Rafhan Maize Products Company Limited (PSX: RMPL) started its operations in Pakistan as a corn refining industry in 1953. Over the course of years, the company has grown into one of the biggest agro based industries of Pakistan.

RMPL produces a variety of food ingredients and industrial products using maize as a basic raw material. RMPL turned into a public limited company in 1985.

Pattern of Shareholding

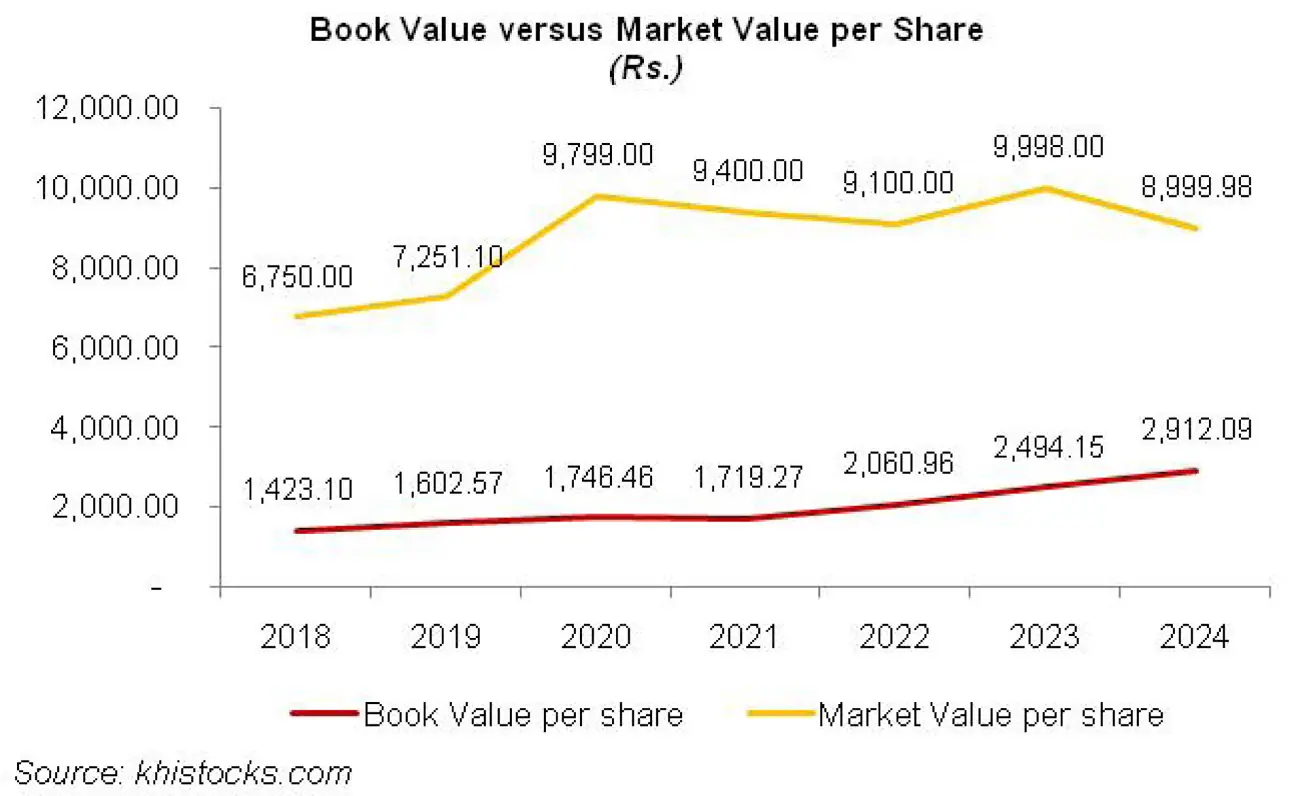

As of December 31, 2024, the company has a total of 9.236 million shares outstanding which are held by 1158 shareholders. Ingredion Incorporated Chicago, USA (parent company) holds 71.04 percent shares of RMPL followed by local general public with a stake of 19.21 percent in the company.

