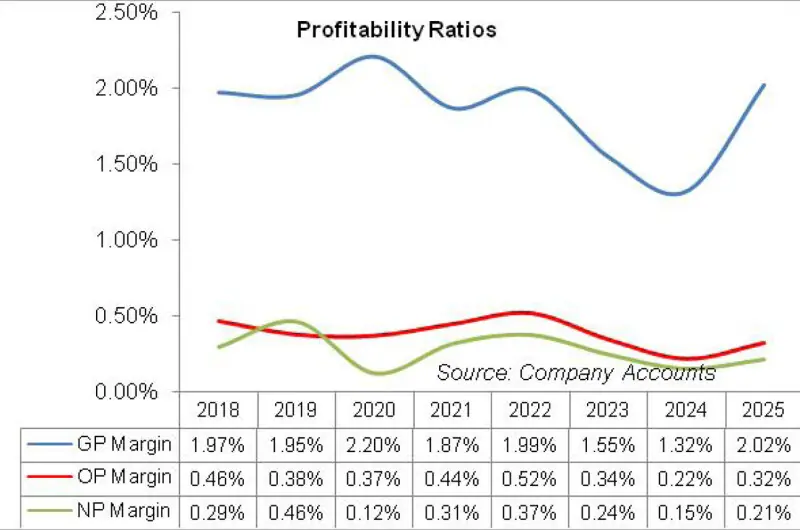

Gross margin registered its optimum level in 2020 while operating margin peaked in 2022. Conversely, net margin maxed out in 2019 (see graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, GIL’s topline posted a marginal 6.30 percent growth year-on-year to clock in at Rs.896.78 million. The sale of atta and katta packings were the main growth drivers. Conversely, the sale of maida slid during the year.

The company produced 28.1 million kgs of flour in 2019, which was 15.6 percent higher than the production volume of 2018. This translated into capacity utilization of 30 percent in 2019 versus capacity utilization of 26 percent recorded in the previous year.

Despite high demand, the company couldn’t fully utilize its capacity due to ban imposed by the government on the movement of wheat from one province and one district to another occasionally during the year. The fixation of wheat quota by the food department also impeded the production activity of GIL.

Moreover, lesser production of wheat in Sind province also created supply shortage during the year. Cost of sales also grew by 6.31 percent year-on-yearin 2019 as the wheat support price grew by Rs.50 to clock in at Rs.1350 per 40 kg.

The government had last raised the support prices in FY15 from Rs,1200 to Rs.1300 per 40 kg. Gross profit grew by 5.40 percent year-on-year in 2019 while GP margin stood at 1.95 percent versus GP margin of 1.97 percent recorded in 2018. Operating expense inched up by 7.10percent year-on-year in 2019 which largely comprised of payroll expense.

During 2019, the company added 5 new employees to its team, taking the tally to 39 employees. Operating profit slipped by 13.82 percent year-on-year in 2019 with OP margin slightly dropping to 0.38 percent from OP margin of 0.46 percent posted in 2018. GIL’s finance cost only comprised of bank charges which inched up by 3.53 percent year-on-year in 2019.

The effect of prior year’s current and deferred tax charge culminated in a tax credit of Rs.0.76 million in 2019. This resulted in 66.36 percent year-on-year rise in net profit which clocked in at Rs. 4.12 million in 2019 with NP margin of 0.46 percent versus NP margin of 0.29 percent recorded in 2018. EPS also grew from Rs.8.25in 2018 to Rs.13.72 in 2019.

In 2020, GIL’s net sales plummeted by 4.13 percent year-on-year to clock in at Rs.859.76 million. The company produced 21.38 million kgs of flour in 2020 which was 24 percent lesser than the production volume attained in 2019. This culminated into capacity utilization of 23 percent in 2020. Except for an uptick in the net sales of bran, all other categories registered sales decline in 2020.

The destruction of demand can be attributed to the closure of HORECA industry during COVID-19. With low production, the cost of sales also shrank by 4.37 percent. This drove the gross profit up by 8.25 percent year-on-year which translated into GP margin of 2.20 percent in 2020.

The number of employees grew to 41 in 2020 resulting in 14.96 percent year-on-year hike in the operating expense. Operating profit narrowed down by 6.10 percent year-on-year n 2020, however, OP margin stayed range bound at 0.37 percent.

Finance cost dropped by 55.27 percent year-on-year in 2020 which comprised of only bank charges. Higher effective tax rate due to tax effect of depreciation allowance further squeezed the bottomline which tapered by 74.84 percent year-on-year in 2020 to clock in at Rs.1.04 million. This translated into NP margin of 0.12 percent and EPS of Rs.3.45 in 2020.

GIL’s net sales revived in 2021, boasting 39 percent year-on-year growth to clock in at Rs.1195.26 million.

All the product categories performed well during the year with maida making the highest contribution to the net sales followed by katta packing. GIL’s production grew by 3.3 percent in 2021 with capacity utilization standing at 24 percent. This translated into annual production of 22.094 million kgs in 2021. Cost of sales grew by 39.50 percent year-on-year.

Gross profit enhanced by 17.66 percent year-on-year in 2021; however, GP margin marched down to 1.87 percent. This was due to higher support price of wheat, especially in Sind and Baluchistan where it jacked up to Rs.2200 per 40 kg.