Directors, CEO, their spouse and minor children own around 7.04 percent shares of RMPL while Insurance companies account for 1.49 percent shares. Around 1 percent of the company’s shares are held by Banks, DFIs and NBFIs. The remaining shares are held by other categories of shareholders.

Financial Performance (2020-24)

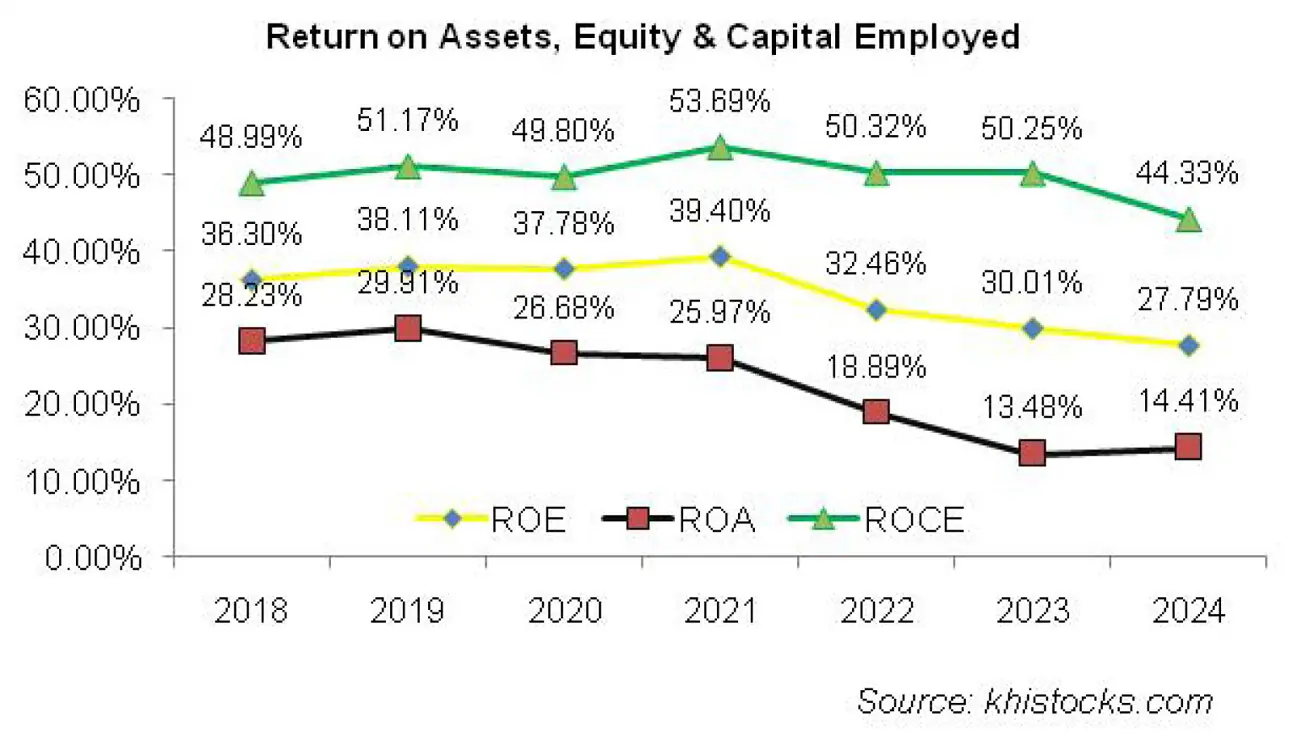

RMPL’s margins posted year-on-year growth over the period under consideration. The bottomline also followed the similar trajectory except for a nosedive in 2022 where the company attained the highest topline growth in five years.

Margins inched down in 2019 followed by a staggering rebound in 2020 where they attained their optimum level. In the subsequent two years, the margins deteriorated. In 2023, RMPL’s margins ticked up. In 2024, gross and operating margins fell while net margin posted a skimpy growth. The detailed performance review of the period under consideration is given below.

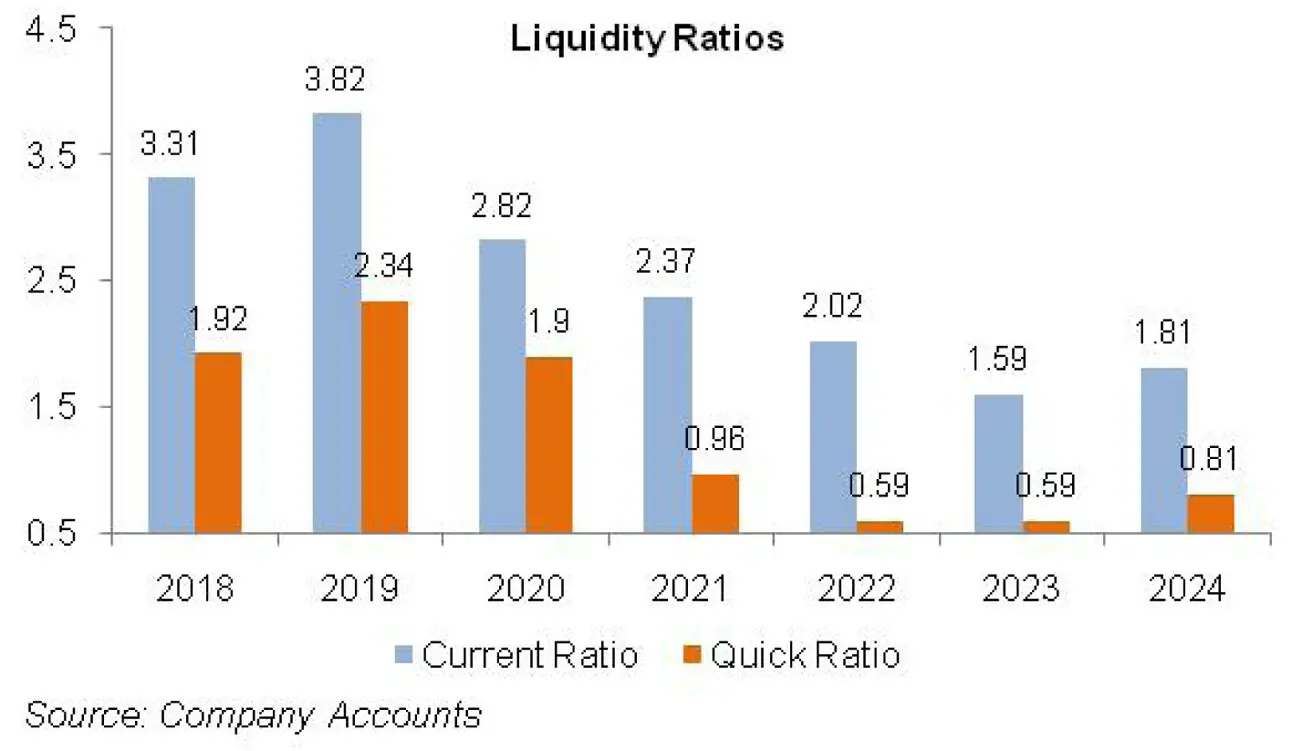

In 2020, RMPL faced significant volumetric sales loss particularly due to subdued textile sector activity due to COVID-19 related lockdown and cancellation of export orders. Food segment performed better despite the closure of restaurants, schools, marriage halls etc as household demand spurred.

Household demand of food, beverages, pharmaceuticals, processed food, condiments etc also stimulated the demand of RMPL’s food grade starches in those sectors. Lower off-take was offset by price increase resulting in 1.74 percent year-on-year growth in topline which clocked in at Rs. 35,873.33 million.

Upward price revision and a downtick in cost of sales due to lower sales volume resulted in GP margin of 27.27 percent in 2020 as against GP margin of 25.44 percent recorded in the previous year.

In absolute terms, gross profit inched up by 9 percent in 2020. Distribution and administrative expense ticked up by 6.65 percent and 5.70 percent respectively in line with inflationary pressure.