Operating expense spiked by 6.80 percent year-on-year due to higher payroll expense on account of inflation while number of employees stayed at 41. Operating profit rebounded by 67.80 percent year-on-year in 2021 with OP margin clocking in at 0.44 percent. Finance cost(bank charges) escalated by 28 percent year-on-year.

Tax effect of depreciation allowance resulted in 27.53 percent year-on-year plunge in tax charge for the year. Consequently, net profit magnified by 263.31 percent year-on-year in 2021 to clock in at Rs.3.76 million. This resulted in NP margin of 0.31 percent and EPS of Rs.12.54 in 2021.

In 2022, GIL net sales grew by a marginal 3.35 percent year-on-year to clock in at Rs.1235.29 million. The decline in the net sales of atta largely offset the higher turnover of other categories. GIL’s production slid by 6 percent year-on-year to 20.765 million kgs in 2022. This translated into capacity utilization of 22 percent – the lowest since 2018.

Cost of sales inched up by 3.22 percent, resulting in 10 percent higher gross profit recorded in 2022. GP margin also slightly grew to 2 percent in 2022.

Operating expense escalated by 6.75 percent year-on-year in 2022 on account of inflation and rise in employee headcount to 44. Operating profit burgeoned by 19.87 percent year-on-year with OP margin slightly ticking up to 0.52 percent in 2022.

Finance cost/bank charges hiked by 21.77 percent year-on-year in 2022. Net profit picked up by 22.16 percent year-on-year in 2022 in clock in at Rs.4.60 million with NP margin of 0.37 percent and EPS of Rs.15.32 – the highest among all the years under consideration.

The monsoon floods greatly affected the agricultural output of the country during the first half of the year. This created immense shortage of wheat.

The Sind government raised the minimum support price to an exorbitant level of Rs.4000 per 40 kg to encourage the growers. However, this resulted in unprecedented level of food inflation in the country. GIL’s production slid by 2.6 percent in 2023 to clock in at 20.221 million kgs.

This resulted in capacity utilization of21.81 percent.GIL’s net sales grew by 43.32 percent year; however, GP margin fell to 1.55 percent despite 11.52 percent rise in gross profit in 2023. High inflation and transportation charges pushedoperating expense up by 18.81 percent year-on-year in 2023.

This squeezed the operating profit by 4.25 percent year-on-year with OP margin sinking to 0.34 percent in 2023. Finance cost measured 3.69 percent year-on-year in 2023. This resulted in 5.80 percent thinner bottomline in 2023. Net profit stood at Rs.4.33 million in 2023 with NP margin of 0.24 percent and EPS of Rs.14.42.

In 2024, GIL’s topline grew by 22.40 percent to clock in at Rs.2166.95 million. This mainly came on the back of higher prices of wheat purchased from Food Department and open market. During the year, the company’s production volume stood at 18.945 million kgs, down 6.3 percent year-on-year. This translated into the lowest ever capacity utilization of 20.44 percent recorded in 2024.

Unprecedented spike in the prices of electricity, transportation as well as other related items resulted in 22.69 percent surge in cost of sales in 2024. In absolute terms, gross profit ticked up by 4.33 percent in 2024, however, GP margin slumped to its multiyear low level of 1.32 percent.

Operating expense escalated by 19.82 percent in 2024 particularly due to higher payroll expense which was the result of inflation and increase in workforce from 42 employees in 2023 to 46 employees in 2024. Operating profit tapered off by 22.48 percent in 2024 with OP margin sliding down to 0.22 percent.

Finance cost increased by 24.73 percent in 2024. GIL recorded 24.65 percent decline in its net profit in 2024 which clocked in at Rs.3.263 million with EPS of Rs.10.88 and NP margin of 0.15 percent.

In 2025, GIL recorded 25.86 percent year-on-year deterioration in its topline which clocked in at Rs.1606.64 million. This was due to decreased rate of wheat in the open market which enabled the company to align its prices.

Reduced commodity prices also enabled the company to record 26.38 percent lower cost of sales in 2025. This translated into 13.50 percent uptick in gross profit with GP margin ticking up to 2 percent. Operating expense surged by 17.14 percent in 2025 due to inflationary pressure. GIL also recorded other income of Rs.2.76 million in 2025, up 50.55 percent year-on-year. This largely included profit on bank deposits followed by reversal of provision booked for ECL.

Higher profit related provisioning resulted in 10.24 percent spike in other expense in 2025. Operating profit improved by 9.13 percent in 2025 with OP margin ticking up to 0.32 percent. Finance cost (bank charges) escalated by 86.14 percent in 2025. GIL recorded 4.36 percent uptick in its net profit which clocked in at Rs.3.405 million in 2025. This translated into EPS of Rs.11.35 and NP margin of 0.21 percent in 2025.

Future Outlook

Wheat prices,which declinedtotheir 3-year low level during August-25, bounced back in September-25. The main underlying factor is the ban imposed by Punjab government on inter-provincial wheat movement.

The other three provinces depend on the surplus of Punjab to meet its demand in the off-season, the prohibition of which has created insufficiency in the other three provinces.

However, the reason behind the ban on inter-state movement of the commodity is not clear. Post flood damages may be one of the reasons.

However, secrecy on such issues will further spark the price hike. Farmers are also reluctant to plant wheat in the anticipation of commercial import to cool down the prices. Transparency in this matter will not only give a clear direction to the farmers but will also manage the prices of the essential commodity.

Comments

Comments are closed for this article.