Other income turned out to be stunning, boasting 36.20 percent year-on-year growth mainly on account on markup on deposits and staff loans.

However, other income was offset by 10.70 percent higher other expense recorded in 2020 on the back of increased provisioning done for WWF and WPPF. OP margin jumped up to 23.75 percent in 2020 versus OP margin of 21.98 percent registered in the previous year. In absolute terms, operating profit ticked up by 9.93 percent in 2020.

Finance cost increased by 99.36 percent in 2020 despite the fact that discount rate ticked down amidst COVID-19 to regain the lost momentum in economic activity.

Growth in finance cost was mainly on account of long-term refinancing attained from SBP for the payment of wages and salaries. Besides foreign exchange loss also fueled the growth of finance cost.

The bottomline grew by 11.95 percent year-on-year to clock in at Rs.6094.23 million in 2020 with EPS of Rs.659.80. This was against the EPS of Rs.589.36 posted in 2019. NP margin clocked in at 17 percent as against 15.44 percent in 2019.

In 2021, RMPL’s topline grew by 18.78 percent year-on-year to clock in at Rs.42,609.63 million.

The topline growth was supported by both price and volumetric increase. However, high cost of sales particularly because of elevated fuel and power cost as well as high prices of specific varieties of corn put GP margin under pressure which clocked in at 24.22 percent in 2021.

In absolute terms, gross profit inched up by 5.48 percent in 2021. Distribution expense inched up by 4.92 percent in 2021 due to elevated commission expense incurred during the year. Administrative expense mounted by 21.94 percent in 2021 due to higher payroll expense which was the result of inflationary pressure.

RMPL streamlined in workforce from 1122 employees in 2020 to 1064 employees in 2021. Other income posted 18 percent improvement over the last year due to increased mark-up income on bank deposits and staff loan as well as gain recorded on the sale of scrap in 2021.

However, other income was counterbalanced by 10.54 percent higher other expense recorded in 2021 on account of profit related provisioning. Operating profit ticked up by 5.49 percent in 2021 while OP margin fell to 21 percent.

Finance cost plunged by 0.78 percent year-on-year in 2021. Monetary easing and the absence of foreign exchange loss played its role in keeping the finance cost in check. RMPL’s net profit posted a marginal 2.68 percent year-on-year growth to clock in at Rs.6257.32 million in 2021. This translated into EPS of Rs.677.46 and NP margin of 14.70 percent.

In 2022, RMPL boasted 37.89 percent year-on-year growth in its net sales which clocked in at Rs.58,755.77 million. This was the result of better sales mix and prices which compensated for volume loss. Growth in export revenue was majorly driven by Pak Rupee devaluation which resulted in higher exchange gain for the company.

In the domestic market, while textile as well as paper and corrugation sectors continued to grapple owing to floods, weakening exports, high energy cost, recession etc, food sector provided much needed growth momentum to RMPL. 45.31 higher cost of sales incurred in 2022 didn’t let RMPL sustain its GP margin which dropped to five-year low level of 20.14 percent.

In absolute terms, gross profit picked up by 14.68 percent in 2022. Distribution expense escalated by 23.91 percent in 2022 due to higher commission expense and increased salaries of sales force.

Administrative expense surged by 34.11 percent in 2022 due to increase in IT, data communication and networking charges as well as higher payroll expense.

RMPL expanded its workforce to 1075 employees in 2022. Other income grew by 12.56 percent in 2022 due to higher profit recognized on the sale of scrap and robust foreign exchange gain. In line with the previous year, other income was offset by 10.58 percent higher other expense which encompassed provisioning done for WWF and WPPF.

Operating profit grew by 12.69 percent in 2022, however, OP margin fell down to its lowest level of 17.24 percent. Finance cost multiplied by a massive 347.76 percent in 2022 owing to higher discount rate as well as increased short-term running finances obtained during the year.

RMPL bottomline tapered off by 1.25 percent year-on-year to clock in at Rs.6179.39 million. This translated into NP margin of 10.52 percent and EPS of Rs.669.02.

In 2023, RMPL’s topline grew by 11.42 percent to clock in at Rs.65,466.70 million. While textile sector demand continued to struggle owing to higher energy cost and global demand destruction, paper & corrugation segment and food segment showed resilience during the year.

The company also explored new export markets resulting in improvement in export sales. Upward price revision to combat inflationary pressure, elevated energy cost and higher global commodity prices also supported topline growth in 2023.

Cost of sales surged by 9.70 percent in 2023 due to the reasons stated above. Gross profit strengthened by 18.24 percent in 2023 with GP margin picking up to 21.37 percent. Distribution expense posted 19.15 percent growth in 2023 on account of higher commission expense and increased salaries of sales force.

Administrative expense spiraled by 37.30 percent in 2023 due to higher IT, networking and data communication charges and increased payroll expense as the company further enhanced its workforce to 1097 employees.

Other income posted a phenomenal growth of 122.97 percent in 2023 particularly on the back of hefty mark-up income, dividend income and profit on sale of scrap. Unlike previous year, in 2023, other income outnumbered other expense.

Other expense grew by 19.49 percent in 2023 due to exchange loss and profit related provisioning. RMPL posted 23.45 percent higher operating profit in 2023 with OP margin climbing up to 19.10 percent. 143.61 percent higher finance cost incurred in 2023 was the consequence of monetary tightening and increased external financing.

RMPL’s net profit progressed by 11.87 percent to clock in at Rs.6912.78 million in 2023. This translated into EPS of Rs.748.43 and NP margin of 10.56 percent in 2023.

In 2024, RMPL’s topline posted a marginal year-on-year growth of 6.81 percent to clock in at Rs.69,922.60 million.

Sales growth was mainly attributable to price increase and increase in export sales on the back of tapping new markets. Overall volumes remained subdued due to lackluster performance of textile sector which is the major customer of RMPL.

Cost of sales surged by 7.42 percent due to high inflation and Pak Rupee depreciation in the 1HCY25 as well as elevated energy cost. Gross profit picked up by 4.56 percent in 2024, however, GP margin slightly inched down to 20.92 percent.

Distribution and administrative expenses grew by 13.56 percent and 10.46 percent respectively during the year. The main growth propellers were enhanced payroll expense, communication expense as well as commission expense. RMPL streamlined its workforce to 1057 employees in 2024.

Other income which showed resilience throughout the period under review ticked down by 5.88 percent in 2024 due to considerable decline in mark-up on bank deposits on account of the onset of monetary easing during the year.

The absence of foreign exchange loss during the year pushed down other expense by 2.16 percent in 2024. Operating profit posted a marginal growth of 2.53 percent in 2024 with OP margin sinking to 18.33 percent.

Finance cost escalated by 54.14 percent in 2024 due to increased short-term and long-term financing and higher discount rate for most part of the year. Net profit picked up by 8.13 percent to clock in at Rs.7475.11 million in 2024. This translated into EPS of Rs.809.31 and NP margin of 10.69 percent in 2024.

Recent Performance (1HCY25)

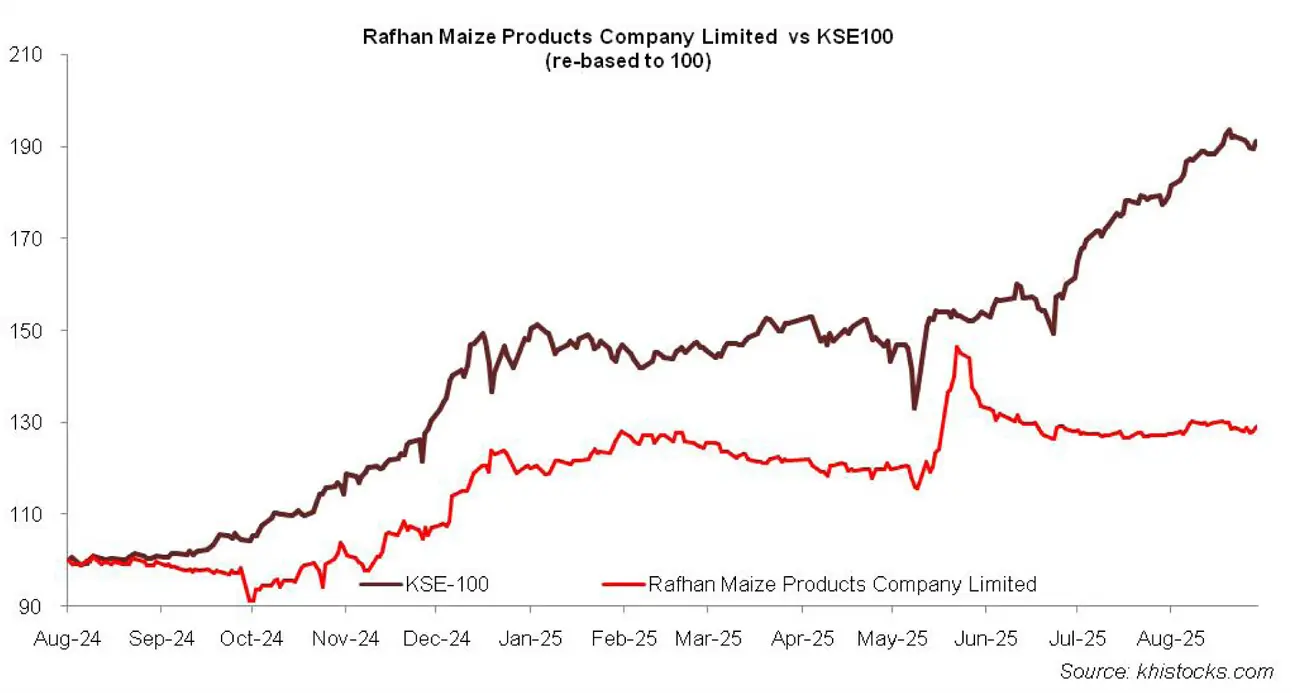

During the first half of CY25, RMPL posted 8.63 percent year-on-year growth in its topline which clocked in at Rs.36,530.20 million.

The growth was mainly backed by superior export sales due to the company’s continuous efforts to enhance its geographical outreach and strengthen its relationship with the existing global clients.

Across segments, packaging, chemical, home and personal care segments showed robust growth during the year. Conversely, textile and paper & board segments couldn’t register any sound growth. Food and animal nutrition segments remained stable during the year. Cost of sales mounted by 8 percent in 1HCY25 due to higher energy cost and rising corn prices.

However, with superior export sales, the company was able to drive 11.17 percent growth in its gross profit in 1HCY25. GP margin also stayed intact at 21 percent in 1HCY25. Increased focus on cross border sales culminated into 26.36 percent higher distribution expense in 1HCY25. Administrative expense ticked up by 7.82 percent in 1HCY25 due to higher payroll expense as well as communication charges.

Superior gain recognized on the sale of investment and robust mark-up income in 1HCY25 was offset by no foreign exchange gain and thinner dividend income, resulting in a paltry 5.37 percent growth recorded in other income in 1HCY25.

Higher profit related provisioning seems to be the cause of 22 percent higher other expense recorded in 1HCY25. Operating profit picked up by 8.97 percent in 1HCY25 with OP margin staying intact at 18.30 percent. Finance cost ticked up by 3.85 percent in 1HCY25 due to higher working capital related financing obtained during the period.

Net profit ticked up by 4.19 percent to clock in at Rs.3866.104 million in 1HCY25. This translated into

EPS of Rs.418.57 in 1HCY25 versus EPS of Rs.401.72 recorded in 1HCY24. NP margin was maintained at 11 percent in 1HCY25.

Future Outlook

Improvement in macroeconomic indicators has provided some respite; however, rising geopolitical tensions, global recession, increased competition and heightened energy tariff continue to suppress the company’s financial performance.

The company aims to combat these challenges by controlling non-productive cost and enhance its export sales.

Comments

Comments are closed for this article.